2026 Retirement Income Gap: Bridge 20% Shortfall with Strategic Withdrawals

Effectively addressing the projected 20% 2026 retirement income gap requires understanding strategic withdrawal methods and proactive financial adjustments to ensure long-term stability.

As we look towards 2026, the prospect of a significant 2026 retirement income gap looms large for many Americans. This projected 20% shortfall isn’t just a number; it represents a tangible threat to the financial security and peace of mind of retirees. Understanding the factors contributing to this gap and, more importantly, developing strategic withdrawal plans are paramount to safeguarding your retirement dreams.

Understanding the 2026 Retirement Income Gap

The notion of a retirement income gap refers to the difference between the income retirees expect to have and the income they actually receive or need to maintain their desired lifestyle. For 2026, various economic indicators and demographic shifts point to a potential 20% deficit for many households. This isn’t a sudden phenomenon but rather the culmination of several long-term trends.

Several factors contribute to this growing challenge. Increased life expectancies mean retirement savings need to stretch further than ever before. Rising healthcare costs continue to erode retirement funds, often exceeding initial projections. Furthermore, persistent inflation, even at moderate levels, significantly reduces the purchasing power of fixed incomes over time. The evolving landscape of Social Security and pension plans also plays a crucial role.

Economic Headwinds and Their Impact

Forecasters anticipate continued economic volatility, which can affect investment returns and job security for those nearing retirement. Market downturns, even temporary ones, can severely impact a retirement portfolio, especially for those in the withdrawal phase. Low interest rates, while favorable for borrowers, can be detrimental to savers who rely on fixed-income investments for a portion of their retirement income.

- Inflationary Pressures: The erosion of purchasing power due to rising costs for everyday goods and services.

- Market Volatility: Unpredictable swings in investment values impacting portfolio longevity.

- Healthcare Expenses: Ever-increasing costs for medical care, prescriptions, and long-term care.

- Interest Rate Environment: Low returns on traditionally safe investments like bonds and savings accounts.

The confluence of these factors creates a challenging environment for retirees, making it imperative to re-evaluate traditional retirement planning models. Acknowledging this potential 20% gap is the first step toward developing robust strategies to mitigate its impact and ensure a comfortable retirement.

In conclusion, the 2026 retirement income gap is a complex issue driven by a combination of economic, demographic, and systemic factors. Recognizing these underlying causes is essential for individuals to proactively adjust their financial strategies and avoid being caught unprepared.

Assessing Your Personal Retirement Shortfall

Before you can bridge the 2026 retirement income gap, you first need to accurately assess your personal financial situation. This involves a thorough review of your current assets, projected expenses, and potential income sources in retirement. Many individuals underestimate their future needs or overestimate the security of their existing savings.

Start by calculating your anticipated monthly expenses in retirement. Don’t just think about the big costs like housing; consider everything from groceries and utilities to leisure activities, travel, and unexpected emergencies. Be realistic about healthcare costs, as these often increase significantly with age. Once you have a clear picture of your expenses, compare this to your projected retirement income from sources like Social Security, pensions, and investment withdrawals.

Tools and Resources for Calculation

Several online calculators and financial planning tools can help you estimate your shortfall. These tools often allow you to input various scenarios, such as different inflation rates or investment returns, to see how they might affect your long-term financial health. Working with a qualified financial advisor can also provide invaluable insights and personalized projections.

- Retirement Calculators: Online tools that estimate your savings needs based on desired income and lifestyle.

- Financial Planners: Professionals who can provide personalized analysis and strategy development.

- Budgeting Software: Applications that help track current spending and project future expenses.

- Social Security Statements: Essential for understanding your projected benefits.

It’s crucial to be honest and comprehensive in this assessment. Overlooking potential costs or being overly optimistic about returns can lead to a larger gap than anticipated. Consider factors like potential long-term care needs, which can be a significant drain on resources if not planned for.

