Maximize Retirement Savings 2026: IRA Limits & Strategies

In an ever-evolving financial landscape, the quest to maximize retirement savings remains a top priority for individuals and families across the globe. As we look ahead to 2026, understanding the nuances of retirement accounts, particularly Individual Retirement Arrangements (IRAs), and their updated contribution limits, becomes paramount. This comprehensive guide is designed to equip you with the knowledge and strategies necessary to not only meet but exceed your retirement goals, ensuring a secure and prosperous future.

Retirement planning is not merely about setting aside money; it’s about strategic allocation, understanding tax implications, and leveraging every available tool to your advantage. The year 2026 promises new opportunities and adjustments that, when understood and acted upon, can significantly impact your financial well-being in retirement. Our focus will be on the critical updates to IRA contribution limits, how they compare to previous years, and actionable steps you can take to make the most of these changes.

Whether you’re just starting your career, in your peak earning years, or nearing retirement, the principles outlined here will provide a roadmap to optimize your savings. We’ll delve into the specifics of Traditional and Roth IRAs, explore the benefits of employer-sponsored plans like 401(k)s, and discuss advanced strategies such as catch-up contributions and the backdoor Roth IRA. The goal is to empower you with the insights needed to make informed decisions and ultimately, to maximize retirement savings effectively.

Understanding the Importance of Early Retirement Planning

The power of compound interest is perhaps the most compelling argument for starting your retirement planning early. Even small, consistent contributions made over a long period can grow into a substantial sum, thanks to the magic of compounding. For instance, a 25-year-old who starts saving today will see their money grow significantly more than someone who begins saving at 35, even if the latter contributes more annually. This exponential growth underscores why understanding how to maximize retirement savings from an early age is so crucial.

Beyond compound interest, early planning allows for greater flexibility and resilience against market fluctuations. When you have a longer time horizon, you can afford to take on a bit more risk, which often translates to higher potential returns. Moreover, economic downturns become less daunting as there’s ample time for your investments to recover before you need to draw on them. This long-term perspective is a cornerstone of successful retirement planning and a key factor in achieving your financial independence.

The Landscape of Retirement Accounts

Before diving into the 2026 specifics, it’s essential to have a foundational understanding of the primary retirement vehicles available. These include:

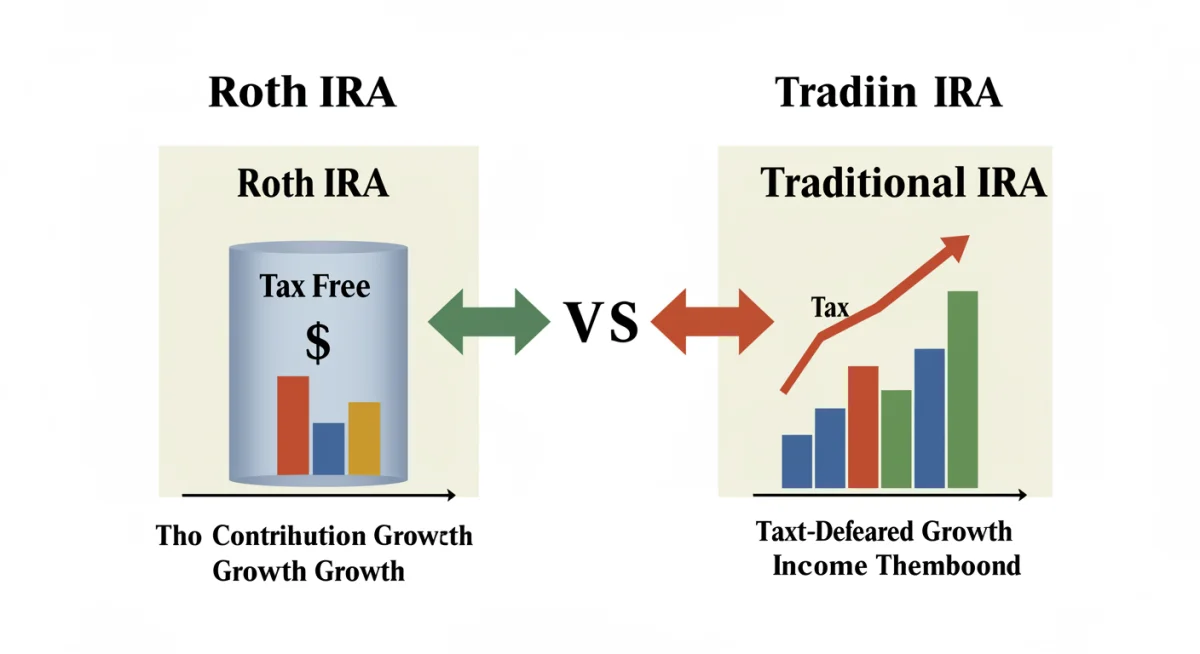

- Traditional IRAs: Contributions may be tax-deductible, and earnings grow tax-deferred until withdrawal in retirement. Withdrawals in retirement are taxed as ordinary income.

