Maximizing Your HSA: An Expert Guide to 2026 Contribution Limits and Tax Benefits

In the evolving landscape of personal finance and healthcare, the Health Savings Account (HSA) stands out as an exceptionally powerful tool for both managing medical expenses and building long-term wealth. As we look ahead to 2026, understanding the projected HSA contribution limits and the myriad tax benefits associated with these accounts becomes paramount for anyone serious about optimizing their financial health. This comprehensive guide will delve deep into the intricacies of HSA 2026 benefits, offering expert strategies to help you maximize this invaluable resource.

The HSA is not just another savings account; it’s a unique, triple-tax-advantaged investment vehicle that offers unparalleled opportunities for financial growth. For those enrolled in a high-deductible health plan (HDHP), an HSA can be a game-changer, providing a tax-efficient way to save for current and future medical costs, including those in retirement. The beauty of the HSA lies in its flexibility and its ability to serve as both a short-term spending account for healthcare and a long-term investment vehicle.

Anúncios

Understanding the HSA Landscape in 2026

While the official HSA contribution limits for 2026 are typically announced by the IRS in the latter half of the preceding year (around October or November 2025), we can make informed projections based on historical trends and inflation adjustments. These limits are crucial because they dictate how much you can contribute to your account annually and, consequently, how much you can save in taxes and grow your investments.

Anúncios

Historically, HSA contribution limits have seen modest increases year over year, primarily driven by inflation. These adjustments are designed to keep pace with rising healthcare costs and maintain the purchasing power of your savings. For 2026, we anticipate a continuation of this trend, meaning individuals and families will likely see a slight bump in the maximum allowable contributions.

It’s important to note that eligibility for an HSA is tied directly to enrollment in an HDHP. For 2026, the IRS will also define the minimum deductible and maximum out-of-pocket expenses for HDHPs. These thresholds are critical for determining whether your health plan qualifies you to open and contribute to an HSA. Staying informed about these evolving figures is the first step in leveraging your HSA 2026 benefits effectively.

