2026 Wealth Preservation: Advanced Strategies to Mitigate Inflation’s 4% Impact

Anúncios

2026 Wealth Preservation: Advanced Strategies to Mitigate Inflation’s 4% Impact

As we cast our gaze towards 2026, the economic horizon presents both opportunities and challenges. A significant concern for investors and individuals alike remains the persistent threat of inflation. While central banks strive for price stability, a 4% inflation rate could significantly erode purchasing power and diminish the real value of your hard-earned assets. Therefore, understanding and implementing robust Wealth Preservation 2026 strategies is not merely advisable, but essential. This comprehensive guide delves into advanced tactics designed to protect and grow your wealth in an environment where inflation threatens to quietly steal your financial future.

Anúncios

The concept of Wealth Preservation 2026 extends beyond simply maintaining your current net worth. It encompasses proactive measures to ensure your assets not only retain their value but also experience real growth after accounting for inflationary pressures. The year 2026, with its unique economic forecasts and global uncertainties, demands a sophisticated approach to financial planning. We will explore a multifaceted strategy, combining traditional wisdom with innovative financial instruments, to build a resilient portfolio capable of weathering economic storms and emerging stronger.

Anúncios

Understanding the 4% Inflation Threat in 2026

Before we can effectively preserve wealth, we must first understand the enemy: inflation. A 4% inflation rate, while seemingly modest, has a compounding effect that can be devastating over time. For instance, an asset worth $100,000 today would require $104,000 next year just to maintain the same purchasing power. Over a decade, this erosion accelerates dramatically. In 2026, various factors could contribute to sustained inflationary pressures, including supply chain disruptions, geopolitical tensions, fiscal policies, and evolving consumer demand. Recognizing these drivers is the first step in formulating an effective Wealth Preservation 2026 plan.

Economic forecasts for 2026 suggest a complex interplay of global forces. While some indicators point towards moderation, others hint at persistent challenges. Labor market dynamics, energy prices, and raw material costs are all variables that could influence the inflation trajectory. For the proactive investor, assuming a 4% inflation rate as a baseline for planning provides a prudent margin of safety. This assumption allows for the development of strategies that are resilient even if inflation exceeds current expectations, solidifying your Wealth Preservation 2026 efforts.

