Federal Interventions 2026: Stabilizing the Housing Market

Anúncios

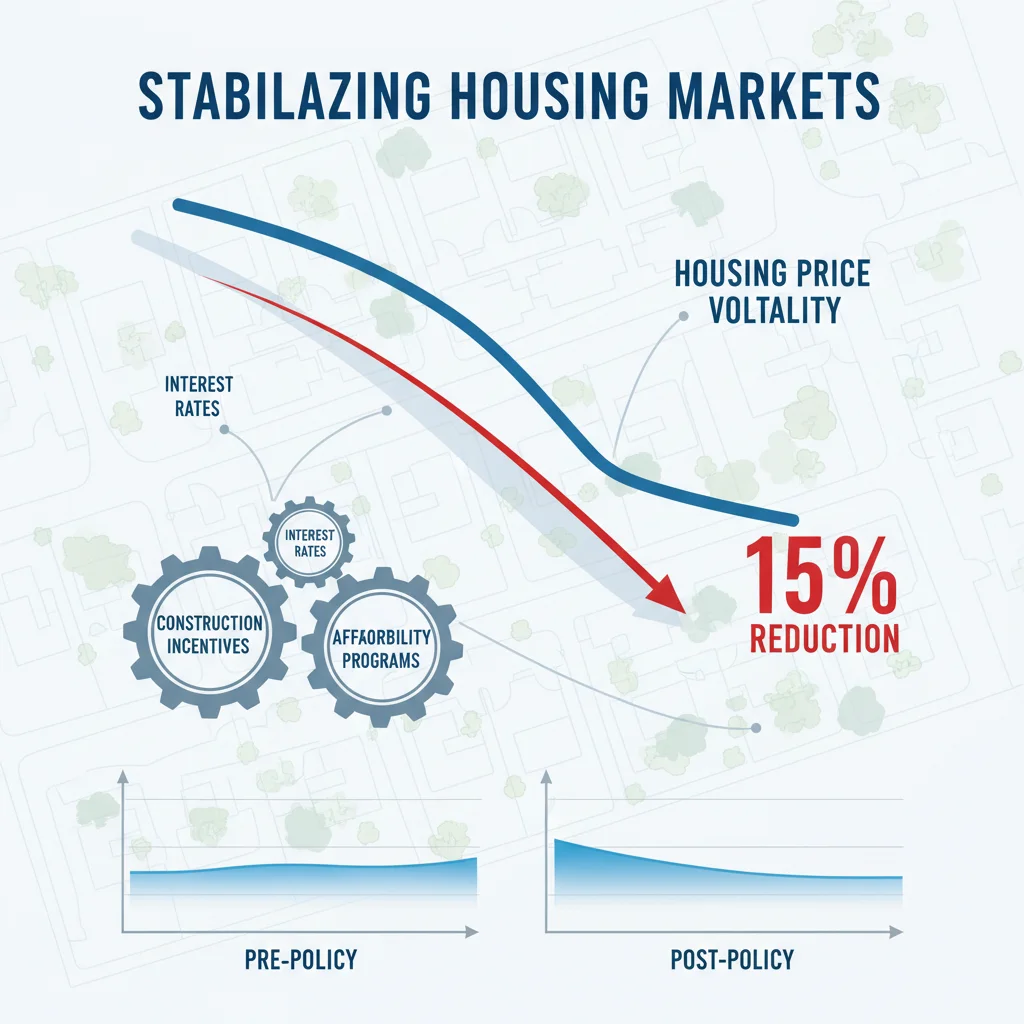

The American dream of homeownership has, for many, become an increasingly elusive aspiration. Over the past decade, the housing market has been characterized by periods of intense volatility, rapid price appreciation, and affordability crises that have disproportionately impacted low- and middle-income families. Recognizing the profound economic and social implications of an unstable housing market, the federal government is set to introduce a series of comprehensive interventions in 2026. The ambitious goal? To achieve significant housing market stabilization, specifically targeting a 15% reduction in national price volatility. This article delves deep into the anticipated federal strategies, their potential impact, and the broader implications for the future of housing in the United States.