Ultimately, a precise assessment of your personal retirement shortfall provides the foundation for effective planning. Without a clear understanding of the gap, any strategies implemented will be based on assumptions rather than concrete data, potentially leading to inadequate preparation for the 2026 retirement income gap.

Strategic Withdrawal Methods to Maximize Income

Once you understand the potential 2026 retirement income gap, the next critical step is to implement strategic withdrawal methods. Simply pulling money from your accounts without a plan can quickly deplete your savings. The goal is to create a sustainable income stream that lasts throughout your retirement, even with a reduced portfolio.

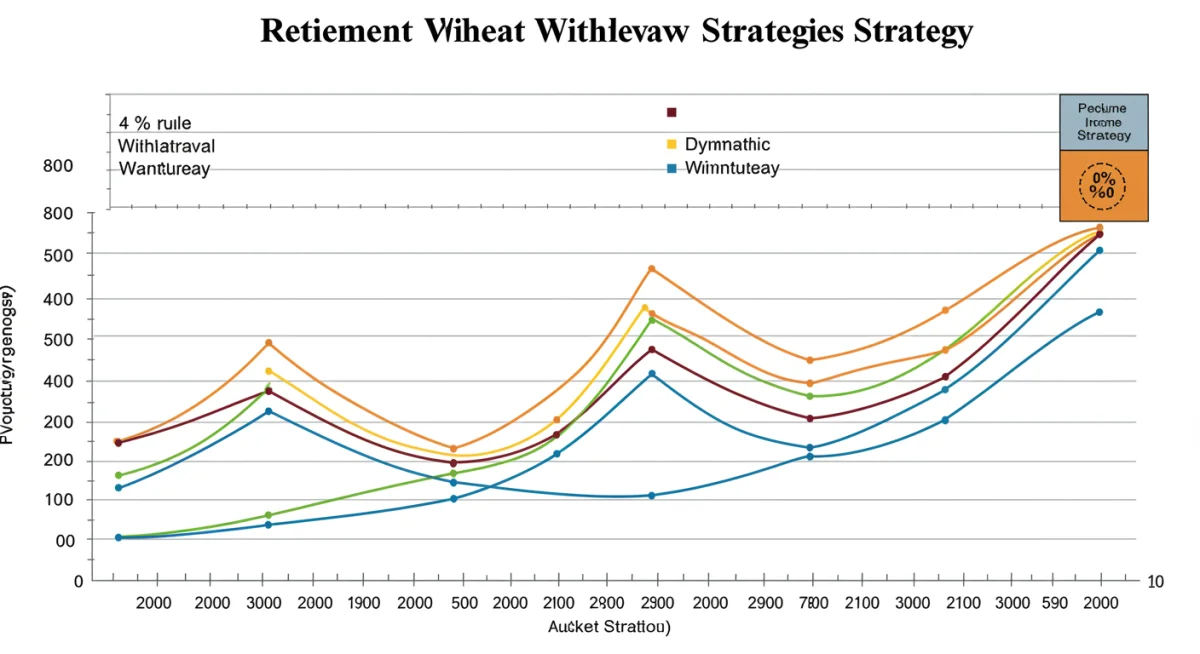

One of the most well-known strategies is the 4% rule, which suggests withdrawing 4% of your initial retirement portfolio value in the first year, then adjusting that amount for inflation in subsequent years. While a good starting point, its effectiveness can vary depending on market conditions and individual circumstances. More dynamic strategies are often necessary in today’s economic climate to address the 2026 retirement income gap.

Dynamic Withdrawal Strategies

Dynamic withdrawal strategies offer more flexibility than fixed rules. These methods adjust your withdrawal amount based on market performance, allowing you to take out less during down years to preserve capital and more during up years. This approach can significantly improve the longevity of your portfolio, even if it means fluctuating income year to year.

