Navigating 2026 Small Business Healthcare Mandates: A Comprehensive Guide for Owners

Anúncios

As we approach the mid-2020s, the landscape of healthcare regulations continues to evolve, particularly for small businesses. The year 2026 is poised to bring significant changes, and proactive preparation is not just advisable, but essential for the sustained success and compliance of your enterprise. Understanding the 2026 Small Business Healthcare mandates is paramount for every owner. This comprehensive guide aims to demystify these upcoming changes, providing you with the knowledge and strategies needed to navigate the complexities and ensure your business remains compliant, competitive, and an attractive employer.

The Affordable Care Act (ACA), initially enacted in 2010, laid the groundwork for many of the current healthcare regulations. However, the healthcare environment is dynamic, with ongoing legislative adjustments, market shifts, and evolving societal expectations. The 2026 mandates are not just minor tweaks; they represent a potential reshaping of how small businesses approach employee health benefits, compliance, and overall financial planning. Ignoring these changes could lead to significant penalties, increased operational costs, and a decline in employee morale.

Anúncios

This article will delve into the specifics of what small business owners need to know, from the core legislative changes to the practical steps for implementation. We will explore the potential financial impacts, the importance of employee communication, and how to leverage professional resources to ease the transition. Our goal is to equip you with a robust understanding of the 2026 Small Business Healthcare landscape, transforming potential challenges into opportunities for growth and stability.

Anúncios

The Evolving Landscape: Why 2026 Matters for Small Business Healthcare

The year 2026 isn’t just another year on the calendar; it marks a critical juncture for small business healthcare. Several factors converge to make this period particularly significant. Firstly, the ongoing debates and reforms surrounding the ACA continue to influence future legislation. While the core tenets of the ACA may remain, specific provisions, subsidies, and employer responsibilities are subject to revision. These revisions often aim to address perceived shortcomings, improve access, or control costs, but they inevitably create new compliance hurdles for businesses.

Secondly, the economic climate and workforce demographics play a crucial role. A competitive job market often necessitates attractive benefits packages, with healthcare being a top priority for many employees. Small businesses, often competing with larger corporations for talent, must offer competitive healthcare options to recruit and retain skilled workers. The 2026 Small Business Healthcare mandates could influence the affordability and structure of these packages.

Thirdly, technological advancements and data privacy concerns are increasingly shaping healthcare policy. The secure handling of protected health information (PHI) and the integration of digital health solutions are areas likely to see enhanced regulation. Small businesses must be prepared to adapt their data management practices to meet these evolving standards.

Finally, state-level initiatives often precede or supplement federal mandates. While this guide focuses on federal changes, it’s vital for small business owners to also remain aware of any specific healthcare reforms or requirements enacted within their respective states, as these can add additional layers of complexity to the 2026 Small Business Healthcare compliance puzzle.

Key Legislative Changes and Their Impact on Small Businesses

While the exact legislative text for 2026 may still be under development, based on current trends and discussions, several key areas are likely to see significant changes or increased scrutiny. Understanding these potential shifts is the first step in proactive planning for 2026 Small Business Healthcare.

Expanded Employer Mandates and Reporting Requirements

One of the most impactful aspects of the ACA for larger employers has been the employer mandate, requiring businesses with 50 or more full-time equivalent employees (FTEs) to offer affordable, minimum essential coverage. While small businesses (those with fewer than 50 FTEs) have historically been exempt from this mandate, there’s always a possibility of adjustments to these thresholds or the introduction of new reporting requirements that could indirectly affect smaller entities. Even if the direct mandate doesn’t expand, increased scrutiny on employee classification (full-time vs. part-time) or new data collection mandates could add administrative burdens.

For businesses already subject to the employer mandate, expect more stringent enforcement and potentially revised definitions of what constitutes "affordable" coverage. The affordability percentage, which dictates the maximum percentage of an employee’s household income that they can be required to contribute towards premiums, is periodically adjusted and could see changes that impact plan design and employer contributions.