Understanding the current landscape is crucial before exploring the proposed solutions. The housing market is a complex ecosystem influenced by a myriad of factors, including interest rates, supply and demand dynamics, population growth, economic health, and even global events. Recent years have seen a confluence of these factors create a perfect storm: historically low interest rates fueled demand, while supply struggled to keep pace due to labor shortages, material costs, and restrictive zoning laws. This imbalance led to unprecedented price surges, making homeownership unattainable for many and exacerbating wealth inequality. The federal government’s planned interventions in 2026 represent a concerted effort to recalibrate this imbalance and foster genuine housing market stabilization.

Anúncios

The Genesis of Federal Intervention: Why 2026?

The decision to implement significant federal interventions in 2026 is not arbitrary. It stems from a confluence of factors, including extensive economic analysis, demographic projections, and a growing consensus that the current trajectory of the housing market is unsustainable. Experts predict that without decisive action, housing affordability will continue to deteriorate, potentially triggering broader economic instability. The target of a 15% reduction in national price volatility is a carefully calculated figure, aiming to cool down overheated markets without causing a drastic downturn that could harm existing homeowners. This nuanced approach underscores the complexity of achieving true housing market stabilization.

Furthermore, the 2026 timeline allows for adequate planning, legislative processes, and the necessary coordination among various federal agencies, state governments, and private sector stakeholders. Crafting policies that are both effective and equitable requires careful consideration of regional differences, economic conditions, and the diverse needs of communities across the nation. The federal government aims to learn from past housing crises and policy missteps, ensuring that the 2026 interventions are robust, adaptable, and designed for long-term housing market stabilization.

Anúncios

Key Pillars of the 2026 Federal Housing Strategy

The proposed federal interventions are expected to be multi-faceted, addressing both the supply and demand sides of the housing equation, while also focusing on regulatory reforms and financial assistance programs. The overarching goal remains housing market stabilization through a holistic approach.

1. Boosting Housing Supply and Construction Incentives

One of the most significant contributors to price volatility has been the chronic shortage of housing supply. The federal government plans to tackle this head-on with a range of initiatives:

- Streamlined Zoning and Land-Use Policies: Encouraging states and municipalities to reform restrictive zoning laws that limit density and increase development costs. This could include federal grants or incentives for cities that adopt more permissive zoning for multi-family housing and mixed-use developments.

- Increased Funding for Affordable Housing Development: Significant investment in programs like the Low-Income Housing Tax Credit (LIHTC) and other direct subsidies for developers building affordable housing units. This aims to stimulate construction in areas with critical shortages and promote housing market stabilization.

- Support for Innovative Construction Technologies: Investing in research and development for modular construction, 3D-printed homes, and other cost-effective building methods that can accelerate construction timelines and reduce labor costs.

- Workforce Development for Construction Trades: Addressing labor shortages in the construction industry through federal funding for vocational training programs, apprenticeships, and initiatives to attract new talent to the sector.

- Federal Land Utilization: Identifying and making available suitable federal land for residential development, particularly in high-demand areas, to increase supply.

2. Enhancing Affordability and Access for Homebuyers

Beyond increasing supply, the federal plan will focus on making homeownership more accessible and affordable, directly contributing to housing market stabilization:

- First-Time Homebuyer Assistance Programs: Expanding down payment assistance, closing cost grants, and favorable loan terms for eligible first-time homebuyers, particularly those in underserved communities.

- Mortgage Interest Rate Stabilization Mechanisms: While direct manipulation of interest rates is typically the purview of the Federal Reserve, the government may explore mechanisms to buffer homebuyers from extreme rate fluctuations, perhaps through specific loan programs or subsidies that absorb some of the volatility.

- Rental Assistance and Tenant Protections: Recognizing that a stable rental market is intrinsically linked to housing market stability, the plan may include expanded rental assistance programs and federal guidelines for tenant protections to prevent displacement and ensure housing security.

- Targeted Support for Vulnerable Populations: Specific programs designed to assist veterans, seniors, individuals with disabilities, and low-income families in securing stable housing.