Another powerful approach is the bucket strategy, where you divide your assets into different ‘buckets’ based on their liquidity and risk profile. For example, one bucket might hold cash for immediate needs (1-2 years of expenses), another for short-term investments (3-5 years), and a third for long-term growth (5+ years). This helps ensure you have readily available funds without being forced to sell growth assets during a market downturn.

- The 4% Rule: A traditional guideline for initial withdrawal, adjusted for inflation annually.

- Dynamic Adjustments: Modifying withdrawals based on portfolio performance and market conditions.

- Bucket Strategy: Segmenting assets into short-term, mid-term, and long-term needs for better management.

- Tax-Efficient Withdrawals: Prioritizing withdrawals from different account types (taxable, tax-deferred, tax-free) to minimize tax burden.

The sequence of withdrawals from different account types (taxable, tax-deferred, tax-free) also plays a crucial role in maximizing your income. Often, it’s advisable to draw from taxable accounts first, then tax-deferred accounts (like 401(k)s and IRAs), and finally tax-free accounts (like Roth IRAs). This strategy can help manage your tax liability throughout retirement.

In essence, strategic withdrawal methods are not one-size-fits-all. They require careful planning, regular review, and a willingness to adapt to changing circumstances. By employing these advanced techniques, retirees can significantly improve their chances of bridging the 2026 retirement income gap and securing their financial future.

Optimizing Your Investment Portfolio for Income and Longevity

Beyond withdrawal strategies, the composition of your investment portfolio is paramount in addressing the 2026 retirement income gap. A well-structured portfolio can generate consistent income, grow sufficiently to outpace inflation, and withstand market fluctuations. It’s not just about accumulating wealth, but about structuring it for sustainable distribution.

Diversification remains a cornerstone of effective portfolio management. Spreading your investments across various asset classes, industries, and geographies can reduce risk and enhance returns. However, in retirement, the emphasis shifts from aggressive growth to a balance of growth, income generation, and capital preservation. This often means a careful mix of equities, fixed income, and potentially alternative investments.

Asset Allocation for Retirees

A common approach for retirees is to adopt a more conservative asset allocation as they age, reducing exposure to volatile assets like stocks and increasing allocation to more stable, income-generating assets like bonds. However, with increased life expectancies, a completely conservative portfolio might not provide enough growth to combat inflation and maintain purchasing power over 20 or 30 years of retirement. A balanced approach that still includes a reasonable allocation to growth assets is often recommended.

- Balanced Portfolio: A mix of stocks for growth and bonds for income and stability.

- Dividend Stocks: Companies that pay regular dividends can provide a consistent income stream.

- Fixed-Income Investments: Bonds, CDs, and annuities offer predictable income and capital preservation.

- Real Estate: Can provide rental income and potentially appreciate in value.

Consider income-generating assets such as dividend-paying stocks, real estate investment trusts (REITs), and high-quality bonds. Annuities can also play a role, providing a guaranteed income stream, although they come with their own set of complexities and considerations. The key is to build a portfolio that aligns with your risk tolerance, income needs, and time horizon.

Regular rebalancing is also crucial. As market conditions change, your initial asset allocation can drift. Periodically rebalancing your portfolio back to your target percentages helps maintain your desired risk level and ensures you’re not overly exposed to any single asset class. This disciplined approach is vital for overcoming the 2026 retirement income gap.

In conclusion, optimizing your investment portfolio for retirement involves a strategic balance between income generation, growth, and risk management. A thoughtful asset allocation, combined with regular rebalancing, can significantly contribute to bridging the 2026 retirement income gap and ensuring financial stability.

Exploring Non-Traditional Income Sources and Part-Time Work

For many facing the 2026 retirement income gap, traditional income sources like Social Security and investment withdrawals may not be enough. Exploring non-traditional income streams and considering part-time work can be powerful strategies to supplement your retirement funds and maintain your desired lifestyle. Retirement no longer has to be a complete cessation of work.