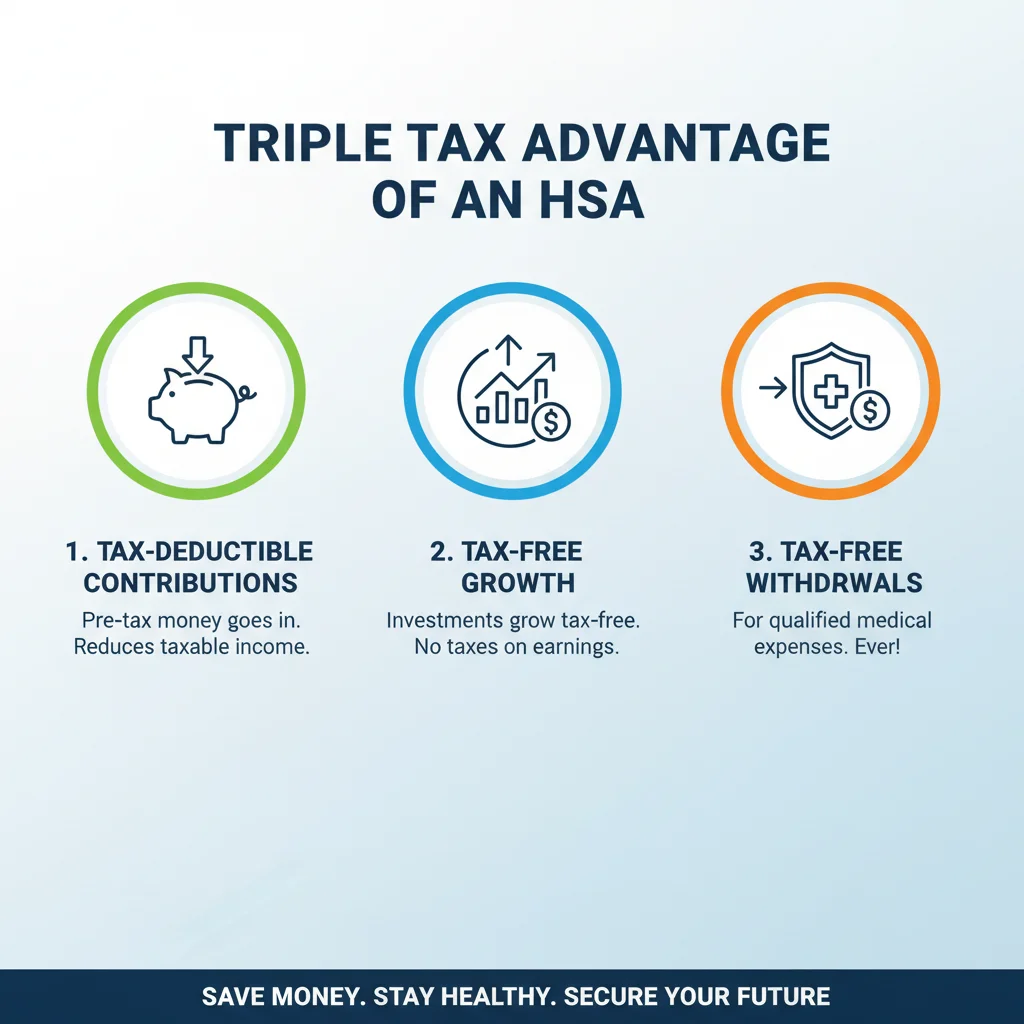

Beyond the contribution limits, understanding the broader HSA landscape involves recognizing its unique position in the pantheon of retirement and savings vehicles. Unlike a 401(k) or IRA, an HSA offers tax advantages at all three stages: contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals are tax-free. This ‘triple-tax advantage’ is a powerful engine for wealth accumulation, making it a critical component of any savvy financial plan.

Projected 2026 HSA Contribution Limits and Eligibility

While definitive numbers for 2026 are yet to be released, we can look at the 2025 limits and historical growth rates to provide educated estimates. For 2025, the limits were set at $4,150 for self-only coverage and $8,300 for family coverage, with an additional catch-up contribution of $1,000 for those aged 55 and over. Given typical inflation adjustments, we might see these figures increase by approximately 2-3% for 2026. This would place individual contributions in the range of $4,230 to $4,275 and family contributions between $8,460 and $8,550. The catch-up contribution for those 55 and older is statutory and usually remains constant at $1,000.

It’s crucial to confirm these figures once they are officially announced by the IRS. However, planning based on these projections allows you to begin strategizing your contributions well in advance. Maximizing your HSA 2026 benefits starts with knowing how much you can contribute.

Eligibility for an HSA remains contingent upon enrollment in an HDHP. For 2025, an HDHP was defined as a plan with a minimum deductible of $1,650 for self-only coverage and $3,300 for family coverage, and maximum out-of-pocket expenses of $8,300 for self-only and $16,600 for family coverage. These thresholds are also subject to inflation adjustments each year. Therefore, for 2026, expect slightly higher minimum deductibles and maximum out-of-pocket limits. Always verify your health plan meets these criteria to ensure your eligibility for an HSA.

Beyond the basic requirements, there are a few other nuances to HSA eligibility. You cannot be enrolled in Medicare, nor can you be claimed as a dependent on someone else’s tax return. If you have other health coverage that is not an HDHP (e.g., a spouse’s plan that covers you and is not a limited-purpose FSA or HRA), you may not be eligible. Understanding these rules is fundamental to ensuring you can legally contribute and reap the rewards of your HSA 2026 benefits.

Why Maximize Your Contributions?

The primary reason to maximize your HSA contributions each year is to take full advantage of its unparalleled tax benefits. Every dollar you contribute is a dollar that reduces your taxable income, potentially lowering your tax bill. Furthermore, these contributions grow tax-free, and when withdrawn for qualified medical expenses, they are also tax-free. This triple-tax advantage is a financial superpower that few other accounts offer.