- Roth IRAs: Contributions are made with after-tax dollars, meaning qualified withdrawals in retirement are tax-free. This is particularly attractive for those who expect to be in a higher tax bracket in retirement.

- 401(k)s and Other Employer-Sponsored Plans: These plans, often with employer matching contributions, offer a powerful way to save. Like Traditional IRAs, contributions are typically pre-tax, and growth is tax-deferred.

- SEP IRAs and SIMPLE IRAs: Designed for small business owners and self-employed individuals, these offer higher contribution limits than traditional IRAs.

Each of these accounts comes with its own set of rules, benefits, and limitations, making the choice dependent on your individual financial situation, income level, and retirement goals. The objective is always to choose the accounts that best enable you to maximize retirement savings given your unique circumstances.

2026 IRA Contribution Limits: What’s New?

One of the most anticipated updates for retirement savers each year concerns the IRS contribution limits for IRAs. While the definitive 2026 figures are typically announced later in the preceding year, projections and historical trends provide a strong indication of what to expect. These adjustments are usually tied to inflation and cost-of-living increases, reflecting the government’s effort to help individuals keep pace with rising expenses and adequately save for retirement. Staying informed about these changes is fundamental to effectively maximize retirement savings.

For 2026, it is projected that the standard IRA contribution limit (for both Traditional and Roth IRAs) will see an increase from previous years. This increase, even if modest, presents a valuable opportunity to set aside more tax-advantaged money for your future. For illustrative purposes, if the limit increases by, for example, $500, that’s an additional $500 that can grow tax-deferred or tax-free over decades, significantly impacting your overall retirement nest egg.

Catch-Up Contributions for Those 50 and Over

A particularly important feature for older savers is the provision for catch-up contributions. These allow individuals aged 50 and over to contribute an additional amount beyond the standard limit to their IRAs. This is a critical mechanism designed to help those who may have started saving later or experienced career interruptions to maximize retirement savings in their later working years. The catch-up contribution limit is also subject to annual adjustments based on inflation.

For 2026, we anticipate an increase in the catch-up contribution limit as well. This means individuals aged 50 and above will likely be able to contribute an even larger sum to their IRAs, providing a powerful boost to their retirement funds. It’s a strategic advantage that should not be overlooked by eligible individuals, as it can significantly accelerate the growth of their retirement portfolio.

Keeping track of these specific numbers as they are released by the IRS will be crucial. Our advice is to bookmark official IRS publications or reliable financial news sources to get the most up-to-date information as soon as it becomes available. Proactive awareness allows for proactive planning, which is key to optimizing your retirement contributions.

Strategies to Maximize Retirement Savings with New IRA Limits

With the anticipated adjustments to IRA contribution limits in 2026, now is the opportune time to refine your strategies to maximize retirement savings. This section will explore practical approaches to leverage these new limits, ensuring every dollar you contribute works harder for your future.

1. Max Out Your Contributions

The most straightforward strategy is to contribute the maximum amount allowed to your IRA each year. If you can afford to, contributing the full limit (plus catch-up contributions if eligible) should be your primary goal. This ensures you take full advantage of the tax benefits and the power of compound interest. Many people fall short of this goal, leaving potential tax savings and investment growth on the table. Make it a priority to review your budget and financial capacity to hit these maximums.

2. Automate Your Savings

One of the simplest yet most effective ways to ensure consistent contributions is to automate them. Set up automatic transfers from your checking account to your IRA on a weekly, bi-weekly, or monthly basis. This ‘set it and forget it’ approach helps you stay disciplined and ensures you’re consistently contributing towards the annual limit without having to actively remember each time. Automation removes the psychological barrier of making a conscious decision to save, making it easier to maximize retirement savings.

3. Understand the Traditional vs. Roth IRA Decision

The choice between a Traditional and Roth IRA is critical and depends on your current and projected future tax situation. If you expect to be in a higher tax bracket now than in retirement, a Traditional IRA (with its potential for current tax deductions) might be more advantageous. Conversely, if you anticipate being in a higher tax bracket during retirement, a Roth IRA (with its tax-free withdrawals in retirement) could be the better option. Many financial advisors suggest diversifying by contributing to both if eligible, offering flexibility in retirement. Reviewing your income and tax situation annually is essential to making the best choice.