Changes to Subsidies and Tax Credits

The ACA included premium tax credits to help individuals and families afford health insurance purchased through the marketplaces. These subsidies have been subject to temporary enhancements in recent years. For 2026, there could be revisions to the eligibility criteria, the amount of the subsidies, or their duration. While primarily affecting individuals, these changes can indirectly impact small businesses. If subsidies become less generous, employees might seek more comprehensive or affordable options through their employers, placing greater pressure on businesses to offer competitive plans. Conversely, if subsidies expand, some employees might opt for marketplace plans, potentially reducing demand for employer-sponsored coverage.

New Regulations on Health Plan Design and Benefits

Healthcare policy is continually evolving to address new medical technologies, public health concerns, and patient needs. For 2026, we could see new regulations influencing health plan design for 2026 Small Business Healthcare. This might include:

- Mental Health Parity: Continued emphasis on ensuring mental health and substance use disorder benefits are covered at parity with medical and surgical benefits. Small businesses should review their plans to ensure full compliance.

- Prescription Drug Costs: Potential new measures to regulate prescription drug pricing or increase transparency, which could affect plan costs and formulary design.

- Telehealth Services: Further integration and regulation of telehealth and remote care services, which gained significant traction during the pandemic. Plans may be required to cover a broader range of virtual services.

- Preventive Care: Continued or expanded requirements for coverage of preventive services without cost-sharing.

Data Privacy and Security Enhancements

With the increasing digitization of health records and the rise of cyber threats, expect heightened focus on data privacy and security. Small businesses that handle employee health information, even indirectly through benefits administration, will need to ensure robust compliance with HIPAA (Health Insurance Portability and Accountability Act) and potentially new state or federal privacy regulations. This includes securing electronic health records, training staff on data protection, and having protocols for breach notification.

Financial Implications and Cost Management Strategies

The financial impact of healthcare mandates is often the primary concern for small business owners. The 2026 Small Business Healthcare changes could lead to increased premium costs, administrative expenses, or penalties for non-compliance. Strategic financial planning is crucial to mitigate these impacts.

Understanding Rising Premium Costs

Healthcare premiums have been on an upward trajectory for years, driven by factors such as medical inflation, new technologies, and an aging population. The 2026 mandates could exacerbate these increases through new coverage requirements or administrative burdens. Small businesses need to budget for these potential increases and explore various plan options.

