American Opportunity Tax Credit 2026: Maximize Your $2,500 Education Refund

Anúncios

Higher education in the United States represents a significant investment, often accompanied by substantial financial burdens. Fortunately, the U.S. government offers various tax benefits to help offset these costs, with the American Opportunity Tax Credit (AOTC) being one of the most impactful. For the 2026 tax year, the AOTC continues to be a crucial resource for students and families, potentially putting up to $2,500 back into their pockets. Understanding the intricacies of the AOTC 2026 is paramount for anyone navigating college expenses.

This comprehensive guide delves into everything you need to know about the American Opportunity Tax Credit for the 2026 tax year. From eligibility requirements and qualified expenses to claiming the credit and maximizing your refund, we’ll provide a detailed roadmap to ensure you don’t miss out on this valuable financial aid. Whether you’re a student, a parent, or a tax professional, mastering the AOTC 2026 can lead to significant savings.

Anúncios

What is the American Opportunity Tax Credit (AOTC)?

The American Opportunity Tax Credit (AOTC) is a partially refundable tax credit designed to help students and their families pay for higher education expenses. It provides a credit of up to $2,500 per eligible student for qualified education expenses paid for the first four years of postsecondary education. What makes the AOTC particularly attractive is its refundable component: up to 40% of the credit (or $1,000) can be received as a tax refund, even if you owe no taxes.

Anúncios

Initially enacted as part of the American Recovery and Reinvestment Act of 2009, the AOTC has been extended multiple times due to its effectiveness in supporting educational pursuits. It replaced and expanded upon the Hope Credit, offering a more generous credit amount and wider applicability for a longer duration of study. The AOTC 2026 provisions are expected to remain consistent with previous years, offering stable support for educational funding.

Key Features of the AOTC:

- Maximum Credit: Up to $2,500 per eligible student per year.

- Refundable Portion: Up to 40% of the credit (or $1,000) can be refundable. This means if the credit reduces your tax liability to zero, you could still get up to $1,000 back as a refund.

- Duration: Available for the first four years of postsecondary education.

- Calculation: The credit is 100% of the first $2,000 of qualified education expenses and 25% of the next $2,000 of qualified education expenses.

Understanding these fundamental aspects is the first step toward leveraging the AOTC 2026 to its fullest potential. It’s crucial to distinguish it from other education credits like the Lifetime Learning Credit, as you can only claim one per student per year.

Eligibility Requirements for the AOTC 2026

To claim the AOTC 2026, both the student and the educational program must meet specific criteria set by the IRS. Failing to meet even one of these requirements can disqualify you from receiving the credit. Therefore, a thorough review of these conditions is essential.

Student Eligibility:

- Enrollment: The student must be pursuing a degree or other recognized educational credential. This includes undergraduate degrees, associate degrees, and vocational certificates.

- Enrollment Status: The student must be enrolled at least half-time for at least one academic period beginning in the tax year. The definition of "half-time" is determined by the educational institution.

- Academic Level: The student must be in their first four years of higher education (i.e., they have not completed the first four years of postsecondary education before the beginning of the tax year). This means they haven’t completed four years of college-level study.

- Prior AOTC Claims: The student must not have claimed the AOTC or the former Hope Credit for more than four tax years.

- Felony Drug Conviction: The student must not have a felony drug conviction on their record for the tax year.

Educational Institution Eligibility:

The educational institution must be an eligible educational institution. This generally includes any accredited public, nonprofit, or proprietary (privately-owned, for-profit) postsecondary institution eligible to participate in a student aid program administered by the U.S. Department of Education. This includes most colleges, universities, and vocational schools.

Income Limitations for the AOTC 2026:

The AOTC 2026 is subject to income phase-outs, meaning your adjusted gross income (AGI) can affect the amount of credit you can claim. For the 2026 tax year, the income thresholds are generally:

- Married Filing Jointly: The credit begins to phase out for taxpayers with a modified AGI between $160,000 and $180,000.

- Single, Head of Household, or Qualifying Widow(er): The credit begins to phase out for taxpayers with a modified AGI between $80,000 and $90,000.

If your modified AGI falls within these ranges, the amount of your AOTC will be reduced. If your AGI exceeds the upper limit, you will not be eligible to claim the credit. It’s important to note that these figures are subject to annual adjustments by the IRS, so always refer to the latest IRS publications for the most accurate and up-to-date information for the AOTC 2026.

Qualified Education Expenses for the AOTC 2026

One of the most common areas of confusion when claiming education credits is determining which expenses qualify. The IRS has specific guidelines for what can be included when calculating the AOTC 2026. Generally, these expenses must be for education furnished during an academic period beginning in the tax year, or in the first three months of the next tax year if the payment is made in the current tax year.