By consistently contributing the maximum allowed, you accelerate the growth of your healthcare savings. Over time, the compounding effect of tax-free growth can lead to a substantial balance, providing a robust safety net for future medical needs, especially in retirement when healthcare costs tend to escalate significantly. Think of your HSA as a personal health endowment, growing steadily to cover the inevitable expenses of aging.

The Triple Tax Advantage of HSAs: A Deep Dive into HSA 2026 Benefits

The appeal of an HSA largely stems from its unique triple-tax advantage, making it one of the most tax-efficient savings vehicles available. Let’s break down each component:

- Tax-Deductible Contributions: When you contribute to an HSA, those contributions are 100% tax-deductible from your gross income. This means that every dollar you put into your HSA reduces your taxable income for the year, potentially lowering your overall tax liability. This deduction is an ‘above-the-line’ deduction, meaning you can claim it even if you don’t itemize deductions on your tax return. For employers who contribute to employee HSAs, these contributions are also tax-free for the employee and tax-deductible for the employer, creating a win-win scenario.

- Tax-Free Growth: Once your contributions are in your HSA, they can be invested. Any interest, dividends, or capital gains earned on these investments grow tax-free. This is where the magic of compounding truly shines. Over decades, your investments can grow substantially without being eroded by annual taxes, significantly increasing your long-term savings potential. This tax-free growth is a critical differentiator from taxable brokerage accounts.

- Tax-Free Withdrawals for Qualified Medical Expenses: Perhaps the most compelling benefit is that withdrawals from your HSA are entirely tax-free, provided they are used for qualified medical expenses. This includes a wide range of expenses, from doctor visits and prescription medications to dental work, vision care, and even certain over-the-counter medications. The ability to pay for these costs with tax-free dollars is incredibly powerful, effectively giving you a discount on your healthcare expenditures.

Beyond these three pillars, an HSA offers additional flexibility. Unlike a Flexible Spending Account (FSA), HSA funds roll over year after year, never expiring. This means you don’t have to worry about a ‘use-it-or-lose-it’ policy, allowing you to accumulate a significant balance over time. Furthermore, once you reach age 65 (or become disabled), you can withdraw funds from your HSA for any purpose without penalty, just like a traditional IRA. While these withdrawals would be subject to ordinary income tax if not used for qualified medical expenses, the flexibility is a huge advantage, effectively transforming your HSA into an additional retirement account.

Strategic Uses of Your HSA 2026 Benefits

Leveraging your HSA 2026 benefits goes beyond merely contributing. It involves strategic planning to maximize its utility for both immediate healthcare needs and long-term financial goals.

1. Pay Out-of-Pocket, Invest the Rest

One of the most effective strategies for maximizing your HSA is to pay for current qualified medical expenses out-of-pocket, if you have the means, and allow your HSA funds to grow untouched. Keep meticulous records of all your medical expenses that you pay for with non-HSA funds. You can then reimburse yourself for these expenses tax-free at any point in the future – even decades later. This strategy allows your HSA investments to compound for a longer period, significantly increasing the overall tax-free growth.

Imagine paying a $500 doctor’s bill today from your checking account. You keep the receipt. If you leave that $500 in your HSA, invested for 20 years, it could grow to several thousand dollars. When you need funds in retirement, you can then withdraw that original $500 (plus potentially thousands more in growth) tax-free by reimbursing yourself for that 20-year-old expense. This makes your HSA a powerful, flexible, and tax-efficient emergency fund for healthcare.

2. Invest for Retirement Healthcare Costs

Healthcare is one of the largest expenses in retirement. An HSA is arguably the best vehicle for saving for these costs. By treating your HSA primarily as an investment account, you can build a substantial nest egg specifically earmarked for medical expenses in your golden years. This includes Medicare premiums, deductibles, co-pays, and other out-of-pocket expenses not covered by Medicare. The tax-free growth and withdrawals make it far superior to a 401(k) or IRA for this specific purpose.

Many financial advisors recommend prioritizing maxing out your HSA after receiving any employer match in your 401(k) or 403(b), due to its superior tax advantages for healthcare savings. This strategy ensures you’re addressing a crucial and often underestimated aspect of retirement planning.