4. Leverage the Backdoor Roth IRA (If Applicable)

For high-income earners who exceed the income limitations for direct Roth IRA contributions, the backdoor Roth IRA strategy remains a powerful tool to still benefit from tax-free growth. This involves contributing non-deductible funds to a Traditional IRA and then converting them to a Roth IRA. While the conversion itself is a taxable event if you have pre-tax IRA money, if your Traditional IRA consists solely of non-deductible contributions, the conversion is typically tax-free. This strategy requires careful planning and understanding of the pro-rata rule if you have other pre-tax IRA accounts. Consulting a tax professional is highly recommended to ensure compliance and effectiveness when using this method to maximize retirement savings.

5. Don’t Forget Employer-Sponsored Plans

While this article focuses on IRAs, it’s crucial to remember that employer-sponsored plans like 401(k)s, 403(b)s, and 457(b)s offer even higher contribution limits and often come with employer matching contributions, which is essentially free money. Always contribute at least enough to get the full employer match before maximizing your IRA. Once you’ve secured the match, consider maximizing your IRA, and then return to contributing more to your employer plan if you have additional savings capacity. This multi-pronged approach is key to comprehensively maximize retirement savings.

6. Rebalance Your Portfolio Regularly

Beyond contributions, the performance of your investments within your IRA is equally important. Regularly rebalancing your portfolio to align with your risk tolerance and time horizon can significantly impact long-term growth. As you get closer to retirement, you might shift towards a more conservative asset allocation to protect your capital. Conversely, in your younger years, a more aggressive approach might be warranted. A well-managed portfolio strategy complements consistent contributions in the journey to maximize retirement savings.

Advanced Strategies for Boosting Your Retirement Nest Egg

Beyond the fundamental strategies, there are several advanced techniques that can help you further maximize retirement savings, especially as you progress through different life stages and financial situations.

Spousal IRAs: Doubling the Power

If you are married and one spouse earns little or no income, a Spousal IRA allows the working spouse to contribute to an IRA on behalf of the non-working or lower-earning spouse. This effectively doubles the amount a couple can contribute to tax-advantaged retirement accounts each year, assuming both spouses are eligible. It’s a powerful tool for couples looking to build a robust retirement fund together and a great way to maximize retirement savings as a unit.

Health Savings Accounts (HSAs) as a Retirement Vehicle

While primarily designed for healthcare expenses, Health Savings Accounts (HSAs) are often referred to as the ‘triple-tax-advantaged’ account and can serve as an excellent supplementary retirement savings vehicle. Contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals for medical expenses are also tax-free. If you remain healthy into retirement, you can use HSA funds for non-medical expenses, though these withdrawals will be taxed as ordinary income, similar to a Traditional IRA. This flexibility makes HSAs a compelling option for those with high-deductible health plans who want to maximize retirement savings.

Consider a Mega Backdoor Roth (If Employer Plan Allows)

For those with access to a 401(k) plan that allows after-tax contributions and in-service distributions or rollovers, the ‘mega backdoor Roth’ strategy can be incredibly powerful. This involves contributing after-tax money to your 401(k) beyond the pre-tax and Roth 401(k) limits, and then converting that after-tax money into a Roth IRA or Roth 401(k). This allows for a much larger amount of money to grow tax-free than the standard Roth IRA limits permit. This is a more complex strategy and requires careful consideration of your employer plan’s rules and professional guidance to ensure it’s executed correctly to maximize retirement savings significantly.

Delaying Social Security Benefits

While not directly related to IRA contributions, delaying when you claim Social Security benefits can significantly increase your monthly payout. For every year you delay claiming benefits past your full retirement age (up to age 70), your benefit amount increases. This strategy can reduce the amount you need to withdraw from your investment accounts in early retirement, allowing those funds to continue growing and further contributing to your ability to maximize retirement savings by extending their longevity.

Navigating Income Limitations and Phase-Outs

While the prospect of increasing IRA contribution limits in 2026 is exciting, it’s equally important to understand the income limitations and phase-out rules that can affect your ability to contribute to certain IRAs or deduct Traditional IRA contributions. These thresholds are also typically adjusted annually for inflation, and staying informed is key to making optimal decisions to maximize retirement savings.

Roth IRA Income Limitations

Roth IRAs are highly attractive due to their tax-free withdrawals in retirement. However, the ability to contribute directly to a Roth IRA is subject to Modified Adjusted Gross Income (MAGI) limits. If your MAGI exceeds a certain threshold, your ability to contribute directly to a Roth IRA is phased out, and eventually eliminated. For those above these limits, the backdoor Roth IRA strategy, as discussed earlier, becomes a viable alternative to still benefit from tax-free growth.