Regulatory Reforms and Market Oversight

Effective housing market stabilization also necessitates robust regulatory frameworks and vigilant market oversight. The 2026 interventions are expected to include:

- Combating Speculation: Exploring measures to curb excessive speculative buying that drives up prices without adding real value to communities. This could involve increased taxes on properties flipped within short periods or stricter lending standards for non-owner-occupied purchases.

- Transparent Data Collection and Reporting: Enhancing federal data collection on housing market trends, including sales prices, rental rates, inventory levels, and demographic shifts, to provide policymakers and the public with more accurate and timely information. This transparency is vital for effective housing market stabilization.

- Consumer Protection Measures: Strengthening protections for homebuyers and renters against predatory lending practices, unfair eviction procedures, and discriminatory housing practices.

- Review of GSEs (Government-Sponsored Enterprises): A re-evaluation of the roles of Fannie Mae and Freddie Mac to ensure they are effectively supporting affordable housing and housing market stabilization, rather than inadvertently contributing to market volatility.

The Role of Technology and Data in Housing Market Stabilization

The 2026 federal plan is expected to leverage cutting-edge technology and data analytics to achieve its goals. Predictive modeling can help identify potential market imbalances before they escalate, allowing for proactive interventions. Artificial intelligence could be used to optimize resource allocation for housing development and identify areas most in need of support. Furthermore, blockchain technology could enhance the transparency and security of property transactions, reducing fraud and streamlining processes. The integration of these technological advancements will be crucial for the precision and efficacy of federal efforts towards housing market stabilization.

Moreover, robust data sharing between federal, state, and local entities will create a more comprehensive picture of the housing landscape. This integrated data approach will enable policymakers to make evidence-based decisions, tailor programs to specific regional needs, and monitor the effectiveness of interventions in real-time. Such a data-driven strategy is essential for achieving the targeted 15% reduction in price volatility and ensuring sustained housing market stabilization.

Anticipated Challenges and Potential Roadblocks

While the goal of housing market stabilization is laudable, the path to achieving it is fraught with challenges. The political landscape, economic shifts, and unforeseen global events can all impact the effectiveness of these interventions. Opposition from various interest groups, including developers, real estate investors, and even some homeowners who benefit from rising property values, is almost inevitable. Crafting policies that balance these competing interests while remaining true to the objective of broad housing market stability will require significant political will and skillful negotiation.

Economic headwinds, such as persistent inflation, rising interest rates beyond federal control, or a global recession, could also complicate efforts. Furthermore, the sheer scale and diversity of the U.S. housing market mean that a one-size-fits-all approach is unlikely to succeed. Policies must be flexible enough to address the unique challenges of urban, suburban, and rural areas, as well as different regional economies. The success of housing market stabilization will depend heavily on the ability of federal agencies to adapt and respond to these dynamic conditions.

Another significant challenge lies in the implementation and enforcement of new regulations. Ensuring compliance across thousands of municipalities and countless private entities will require substantial resources and a robust oversight mechanism. Public acceptance and cooperation will also be critical; educating the public about the long-term benefits of housing market stabilization and addressing concerns about potential short-term disruptions will be paramount.

Measuring Success: Beyond the 15% Volatility Target

While a 15% reduction in national price volatility is a clear and measurable target for housing market stabilization, true success will encompass a broader range of indicators. These include:

- Improved Affordability Ratios: A significant decrease in the percentage of income households spend on housing, both for renters and homeowners.

- Increased Homeownership Rates: Particularly among historically underserved communities and first-time buyers.

- Reduced Homelessness: A decline in the number of individuals and families experiencing homelessness, indicating greater access to stable housing.

- Sustainable Construction Growth: A steady, healthy pace of new housing construction that meets demand without oversupplying the market.

- Reduced Regional Disparities: A narrowing of the gap in housing affordability and availability between different regions and cities.

- Enhanced Housing Quality: Improvements in the overall quality and safety of the housing stock across the nation.

These holistic measures will provide a more comprehensive picture of the interventions’ impact and confirm whether genuine housing market stabilization has been achieved, leading to a more equitable and prosperous society.