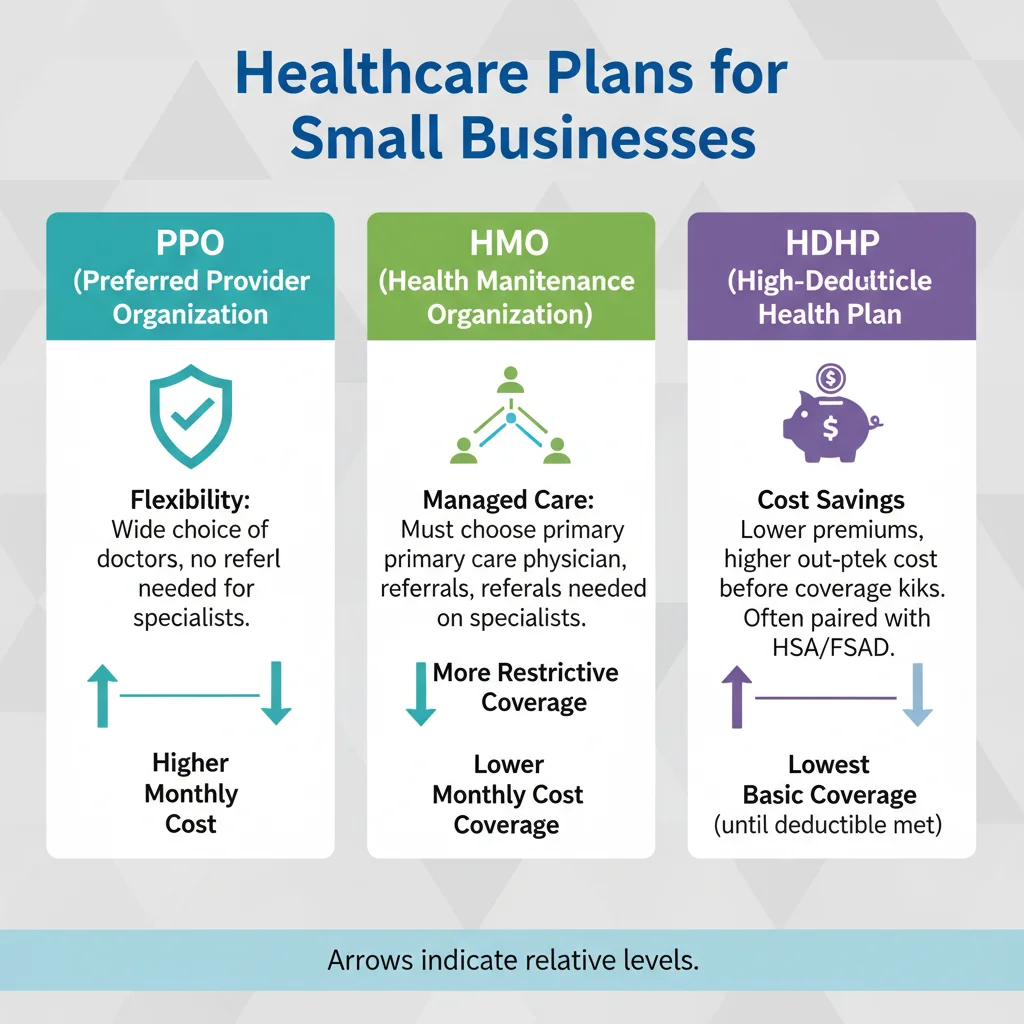

Exploring Different Health Plan Structures

To manage costs, small businesses should explore a range of health plan structures beyond traditional PPOs (Preferred Provider Organizations) and HMOs (Health Maintenance Organizations). Options include:

- High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs): These plans typically have lower premiums and allow employees to save pre-tax money for healthcare expenses. They can be a cost-effective option for both employers and employees.

- Self-Funded Plans: For larger small businesses, self-funding (where the employer pays for claims directly) can offer greater control over costs, though it also carries more risk. Stop-loss insurance can mitigate catastrophic claims.

- Level-Funded Plans: A hybrid approach, offering the cost control of self-funding with the predictability of fully insured plans.

- Health Reimbursement Arrangements (HRAs) and Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs): These allow employers to reimburse employees for healthcare expenses, including premiums, on a tax-free basis. QSEHRAs are specifically designed for small businesses not offering group health plans.

Leveraging Small Business Health Options Program (SHOP)

The ACA established the Small Business Health Options Program (SHOP) Marketplace, designed to help small employers (generally those with 1-50 employees) offer health and dental coverage to their employees. While participation has varied, 2026 might bring renewed focus or enhancements to SHOP, making it a more viable option for some businesses seeking competitive rates and streamlined administration for their 2026 Small Business Healthcare needs.

Tax Credits for Small Employers

Don’t forget the small business health care tax credit. Eligible small employers (generally those with fewer than 25 full-time equivalent employees, paying average annual wages below a certain threshold, and contributing at least 50% of employee premium costs) may qualify for a tax credit to offset premium expenses. Reviewing eligibility for this credit is an important part of cost management.

Controlling Administrative Costs

Compliance with new mandates often means increased administrative burden. Consider investing in HR software or partnering with a Professional Employer Organization (PEO) to streamline benefits administration, payroll, and compliance tasks. These services can help manage the complexities of 2026 Small Business Healthcare regulations, saving time and reducing the risk of errors.