3. Use the Catch-Up Contribution

For those aged 55 and older, the additional $1,000 catch-up contribution is a significant advantage. This allows individuals nearing retirement to accelerate their HSA savings, providing an even larger buffer against future medical costs. If both spouses are 55 or older and have separate HSAs, each can contribute the catch-up amount, effectively adding an extra $2,000 to their combined annual contributions.

This catch-up provision recognizes that healthcare needs often increase with age and provides a valuable opportunity to boost your HSA balance precisely when you might need it most. Don’t overlook this crucial aspect of HSA 2026 benefits if you qualify.

4. Understand Qualified Medical Expenses

While the list of qualified medical expenses is extensive, it’s vital to understand what it covers to avoid non-qualified withdrawals, which would be subject to income tax and a 20% penalty if you’re under 65. The IRS Publication 502 provides a comprehensive list, but generally, it includes most medical care, dental work, vision care, prescription drugs, and even some over-the-counter medications with a doctor’s prescription. Premiums for long-term care insurance, Medicare parts A, B, D, and Medicare Advantage plans are also considered qualified medical expenses, but not regular health insurance premiums.

Keeping thorough records of all your qualified medical expenses, whether reimbursed immediately or saved for future reimbursement, is paramount. This ensures you can always justify your tax-free withdrawals.

HSA vs. Other Retirement Accounts: Why HSA 2026 Benefits Stand Out

While 401(k)s and IRAs are foundational to retirement planning, the HSA offers unique advantages, particularly when it comes to healthcare costs. Comparing them highlights why the HSA, especially with its 2026 benefits, deserves a prominent place in your financial strategy.

- Tax Treatment: Traditional 401(k)s and IRAs offer tax-deductible contributions and tax-deferred growth, with withdrawals taxed in retirement. Roth accounts have after-tax contributions, tax-free growth, and tax-free withdrawals in retirement. The HSA, as discussed, boasts a triple-tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This makes it superior for healthcare savings.

- Flexibility: While 401(k)s and IRAs typically impose penalties for withdrawals before age 59½ (with some exceptions), HSA funds can be withdrawn tax-free at any time for qualified medical expenses, without penalty. After age 65, HSA funds can be withdrawn for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income, similar to a traditional IRA.

- Employer Contributions: Many employers contribute to employee HSAs, which is essentially free money. This is less common for IRAs and depends on the 401(k) match.

- Rollover: Unlike FSAs, HSA funds never expire and roll over year after year, allowing for significant accumulation.

The HSA truly shines as a hybrid account – a healthcare savings vehicle that doubles as a powerful retirement investment tool. For those who anticipate significant healthcare costs in retirement (which is most people), maximizing your HSA 2026 benefits can be more impactful than adding an equivalent amount to a traditional retirement account.

Choosing the Right HSA Provider and Investment Options

Not all HSA providers are created equal. The choice of provider can significantly impact your ability to maximize your HSA 2026 benefits. When selecting an HSA administrator, consider the following:

- Fees: Look for providers with low or no monthly maintenance fees, investment fees, and transaction fees. High fees can eat into your returns over time.

- Investment Options: A good HSA provider will offer a diverse range of investment options, including low-cost index funds, ETFs, and mutual funds. Access to robust investment choices is crucial if you plan to use your HSA as a long-term investment vehicle.

- Minimums: Some providers have minimum balance requirements before you can invest your funds. Ideally, you want a provider that allows you to invest your money as soon as possible.

- User Experience: A user-friendly online portal and mobile app can make managing your HSA much easier, from tracking contributions to submitting reimbursement requests.

- Customer Service: Responsive and knowledgeable customer service is important, especially if you have questions about qualified expenses or investment options.

Many employers offer a default HSA provider, but you are not always obligated to use it for all your funds. You might be able to contribute through payroll to your employer’s provider to get any employer contributions, and then transfer funds to a different, more investment-friendly HSA provider that you choose. This strategy allows you to benefit from employer contributions while still optimizing your investment growth. Researching and comparing different HSA providers is a vital step in harnessing your HSA 2026 benefits to their fullest potential.