The Economic and Social Benefits of a Stable Housing Market

Achieving housing market stabilization has far-reaching positive consequences for the entire economy and society. Economically, a stable housing market reduces the risk of financial crises, fosters consumer confidence, and supports sustainable economic growth. When housing costs are predictable and reasonable, households have more disposable income, which can be channeled into other sectors of the economy, stimulating demand and job creation. Businesses also benefit from a stable workforce that can afford to live near their workplaces.

Socially, housing market stabilization promotes greater equity and opportunity. When housing is affordable, individuals and families can invest in education, healthcare, and their communities. It reduces stress, improves mental and physical health outcomes, and strengthens social cohesion. Stable housing is a foundational element for well-being, allowing individuals to build wealth, achieve financial security, and participate more fully in civic life. It also helps to prevent the displacement of communities, preserving local culture and social networks. The federal interventions in 2026 are not just about numbers and percentages; they are about investing in the long-term health and prosperity of the American populace.

Case Studies and Historical Precedents

While the 2026 federal interventions are unique in their scope and specific targets, governments have historically played various roles in housing markets, both domestically and internationally. Examining these precedents can offer valuable insights. For instance, post-World War II, the U.S. government implemented policies that significantly boosted homeownership rates, though some of these policies also inadvertently contributed to segregation. In recent decades, countries like Germany have maintained relatively stable housing markets through strong rental protections, robust social housing programs, and less emphasis on housing as a speculative investment.

Conversely, the 2008 financial crisis serves as a stark reminder of the dangers of an unregulated and overheated housing market. The lessons learned from that period – particularly concerning predatory lending and the lack of oversight – are undoubtedly informing the 2026 strategies. The federal government’s approach appears to be a blend of supply-side incentives, demand-side assistance, and regulatory safeguards, drawing on both successful and cautionary tales from history to ensure effective housing market stabilization.

The Role of Local and State Governments

Federal interventions, while powerful, cannot succeed in isolation. The success of housing market stabilization in 2026 will heavily depend on the active participation and cooperation of state and local governments. Many of the critical levers for housing policy, such as zoning regulations, building codes, and property taxes, reside at the local level. The federal plan will likely include incentives, grants, and technical assistance to encourage states and municipalities to align their policies with national goals. This collaborative approach is essential for tailoring solutions to regional specificities and ensuring that federal directives translate into tangible improvements on the ground. State and local governments can also play a crucial role in identifying specific community needs, managing local development projects, and implementing direct assistance programs that complement federal initiatives. This multi-tiered governance model is vital for comprehensive housing market stabilization.

Future Outlook: A More Equitable Housing Landscape

If the federal interventions in 2026 prove successful, the American housing landscape could look significantly different by the end of the decade. We could see a market characterized by more predictable price growth, increased affordability, and greater access to homeownership for a broader segment of the population. The reduction in price volatility would not only benefit homebuyers but also create a more stable environment for long-term investments in housing infrastructure and community development. The aim is to move away from housing as a speculative commodity and back towards its fundamental role as a secure and stable asset for families.

Moreover, a stable housing market is intrinsically linked to broader economic resilience. By reducing the risk of housing bubbles and busts, the federal government aims to insulate the economy from one of its most significant vulnerabilities. This long-term vision for housing market stabilization extends beyond mere economic metrics; it envisions a society where housing security is a reality for all, fostering stronger communities, reducing inequality, and reinforcing the American dream for future generations.

Conclusion: A New Era for Housing Market Stabilization

The federal government’s planned interventions in 2026 mark a pivotal moment for the U.S. housing market. With an ambitious target of a 15% reduction in national price volatility, these comprehensive strategies aim to address the root causes of instability, from supply shortages to affordability crises. By focusing on boosting construction, enhancing buyer assistance, and implementing robust regulatory reforms, the government seeks to usher in an era of genuine housing market stabilization. While challenges undoubtedly lie ahead, the potential rewards – a more equitable, affordable, and resilient housing market – are profound. The success of these initiatives will not only redefine the landscape of homeownership but also contribute significantly to the overall economic health and social well-being of the nation. The journey towards housing market stabilization is complex, but with concerted effort and strategic foresight, the vision of a stable and accessible housing future for all Americans may well become a reality.