Compliance Checklist for 2026 Small Business Healthcare Mandates

Proactive compliance is key to avoiding penalties and ensuring a smooth transition. Here’s a checklist to guide your preparation for the 2026 Small Business Healthcare mandates:

- Review Employee Count: Regularly assess your full-time equivalent (FTE) employee count to determine if you meet any thresholds for employer mandates.

- Audit Current Health Plans: Evaluate your existing health insurance plans against potential new requirements for coverage, affordability, and minimum value.

- Stay Informed on Legislation: Designate someone (or subscribe to professional services) to monitor federal and state legislative updates regarding healthcare.

- Assess Affordability: Calculate the affordability of your current plans based on potential revised affordability percentages.

- Update Data Security Protocols: Ensure your practices for handling employee health information comply with HIPAA and any new data privacy regulations. Conduct regular security audits.

- Educate Your Team: Inform key personnel (HR, finance, management) about upcoming changes and their responsibilities.

- Budget for Changes: Incorporate potential increases in premium costs, administrative fees, or compliance tools into your financial forecasts.

- Consult with Experts: Engage with benefits brokers, HR consultants, or legal counsel specializing in healthcare compliance.

- Explore Alternative Solutions: Research and evaluate different health plan structures (HDHPs, HRAs, self-funded, level-funded) to find the most suitable and cost-effective options for your business.

- Prepare Communication Strategy: Develop a plan to effectively communicate changes to your employees well in advance.

Communicating Changes to Your Employees

Effective communication is a cornerstone of successful implementation for any significant change, especially concerning employee benefits. The 2026 Small Business Healthcare mandates will likely impact your employees, and transparent, clear communication can prevent confusion, reduce anxiety, and maintain morale.

Transparency and Clarity

When communicating changes, be as transparent as possible about why the changes are occurring (e.g., "due to new federal regulations effective in 2026"), what the changes entail, and how they will specifically affect employees. Avoid jargon and explain complex terms simply.

Provide Ample Notice

Give employees plenty of advance notice about upcoming changes. This allows them time to understand the new plans, ask questions, and make informed decisions, especially if they need to choose new plans or make adjustments to their healthcare spending.

Offer Resources and Support

Don’t just announce changes; provide resources to help employees understand them. This could include:

- Information Sessions: Host meetings (in-person or virtual) where employees can learn about the changes and ask questions.

- Written Materials: Distribute clear, concise summaries of new plans, FAQs, and contact information for benefits administrators.

- One-on-One Consultations: Offer opportunities for employees to discuss their specific situations with HR or a benefits expert.

- Decision-Making Tools: Provide tools or guidance that help employees compare new plan options and understand their costs and benefits.

Address Concerns Proactively

Anticipate common questions and concerns employees might have (e.g., "Will my doctor still be in-network?" "Will my prescription costs change?") and address them in your communications. Acknowledge that changes can be unsettling and emphasize your commitment to supporting their healthcare needs.

Highlight the Positives

If any new mandates or plan changes introduce improved benefits, expanded coverage, or new support programs, highlight these positives. Frame the changes in a way that shows how the business is adapting to continue providing valuable benefits, even in the face of evolving regulations for 2026 Small Business Healthcare.

Leveraging Professional Resources and Technology

Navigating the complexities of 2026 Small Business Healthcare mandates doesn’t have to be a solo endeavor. A wealth of professional resources and technological solutions can significantly ease the burden of compliance and administration.

Benefits Brokers and Consultants

These professionals specialize in the healthcare market and can provide invaluable assistance. They can:

- Stay Up-to-Date: Keep you informed about the latest legislative changes and market trends.

- Plan Design: Help you design benefit packages that meet compliance requirements, employee needs, and your budget.

- Negotiate Rates: Leverage their relationships with carriers to secure competitive rates.