What Qualifies:

- Tuition and Fees: These are the primary qualifying expenses. They include amounts paid for enrollment or attendance at an eligible educational institution.

- Course-Related Books, Supplies, and Equipment: This category includes expenses for books, supplies, and equipment needed for a course of study, even if not purchased directly from the educational institution. This is a significant advantage of the AOTC over some other education benefits.

What Does NOT Qualify:

- Living Expenses: Room and board, insurance, medical expenses (including student health fees), transportation, and similar personal, living, or family expenses are not qualified education expenses.

- Non-Credit Courses: Expenses for courses involving sports, games, or hobbies unless the course is part of the student’s degree program.

- Payments for Services: Payments for services such as athletic fees, even if required for enrollment, are generally not qualified expenses unless they cover a specific educational activity.

- Payments from Tax-Free Assistance: Expenses paid with tax-free scholarship money, grants, or employer-provided educational assistance do not qualify. You can only claim expenses paid "out of pocket" or with taxable student loans.

It’s crucial to keep meticulous records of all your educational expenses, including receipts for tuition payments, book purchases, and any other qualifying items. This documentation will be vital if the IRS ever questions your claim for the AOTC 2026.

How to Claim the American Opportunity Tax Credit 2026

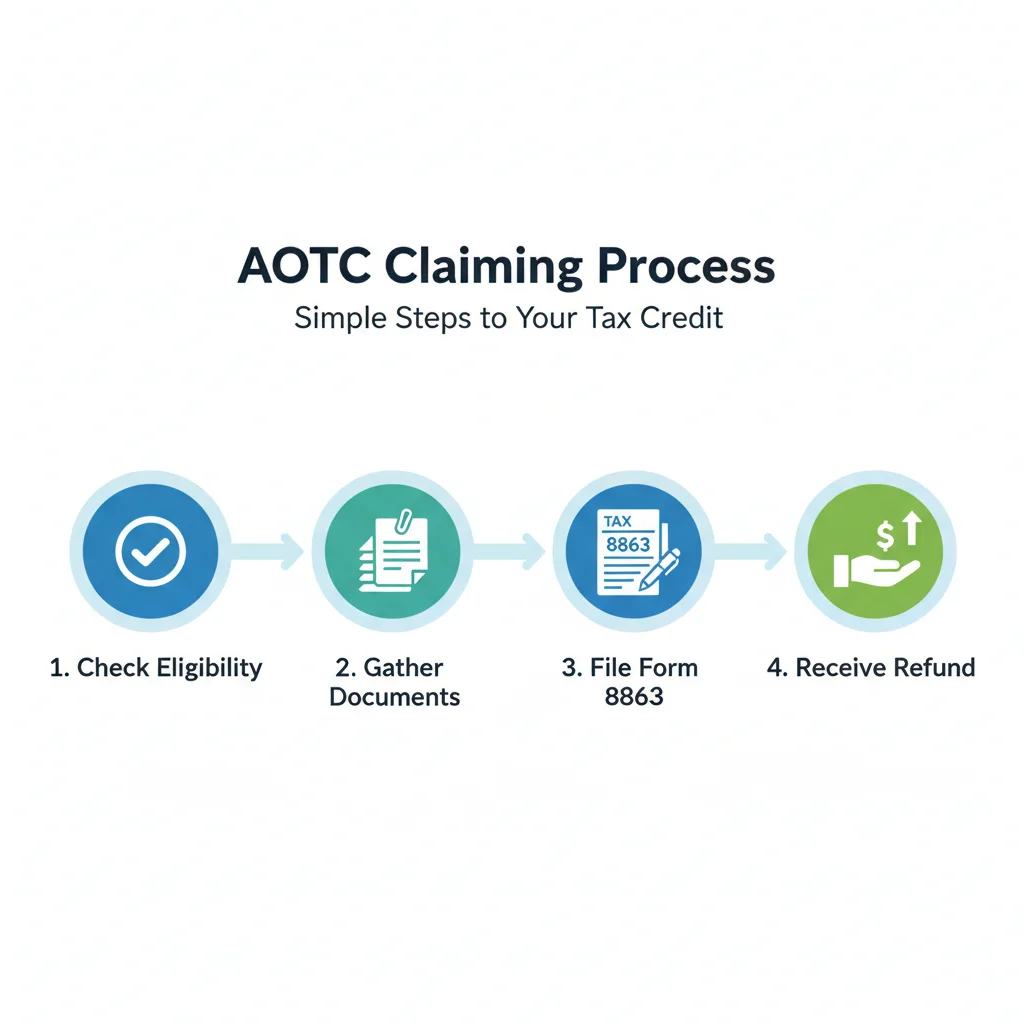

Claiming the AOTC 2026 involves several steps, primarily centered around filing your federal income tax return. The process requires careful attention to detail to ensure you receive the maximum benefit you’re entitled to.