The gig economy has opened up numerous opportunities for retirees to leverage their skills and experience. From consulting and freelance writing to teaching online or driving for ride-sharing services, there are many ways to earn income on a flexible schedule. This not only provides additional funds but can also offer social engagement and a sense of purpose, which are important aspects of a fulfilling retirement.

Leveraging Skills and Hobbies

Think about your existing skills, hobbies, and passions. Can they be monetized? Perhaps you have a talent for crafting, gardening, or tutoring. Turning a hobby into a small business can be a rewarding way to earn extra income. The internet provides platforms for selling handmade goods, offering online courses, or providing virtual assistance. The key is to find something you enjoy that doesn’t feel like a chore.

- Consulting: Offering expertise in your former profession on a part-time basis.

- Freelancing: Utilizing skills like writing, editing, or design for various clients.

- Online Businesses: Selling products or services through e-commerce platforms.

- Part-time Employment: Seeking flexible roles that fit your retirement lifestyle.

Beyond active work, consider passive income streams. This could include rental income from a spare room or property, royalties from creative works, or even dividends from a well-structured investment portfolio that emphasizes income over growth. While these might require initial setup, they can provide ongoing income with minimal active effort.

The decision to work in retirement is a personal one, but for those facing the 2026 retirement income gap, it can be a practical and even enjoyable solution. It provides financial flexibility, allows for continued social interaction, and can keep your mind sharp. The focus should be on finding opportunities that enhance, rather than detract from, your retirement experience.

In conclusion, supplementing traditional retirement income with non-traditional sources or part-time work offers a flexible and effective way to bridge the 2026 retirement income gap. By leveraging existing skills and exploring new opportunities, retirees can enhance their financial security and overall well-being.

Adjusting Lifestyle and Managing Expenses

Even with strategic withdrawals and additional income sources, effectively bridging the 2026 retirement income gap often necessitates a careful review and adjustment of lifestyle and expenses. A realistic approach to spending can significantly impact the longevity of your retirement savings. This isn’t about deprivation, but rather about intentional and mindful spending.

Start by creating a detailed retirement budget. Track your spending for a few months to identify where your money is truly going. You might be surprised by how much is spent on discretionary items. Once you have a clear picture, look for areas where you can comfortably reduce expenses without sacrificing your quality of life. Small adjustments can add up over time.

Smart Spending and Savings Strategies

Consider downsizing your home, especially if your children have moved out and you have excess space. A smaller home often means lower property taxes, utility bills, and maintenance costs. Relocating to an area with a lower cost of living can also free up significant funds. These are major decisions, but they can have a profound impact on your financial flexibility.

- Budgeting: Creating and sticking to a realistic spending plan.

- Downsizing: Moving to a smaller home or an area with a lower cost of living.

- Healthcare Cost Management: Exploring Medicare options, supplemental insurance, and preventative care.

- Debt Reduction: Eliminating high-interest debt before or early in retirement.

Another critical area for expense management is healthcare. As mentioned earlier, healthcare costs are a significant concern for retirees. Thoroughly research Medicare options, consider supplemental insurance plans, and prioritize preventative care to minimize unexpected medical bills. Understanding your coverage and maximizing benefits can save thousands of dollars annually.

Finally, focus on eliminating debt, particularly high-interest consumer debt, before entering or early in retirement. Carrying debt reduces your disposable income and adds financial stress. A debt-free retirement provides immense peace of mind and allows your income to go further. Every dollar saved on interest is a dollar that can be used for living expenses or leisure.

In summary, adjusting your lifestyle and diligently managing expenses are crucial components of bridging the 2026 retirement income gap. By adopting smart spending habits, considering major cost-saving measures, and managing debt, retirees can significantly extend the life of their savings and enjoy a more secure future.

Proactive Planning and Regular Review

Bridging the 2026 retirement income gap is not a one-time task; it requires proactive planning and a commitment to regular review and adjustment. The financial landscape is constantly evolving, and your personal circumstances will change over time. A flexible and adaptable retirement plan is far more likely to succeed than a rigid one.