- Compliance Support: Advise on reporting requirements and help ensure your plans meet all regulatory standards.

HR and Payroll Software

Modern HR and payroll software platforms often include robust benefits administration modules. These systems can:

- Automate Enrollment: Streamline the open enrollment process and manage employee elections.

- Track Eligibility: Automatically track employee eligibility for benefits based on hours worked and other criteria.

- Generate Reports: Produce necessary compliance reports (e.g., ACA reporting forms) efficiently.

- Integrate Data: Connect with payroll and other HR functions to ensure accurate data flow and reduce manual errors.

Professional Employer Organizations (PEOs)

Partnering with a PEO means co-employing your workforce. The PEO handles many HR functions, including payroll, benefits administration, and compliance. For small businesses, this can be a game-changer for 2026 Small Business Healthcare compliance. PEOs often offer:

- Access to Better Benefits: Due to their larger client pool, PEOs can often offer small businesses access to a wider range of high-quality, more affordable health plans, typically reserved for larger companies.

- Compliance Expertise: PEOs have dedicated compliance teams that stay abreast of all federal and state regulations, ensuring your business meets all necessary mandates.

- Reduced Administrative Burden: They take on the administrative tasks associated with benefits, freeing up your time and resources.

Legal Counsel

For complex situations or when interpreting ambiguous regulations, consulting with an attorney specializing in healthcare law or employment law is crucial. Legal counsel can provide tailored advice, review contracts, and help mitigate legal risks associated with 2026 Small Business Healthcare mandates.

Long-Term Strategic Planning for Small Business Healthcare

Beyond immediate compliance, the 2026 Small Business Healthcare mandates should prompt a broader, long-term strategic review of your employee benefits philosophy. Healthcare is a critical component of employee attraction and retention, and a thoughtful approach can yield significant competitive advantages.

Holistic Benefits Strategy

Consider healthcare as part of a holistic benefits package. How do your health plans integrate with other offerings like retirement plans, paid time off, wellness programs, and professional development? A well-rounded package demonstrates your commitment to employee well-being and can differentiate your business in the talent market.

Focus on Employee Wellness

Investing in employee wellness programs can have a dual benefit: improving employee health and potentially reducing long-term healthcare costs. Wellness initiatives, from encouraging physical activity to promoting mental health resources, can lead to a healthier, more productive workforce. This proactive approach can be particularly beneficial as you adapt to 2026 Small Business Healthcare changes.

Regular Review and Adaptation

The healthcare landscape is continuously shifting. Establish a routine for annually reviewing your health plans, assessing their effectiveness, and ensuring ongoing compliance. Be prepared to adapt your strategy as new legislation emerges or as your business grows and its needs change. This continuous cycle of review and adaptation will be vital for managing 2026 Small Business Healthcare and beyond.

Employee Feedback and Engagement

Regularly solicit feedback from your employees regarding their healthcare benefits. Surveys, focus groups, or informal discussions can provide valuable insights into what your employees value most, where there are gaps, and how satisfied they are with current offerings. This feedback can inform your strategic decisions and help you tailor benefits that truly meet their needs, fostering a sense of ownership and appreciation.

Conclusion: Proactive Steps for a Healthy Future

The 2026 Small Business Healthcare mandates represent a significant moment for business owners. While the specifics are still unfolding, the overarching message is clear: proactive engagement, informed decision-making, and strategic planning are indispensable. By understanding the potential legislative changes, assessing financial implications, and leveraging available resources, small businesses can not only meet compliance requirements but also enhance their ability to attract and retain top talent.

Don’t wait until the last minute. Begin your preparation today by reviewing your current plans, consulting with experts, and communicating openly with your employees. Embrace the changes as an opportunity to refine your benefits strategy, ensuring your business remains resilient, compliant, and continues to be a great place to work. A well-prepared small business is a healthy business, ready to face the future with confidence and continued success in the evolving world of healthcare.