Traditional IRA Deductibility Phase-Outs

For Traditional IRAs, the deductibility of your contributions depends on whether you (or your spouse) are covered by a retirement plan at work and your MAGI. If you are not covered by a workplace retirement plan, your Traditional IRA contributions are generally fully deductible, regardless of your income. However, if you are covered by a workplace plan, the deductibility of your Traditional IRA contributions begins to phase out once your MAGI reaches certain levels. If your income is too high, your contributions may not be deductible at all. This distinction is crucial for determining the immediate tax benefits of your contributions and is vital for anyone looking to maximize retirement savings through tax efficiency.

It’s imperative to consult the official IRS guidelines for 2026 once they are released to determine the exact income thresholds. These figures will dictate your eligibility for direct contributions and deductions, influencing your overall strategy to maximize retirement savings. Financial planning software or a qualified financial advisor can help you navigate these complex rules and ensure you are making the most tax-efficient choices for your situation.

The Role of Investment Choices in Your IRA

Contributing to an IRA is just the first step; what you invest in within that IRA is equally, if not more, important for long-term growth. The investment choices you make will significantly influence your ability to maximize retirement savings. Your investment strategy should align with your risk tolerance, time horizon, and overall financial goals.

Diversification is Key

A well-diversified portfolio is crucial for mitigating risk and optimizing returns. This means spreading your investments across different asset classes (e.g., stocks, bonds, real estate), industries, and geographies. Diversification helps protect your portfolio from significant losses if one particular asset class or sector underperforms. Within an IRA, you have a wide array of investment options, including mutual funds, exchange-traded funds (ETFs), individual stocks, and bonds. Choosing a mix that suits your profile is essential.

Consider Low-Cost Index Funds and ETFs

For many investors, low-cost index funds and ETFs are an excellent choice within an IRA. These funds offer broad market exposure, diversification, and typically have very low expense ratios compared to actively managed funds. Over the long term, these lower fees can translate into significantly higher returns, helping you to maximize retirement savings by keeping more of your investment gains.

Review and Adjust Annually

Your investment strategy shouldn’t be static. As you age, your risk tolerance may decrease, and your financial goals might shift. It’s wise to review your IRA investments annually, or at least every few years, to ensure they still align with your objectives. This might involve rebalancing your portfolio, adjusting your asset allocation, or exploring new investment opportunities. Regular review ensures your investments are always working optimally towards your goal to maximize retirement savings.

Avoid Emotional Investing

Market volatility can be unsettling, leading some investors to make impulsive decisions based on fear or greed. However, successful long-term investing often requires a disciplined approach, sticking to your investment plan even during turbulent times. Emotional reactions can lead to buying high and selling low, severely hindering your ability to maximize retirement savings. A well-thought-out investment strategy, coupled with automation and a long-term perspective, can help you avoid these pitfalls.

Putting it All Together: A Holistic Approach to 2026 Retirement Planning

Successfully navigating the 2026 retirement landscape and truly optimizing your savings requires a holistic approach that integrates all the strategies discussed. It’s not just about one action but a combination of consistent effort, informed decisions, and adaptability.

Create a Detailed Financial Plan

Start by developing a comprehensive financial plan that outlines your current financial situation, your retirement goals, and the steps you’ll take to achieve them. This plan should include your desired retirement age, estimated retirement expenses, and projected income sources. A clear plan acts as your roadmap, guiding your decisions on how to maximize retirement savings.

Regularly Monitor Your Progress

Don’t just set your plan and forget it. Regularly monitor your progress towards your retirement goals. Are you on track to hit your contribution limits? Are your investments performing as expected? Are there any unexpected expenses or income changes that require adjustments to your plan? Consistent monitoring allows for timely course corrections, ensuring you remain on the path to a secure retirement.

Seek Professional Guidance

For many, the complexities of retirement planning, especially with evolving tax laws and contribution limits, can be overwhelming. A qualified financial advisor can provide personalized guidance, help you understand the nuances of different retirement vehicles, and develop a tailored strategy to maximize retirement savings. They can also assist with tax planning, estate planning, and other aspects of your financial life that impact your retirement.

Stay Informed About Legislative Changes

Retirement planning is an ongoing process that requires staying informed about legislative changes that could impact your savings. Tax laws, contribution limits, and other regulations can change, and being aware of these shifts allows you to adapt your strategy accordingly. Subscribing to financial news, attending webinars, and consulting with your financial advisor are great ways to stay updated.

In conclusion, the year 2026 presents a fresh opportunity to reassess and supercharge your retirement savings strategy. By understanding the updated IRA contribution limits, strategically choosing between Traditional and Roth options, leveraging catch-up contributions, and exploring advanced techniques, you can significantly enhance your financial security. Remember, the journey to a comfortable retirement is a marathon, not a sprint. Consistent effort, informed decisions, and proactive planning are the cornerstones of success in your quest to maximize retirement savings.