Start planning well in advance of your desired retirement date. The earlier you begin to save and strategize, the more time your investments have to grow and the more flexibility you’ll have to make adjustments. Even if you’re close to retirement, it’s never too late to refine your plan and identify areas for improvement.

The Importance of a Financial Advisor

Working with a qualified financial advisor can be one of the most valuable steps you take. An advisor can help you assess your current situation, project future needs, develop tailored withdrawal strategies, and optimize your investment portfolio. They can also provide objective guidance during market fluctuations and help you stay on track with your goals. Their expertise can be crucial in navigating the complexities of the 2026 retirement income gap.

- Early Planning: Starting retirement preparations as early as possible to maximize impact.

- Professional Guidance: Consulting a financial advisor for personalized strategies and support.

- Annual Reviews: Regularly assessing your plan, expenses, and portfolio performance.

- Estate Planning: Ensuring your assets are distributed according to your wishes and minimizing tax implications.

Schedule annual reviews of your entire retirement plan. This includes revisiting your budget, checking your investment performance, reassessing your withdrawal strategy, and re-evaluating your income sources. Life events, such as unexpected expenses or changes in health, can necessitate significant adjustments to your plan. Regular check-ups ensure your plan remains relevant and effective.

Additionally, don’t neglect estate planning. While focused on future income, ensuring your estate plan is up-to-date is a critical part of comprehensive financial security. This includes wills, trusts, and healthcare directives. Proper estate planning provides peace of mind for you and your loved ones.

In conclusion, proactive planning and consistent review are indispensable for successfully navigating the 2026 retirement income gap. By embracing a flexible approach and seeking professional guidance, you can build a resilient retirement plan that adapts to challenges and secures your financial future.

| Key Strategy | Brief Description |

|---|---|

| Assess Shortfall | Accurately calculate the difference between projected retirement income and expenses. |

| Strategic Withdrawals | Implement dynamic or bucket strategies for sustainable portfolio depletion. |

| Diversify Income | Explore part-time work or passive income sources to supplement traditional funds. |

| Manage Expenses | Create a detailed budget and consider downsizing or relocating for cost savings. |

Frequently Asked Questions About the 2026 Retirement Income Gap

The 2026 retirement income gap refers to the projected 20% shortfall between the income retirees will need to maintain their desired lifestyle and the actual income they are expected to receive from traditional sources like Social Security and pensions, combined with their current savings.

To calculate your personal gap, estimate your annual retirement expenses (housing, healthcare, leisure) and compare them to your projected annual income from Social Security, pensions, and investment withdrawals. Online retirement calculators and financial advisors can help with this assessment.

Strategic withdrawal methods are planned approaches to drawing money from retirement accounts to ensure sustainability. Examples include the 4% rule, dynamic withdrawal strategies that adjust based on market performance, and the bucket strategy which segments assets for different time horizons.

Absolutely. Engaging in part-time work or leveraging skills for consulting or freelancing can significantly supplement retirement income. It offers financial flexibility, social engagement, and often a sense of purpose, making it a valuable tool to bridge any shortfall.

It is highly recommended to review your retirement plan annually, or whenever significant life events occur. Regular reviews ensure your plan remains aligned with your financial goals, adapts to market changes, and addresses any unexpected challenges effectively.

Conclusion

The projected 20% 2026 retirement income gap presents a formidable challenge, but it is by no means insurmountable. By adopting a multi-faceted approach that combines diligent personal assessment, strategic withdrawal methods, optimized investment portfolios, diversified income streams, and prudent expense management, retirees can confidently navigate this financial landscape. Proactive planning, coupled with regular reviews and professional guidance, forms the bedrock of a secure and comfortable retirement. The future is not set in stone; with informed decisions and adaptive strategies, you can bridge the gap and secure the retirement you envision.