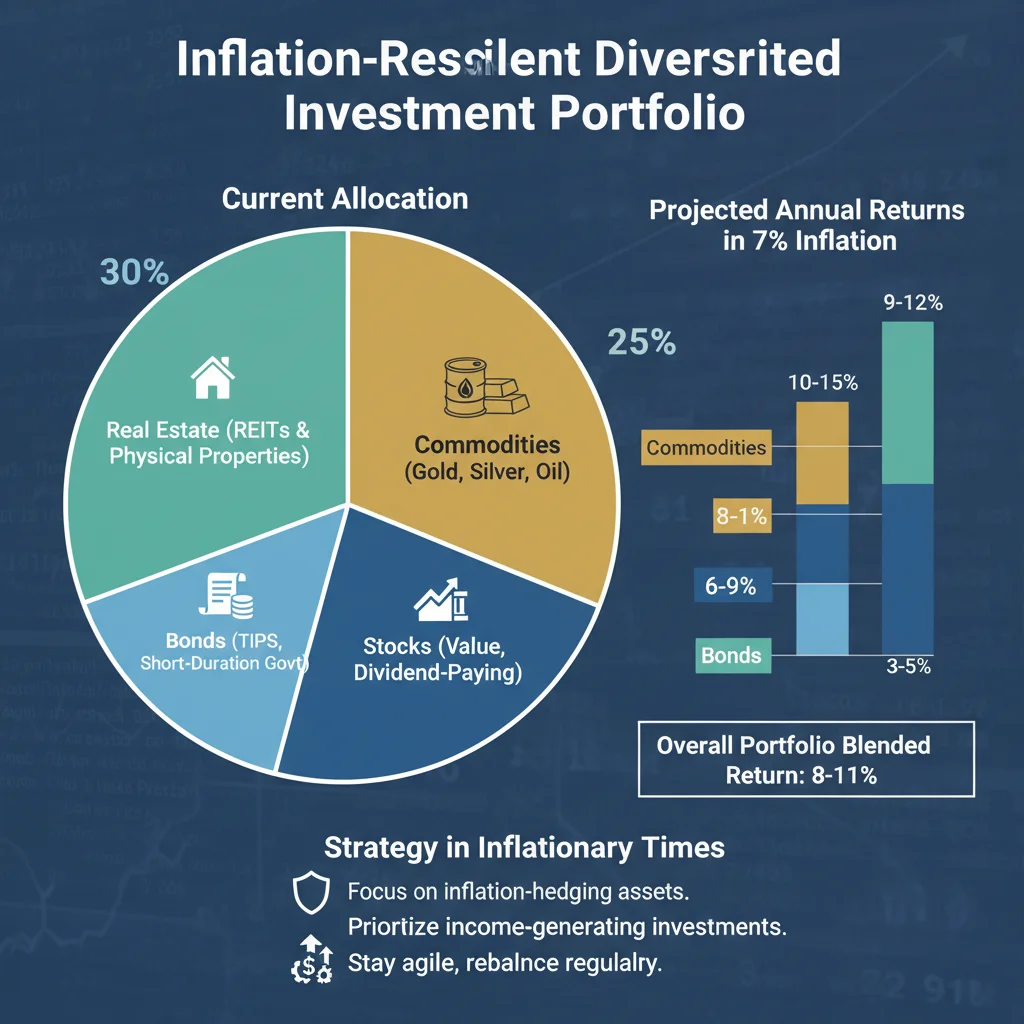

The Cornerstone of Wealth Preservation: Diversification Reimagined

Diversification has always been the bedrock of sound investment, but in an inflationary environment, its application needs to be reimagined. Traditional diversification across stocks and bonds might not be sufficient when both asset classes face headwinds from rising prices and interest rates. For effective Wealth Preservation 2026, diversification must extend to a broader range of asset classes, including those historically known to act as inflation hedges.

Real Assets: Your Shield Against Inflation

Real assets are tangible assets that typically hold or increase their value during inflationary periods. They offer a direct hedge against rising prices because their value is often tied to the cost of production or the demand for physical goods. Key real assets to consider for Wealth Preservation 2026 include:

- Real Estate: Both residential and commercial properties can be excellent inflation hedges. Rental income often increases with inflation, and property values tend to appreciate. Investing in REITs (Real Estate Investment Trusts) can provide diversified exposure without direct property management.

- Commodities: Raw materials like gold, silver, oil, natural gas, and agricultural products tend to perform well when inflation is high. Their prices often rise as the cost of living increases. Gold, in particular, has a long history as a store of value during economic uncertainty and inflationary times.

- Infrastructure: Investments in infrastructure projects (e.g., toll roads, utilities, pipelines) can provide stable, inflation-linked cash flows. These assets are often essential services, making their revenue streams resilient.

- Timberland and Farmland: These are often overlooked but powerful inflation hedges. The value of the land and the products derived from it (timber, crops) tend to increase with inflation, offering both capital appreciation and income.

Incorporating a strategic allocation to these real assets is crucial for any robust Wealth Preservation 2026 strategy. They provide a tangible buffer against the erosion of purchasing power that paper assets might experience.

Beyond Traditional Equities and Fixed Income

While equities and fixed income remain vital components of any portfolio, their role in Wealth Preservation 2026 needs careful consideration. For equities, focus on companies with strong pricing power, low debt, and robust free cash flow. These businesses are better able to pass on rising costs to consumers without sacrificing profitability. Sectors that historically perform well in inflationary environments include:

- Consumer Staples: Companies producing essential goods often maintain demand regardless of economic cycles.

- Healthcare: Demand for healthcare services is generally inelastic.

- Energy: As energy prices rise, so do the revenues of energy companies.

- Utilities: Often regulated, utilities can pass on cost increases, though sometimes with a lag.

For fixed income, traditional long-duration bonds are particularly vulnerable to inflation and rising interest rates. Instead, consider:

- Treasury Inflation-Protected Securities (TIPS): These government bonds adjust their principal value in line with inflation, providing a direct hedge.

- Short-Duration Bonds: Less sensitive to interest rate changes, making them more resilient in a rising rate environment.

- Floating-Rate Notes: The interest payments adjust periodically based on a benchmark rate, offering protection against rising rates.

Re-evaluating your exposure to these asset classes and adjusting allocations based on the 2026 inflation outlook is a critical step in your Wealth Preservation 2026 journey.