Common Misconceptions About HSAs

Despite their advantages, HSAs are often misunderstood. Dispelling these myths can help you better utilize your HSA 2026 benefits.

- Myth 1: HSAs are only for current medical expenses. As discussed, HSAs are powerful long-term investment vehicles. Many people use them to save for retirement healthcare costs, viewing them as a supplemental retirement account.

- Myth 2: You lose the money if you don’t use it. This is true for Flexible Spending Accounts (FSAs), but HSAs are different. Funds roll over year after year, accumulating indefinitely.

- Myth 3: HSAs are too complicated. While there are rules, the core concept is simple: save money, get tax deductions, invest tax-free, and withdraw tax-free for medical needs. Most providers make management straightforward.

- Myth 4: You can only use HSA funds for basic medical care. The list of qualified medical expenses is extensive, covering everything from acupuncture to wheelchairs, and even certain long-term care services and insurance premiums.

- Myth 5: I don’t need an HSA because my health is good. Even if you are currently healthy, medical emergencies can happen, and healthcare costs in retirement are almost inevitable. An HSA provides a crucial financial safety net and a powerful investment tool regardless of your current health status.

Integrating HSA 2026 Benefits into Your Overall Financial Plan

The HSA should not be viewed in isolation but as an integral part of your holistic financial plan. Here’s how it fits in:

- Emergency Fund: While not its primary purpose, the flexibility of HSA withdrawals for medical expenses means it can serve as a secondary emergency fund specifically for health-related crises.

- Retirement Planning: As highlighted, the HSA is an excellent vehicle for saving for healthcare costs in retirement, complementing your 401(k) and IRA.

- Tax Planning: The immediate tax deduction for contributions and the tax-free growth and withdrawals make it a powerful tool for reducing your overall tax burden.

- Estate Planning: Upon your death, if your spouse is the beneficiary, the HSA can be treated as their own HSA. If a non-spouse is the beneficiary, the account ceases to be an HSA and is included in their gross income. This aspect needs to be considered in your broader estate plan.

By consciously integrating your HSA into these different facets of your financial life, you can unlock its full potential. Regular review of your contribution strategy, investment choices, and anticipated medical expenses will ensure you are continually maximizing your HSA 2026 benefits and beyond.

Future Outlook for HSAs

The HSA has enjoyed broad bipartisan support since its inception, and its structure has remained relatively stable, with annual inflation adjustments. While legislative changes are always possible, the core triple-tax advantage and the overall framework of the HSA are expected to remain intact for the foreseeable future. This stability makes the HSA a reliable component of long-term financial planning.

As healthcare costs continue to rise, the importance of tax-advantaged savings vehicles like the HSA will only grow. Staying informed about annual limit adjustments, understanding the rules, and employing smart investment strategies will be key to making the most of your HSA. The HSA 2026 benefits are not just about a single year’s contributions; they are about building a foundation for decades of financial security and health management.

Conclusion: Harnessing Your HSA 2026 Benefits for a Healthier Financial Future

The Health Savings Account is a truly exceptional financial tool, offering a unique blend of tax advantages and flexibility for managing healthcare costs now and in the future. As we approach 2026, understanding the projected contribution limits, the nuances of eligibility, and the profound triple-tax benefits is crucial for anyone looking to optimize their financial well-being.

By adopting strategic approaches such as maximizing contributions, investing for long-term growth, and leveraging catch-up provisions, you can transform your HSA from a mere savings account into a powerful wealth-building engine. Remember to choose a suitable HSA provider with low fees and robust investment options, and integrate your HSA strategy seamlessly into your broader financial and retirement plans.

Don’t underestimate the power of your HSA. It’s more than just a way to pay for doctor’s visits; it’s a critical component of a resilient financial future, offering a tax-efficient path to cover medical expenses in retirement and beyond. Start planning now to fully harness your HSA 2026 benefits and secure your financial health for years to come.

Contributions: A Comprehensive Retirement Planning Guide")