Step-by-Step Guide to Claiming AOTC:

- Receive Form 1098-T: Your educational institution should provide you with Form 1098-T, Tuition Statement, by January 31st of the year following the tax year for which you are claiming the credit. This form reports the amounts billed or paid for qualified tuition and related expenses. While Form 1098-T is a good starting point, remember that the amount reported may not always reflect all your qualified expenses (e.g., books purchased elsewhere).

- Gather All Relevant Documentation: Collect all receipts for tuition and fees, books, supplies, and equipment. Also, keep records of any scholarships, grants, or other tax-free educational assistance received.

- Determine Eligibility: Review all student, program, and income eligibility requirements discussed earlier to ensure you qualify for the AOTC 2026.

- Complete Form 8863, Education Credits (American Opportunity and Lifetime Learning Credits): This is the form you’ll use to calculate and claim the AOTC. You will need to enter information from your Form 1098-T and your records of other qualified expenses.

- Attach Form 8863 to Your Federal Income Tax Return: Once completed, Form 8863 is submitted along with your Form 1040 (or 1040-SR).

Who Claims the Credit?

Generally, either the student or the person who claims the student as a dependent can claim the AOTC 2026, but not both. If the student is claimed as a dependent on someone else’s tax return, only the person claiming the student as a dependent can claim the AOTC. If the student is not claimed as a dependent, they can claim the credit themselves. It’s crucial for families to coordinate to avoid duplicate claims, which can lead to complications with the IRS.

Important Considerations for Filing:

- Social Security Number (SSN): The student must have a valid SSN or Individual Taxpayer Identification Number (ITIN) to claim the credit.

- Timeliness: Ensure all necessary forms are filed by the tax deadline.

- Professional Help: If your situation is complex, consider consulting a tax professional to ensure accurate filing and maximum benefit.

Maximizing Your AOTC 2026 Benefit

While the basic framework of the AOTC is straightforward, there are several strategies and nuances that can help you maximize the benefit you receive for the AOTC 2026.

Coordination with Other Education Benefits:

You cannot claim both the AOTC and the Lifetime Learning Credit for the same student in the same year. You also cannot claim the AOTC for a student for whom you are claiming the Tuition and Fees Deduction (though this deduction is often less beneficial than the AOTC). Carefully evaluate which credit offers the greatest financial advantage. The AOTC is generally more generous due to its higher maximum and refundable portion, especially during the first four years of study.

Furthermore, if you receive tax-free educational assistance (like scholarships or grants), these funds reduce the amount of qualified expenses you can use for the AOTC. However, if you have a choice, you might strategically use tax-free aid to cover non-qualified expenses (like room and board) first, leaving more "out-of-pocket" qualified expenses for the AOTC.

Timing of Payments:

Qualified education expenses are generally those paid during the tax year for an academic period beginning in that tax year or in the first three months of the next tax year. If you pay for next semester’s tuition in December, those expenses can often count for the current tax year’s AOTC. Strategic timing of payments, when possible, can sometimes shift the credit to a year where it might be more beneficial (e.g., if income levels are different).

Student Status and Dependency:

As mentioned, only one person can claim the AOTC for an eligible student. If a student is a dependent, the parent or guardian claims the credit. If the student is not a dependent (e.g., they are over 24, support themselves, or don’t live with parents for more than half the year), they can claim the credit themselves. Discuss this within the family to determine who will benefit most, considering each party’s income level and tax liability. A student with low income might benefit greatly from the refundable portion of the AOTC 2026.

Record Keeping:

Maintain meticulous records. This includes:

- Form 1098-T from the educational institution.

- Receipts for all tuition and fee payments.

- Receipts for books, supplies, and equipment required for courses.

- Records of scholarships, grants, and other financial aid received.

- Bank statements or cancelled checks showing payments made.

Adequate record-keeping is your best defense in case of an IRS audit and ensures you don’t overlook any eligible expenses when calculating your AOTC 2026.

AOTC vs. Lifetime Learning Credit: Which One for 2026?

While both the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) help with education expenses, they serve different purposes and have distinct eligibility requirements. Understanding these differences is key to choosing the right credit for your situation for the AOTC 2026.

Key Differences:

- AOTC: Available for the first four years of postsecondary education, requires enrollment at least half-time, and is partially refundable (up to $1,000). Maximum credit is $2,500.

- Lifetime Learning Credit (LLC): Available for any year of postsecondary education, including graduate school and courses taken to acquire job skills. No "first four years" limit or half-time enrollment requirement. It is non-refundable, meaning it can reduce your tax liability to zero but won’t result in a refund. Maximum credit is $2,000 (20% of the first $10,000 in qualified expenses).