Innovative Strategies and Alternative Investments for 2026

The financial landscape of 2026 is rapidly evolving, bringing forth new opportunities for Wealth Preservation 2026 that were less accessible or even non-existent a decade ago. These innovative strategies and alternative investments can provide additional layers of protection and growth potential.

Private Equity and Venture Capital

Investing in private equity and venture capital funds can offer exposure to high-growth companies before they go public. These investments are less correlated with public markets and can provide significant returns, though they come with higher risk and illiquidity. For accredited investors, strategic allocation to these areas can enhance overall portfolio resilience and growth, contributing significantly to Wealth Preservation 2026.

Hedge Funds and Absolute Return Strategies

Certain hedge fund strategies are designed to generate positive returns regardless of market direction, offering an ‘absolute return’ uncorrelated with traditional markets. These funds often employ sophisticated techniques like short-selling, arbitrage, and derivatives. While complex and typically requiring substantial capital, they can be a powerful tool for Wealth Preservation 2026, especially in volatile or inflationary periods.

Digital Assets and Blockchain Technology

The emergence of digital assets, primarily cryptocurrencies like Bitcoin and Ethereum, has introduced a new dimension to investment. While highly volatile, some view Bitcoin as a potential ‘digital gold’ – a store of value that is decentralized and immune to government-induced inflation. Furthermore, investments in blockchain technology companies or decentralized finance (DeFi) protocols could offer significant growth potential. However, due to their inherent risks, a cautious and well-researched approach with a small, diversified allocation is paramount for any Wealth Preservation 2026 strategy involving digital assets.

Structured Products and Derivatives

For sophisticated investors, structured products and derivatives can be tailored to provide specific inflation hedges or enhanced returns with defined risk parameters. Options, futures, and swaps can be used to mitigate specific risks (e.g., currency fluctuations, interest rate spikes) or to gain exposure to certain asset classes efficiently. These instruments require a deep understanding of financial markets and are typically managed by professional advisors as part of a broader Wealth Preservation 2026 strategy.

Tax-Efficient Wealth Preservation in 2026

Inflation erodes the real value of your money, but taxes can further diminish your investment returns. A crucial aspect of Wealth Preservation 2026 is optimizing your portfolio for tax efficiency. This means strategically utilizing tax-advantaged accounts and understanding the tax implications of your investment decisions.

Leveraging Tax-Advantaged Accounts

- Retirement Accounts (401(k), IRA, Roth IRA): These accounts offer tax deferral or tax-free growth, allowing your investments to compound more effectively without immediate tax drag. Maximizing contributions to these vehicles should be a cornerstone of your Wealth Preservation 2026 plan.

- Health Savings Accounts (HSAs): Often called the ‘triple tax advantage’ account, HSAs offer tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For those eligible, they are a powerful tool for long-term wealth building and preservation.

- 529 Plans: For education savings, 529 plans offer tax-free growth and tax-free withdrawals for qualified educational expenses. They are an excellent way to shield a portion of your wealth from taxes while planning for future costs that are also likely to be impacted by inflation.

Capital Gains and Income Tax Strategies

Actively managing your portfolio to minimize capital gains taxes can significantly boost your after-tax returns. Strategies include:

- Tax-Loss Harvesting: Selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income.

- Long-Term Capital Gains: Holding investments for over a year to qualify for lower long-term capital gains rates.

- Location of Assets: Placing income-generating assets (e.g., bonds, REITs) in tax-deferred accounts and growth-oriented assets (e.g., stocks) in taxable accounts if they are expected to generate long-term capital gains.

Consulting with a qualified tax advisor is essential to tailor these strategies to your specific financial situation and ensure compliance with evolving tax laws in 2026, further strengthening your Wealth Preservation 2026 efforts.

Behavioral Finance and Emotional Discipline in 2026

Beyond the technical aspects of investment, human psychology plays a profound role in Wealth Preservation 2026. Fear and greed, especially during periods of economic uncertainty and inflation, can lead to impulsive decisions that undermine well-laid plans. Maintaining emotional discipline is as crucial as selecting the right assets.

Avoiding Panic Selling and Chasing Returns

When inflation fears grip the market, or when certain asset classes experience rapid, unsustainable growth, the temptation to panic sell or chase returns is strong. Both actions can be detrimental. Panic selling locks in losses, while chasing returns often leads to buying at the peak. A disciplined approach, sticking to your predetermined Wealth Preservation 2026 strategy, and rebalancing your portfolio periodically can help mitigate these behavioral biases.