When to Choose AOTC for 2026:

The AOTC 2026 is generally more beneficial if the student is in their first four years of an undergraduate degree program, enrolled at least half-time, and has significant qualified expenses (at least $4,000 to maximize the credit). Its refundable portion is a major advantage for those with lower tax liabilities.

When to Choose Lifetime Learning Credit:

The LLC is suitable for graduate students, students taking a few courses (even less than half-time), or those pursuing job skills training. It’s also an option if the student has already claimed the AOTC for four years. While less generous, it offers flexibility for a wider range of educational pursuits.

You cannot claim both credits for the same student in the same tax year. Therefore, it’s crucial to compare the potential benefits of each based on your specific circumstances for the AOTC 2026.

Common Pitfalls and How to Avoid Them with AOTC 2026

Despite its benefits, claiming the AOTC can present challenges. Being aware of common pitfalls can help you navigate the process smoothly and avoid issues with the IRS.

1. Incorrectly Calculating Qualified Expenses:

Pitfall: Including non-qualified expenses like room and board, transportation, or health insurance. Also, forgetting to subtract tax-free aid from qualified expenses.

Solution: Refer strictly to IRS Publication 970 for what constitutes "qualified education expenses." Keep separate, detailed records for tuition/fees and books/supplies, and clearly differentiate these from living expenses. Always deduct any tax-free aid received from your total qualified expenses before calculating the credit.

2. Exceeding the Four-Year Limit:

Pitfall: Attempting to claim the AOTC for a student who has already completed four years of postsecondary education or has claimed the Hope/AOTC for four prior tax years.

Solution: Track the number of years the AOTC (or Hope Credit) has been claimed for the student. The IRS systems track this, and an incorrect claim will likely result in a denial or audit.

3. Not Meeting Half-Time Enrollment:

Pitfall: Claiming the AOTC for a student who was not enrolled at least half-time for at least one academic period during the tax year.

Solution: Verify the student’s enrollment status with the educational institution. "Half-time" definition can vary by school but is usually clearly stated on academic records.

4. Income Phase-Out Miscalculation:

Pitfall: Claiming the full credit when your modified AGI exceeds the phase-out limits, or failing to realize you are completely phased out.

Solution: Accurately calculate your modified AGI. Use the IRS guidelines for the AOTC 2026 income limits (which will be published closer to the tax year) to determine if your credit amount needs to be reduced or if you are ineligible.

5. Lack of Documentation:

Pitfall: Not keeping adequate records of expenses and payments, making it difficult to justify your claim if audited.

Solution: As reiterated, maintain meticulous records. This includes Form 1098-T, receipts for all qualifying expenses, and documentation of financial aid. Store these securely for at least three years (the standard IRS audit period).

6. Duplicate Claims:

Pitfall: Both the student and the parent (or another taxpayer) attempting to claim the AOTC for the same student in the same year.

Solution: Coordinate within the family. Determine who can claim the student as a dependent and, consequently, who will claim the AOTC 2026 to maximize the family’s overall tax benefit. Only one person can claim the credit per student.

7. Incorrect Social Security Number (SSN):

Pitfall: The student claiming the credit does not have a valid SSN or ITIN, or an incorrect number is entered on the tax form.

Solution: Ensure the student has a valid SSN or ITIN. Double-check all numbers entered on Form 8863 to prevent processing delays or denials.

The Future of Education Tax Credits Beyond AOTC 2026

While this guide focuses on the AOTC 2026, it’s worth considering the broader landscape of education tax benefits. Tax laws are subject to change, and future legislative actions could impact the availability or structure of these credits. Historically, there have been discussions and proposals for simplifying education tax benefits, but the AOTC has consistently remained a cornerstone due to its effectiveness.

For the foreseeable future, the AOTC is expected to continue providing vital support for students pursuing higher education. However, staying informed about tax law changes through official IRS announcements and reputable financial news sources is always advisable. This proactive approach ensures you can adapt your financial planning to any modifications in tax credits and deductions.

Conclusion: Harnessing the Power of the AOTC 2026

The American Opportunity Tax Credit for 2026 is a powerful tool for making higher education more affordable. With a potential credit of up to $2,500 per eligible student, including a refundable portion of up to $1,000, it can significantly reduce the financial burden of college tuition, fees, books, and supplies.

By carefully understanding the eligibility requirements, identifying qualified expenses, meticulously maintaining records, and correctly filing Form 8863, students and families can successfully claim this valuable credit. Remember to coordinate claims, consider income limitations, and choose the most beneficial education credit for your specific situation.

Don’t let the complexities of tax law deter you. The effort invested in understanding and claiming the AOTC 2026 can result in substantial savings, freeing up resources that can be better used for academic success and future endeavors. Make sure to consult the most current IRS publications or a qualified tax professional for personalized advice, ensuring you fully capitalize on this essential educational financial aid.