The Importance of a Financial Advisor

A seasoned financial advisor can provide an objective perspective, helping you navigate market volatility and avoid emotional pitfalls. They can assist in crafting a personalized Wealth Preservation 2026 plan, ensuring it aligns with your risk tolerance and long-term goals. Their expertise in asset allocation, tax planning, and understanding complex financial instruments can be invaluable, especially when facing a 4% inflation rate.

Estate Planning and Legacy for 2026

True Wealth Preservation 2026 extends beyond your lifetime. Effective estate planning ensures that your assets are protected and distributed according to your wishes, minimizing taxes and administrative burdens for your beneficiaries. In an inflationary environment, the value of your estate can be significantly impacted, making thoughtful planning even more critical.

Reviewing and Updating Your Estate Plan

As asset values fluctuate due to inflation, the composition and value of your estate can change. Regularly reviewing and updating your will, trusts, and beneficiary designations is essential. This ensures that your estate plan remains aligned with your current financial situation and objectives for Wealth Preservation 2026.

Gifting Strategies and Charitable Giving

Strategic gifting during your lifetime can be an effective way to reduce the size of your taxable estate. Utilizing annual gift tax exclusions can allow you to transfer wealth to heirs without incurring gift taxes. Charitable giving can also provide significant tax benefits while supporting causes you care about, contributing to a holistic approach to Wealth Preservation 2026 and legacy planning.

Consideration of Trusts

Various types of trusts can serve different purposes in estate planning, from protecting assets from creditors to providing for minor children or individuals with special needs. Irrevocable trusts, for instance, can remove assets from your taxable estate, offering a powerful tool for Wealth Preservation 2026 against future estate taxes and preserving wealth across generations.

Cybersecurity and Digital Asset Protection in 2026

In an increasingly digital world, Wealth Preservation 2026 must also encompass the protection of your digital assets and financial information from cyber threats. The rise of online banking, digital investment platforms, and cryptocurrency holdings makes cybersecurity an indispensable component of your overall financial security strategy.

Robust Cybersecurity Practices

- Strong Passwords and Multi-Factor Authentication (MFA): Implement unique, complex passwords for all financial accounts and enable MFA wherever possible. This adds an essential layer of security against unauthorized access.

- Secure Networks: Avoid conducting financial transactions on public Wi-Fi. Use a secure, private network or a Virtual Private Network (VPN) to protect your data.

- Regular Software Updates: Keep your operating systems, web browsers, and antivirus software up to date. Software updates often include critical security patches that protect against new vulnerabilities.

- Beware of Phishing and Scams: Be vigilant against phishing emails, texts, and calls that attempt to trick you into revealing personal or financial information. Always verify the sender before clicking links or providing data.

Protecting Digital Investments

For those holding cryptocurrencies or other digital assets, specific security measures are crucial:

- Hardware Wallets: Store cryptocurrencies in hardware wallets (cold storage) for maximum security, especially for significant holdings.

- Reputable Exchanges: Use only well-established and regulated cryptocurrency exchanges with strong security protocols.

- Backup Seed Phrases: Securely store backup seed phrases offline and in multiple, safe locations.

Integrating robust cybersecurity practices into your daily financial routine is non-negotiable for effective Wealth Preservation 2026 in the digital age. A single breach can have catastrophic consequences for your financial well-being.

Conclusion: A Proactive Stance for Wealth Preservation 2026

The journey to effective Wealth Preservation 2026 is multifaceted, requiring a strategic blend of diversified investments, tax efficiency, emotional discipline, comprehensive estate planning, and unwavering cybersecurity. While a 4% inflation rate presents a formidable challenge, it is not insurmountable. By understanding the economic landscape, embracing innovative financial tools, and maintaining a proactive stance, you can not only protect your existing wealth but also position it for substantial growth in the years to come.

Remember, financial planning is not a one-time event but an ongoing process. Regularly review your portfolio, adapt to changing market conditions, and seek professional advice when needed. The future of your financial well-being hinges on the decisions you make today. Equip yourself with these advanced strategies, and confidently navigate the economic complexities of 2026, ensuring your wealth continues to serve your long-term aspirations.