Private vs. Federal Student Loans 2026: Rates, Repayment & Your Best Choice

Anúncios

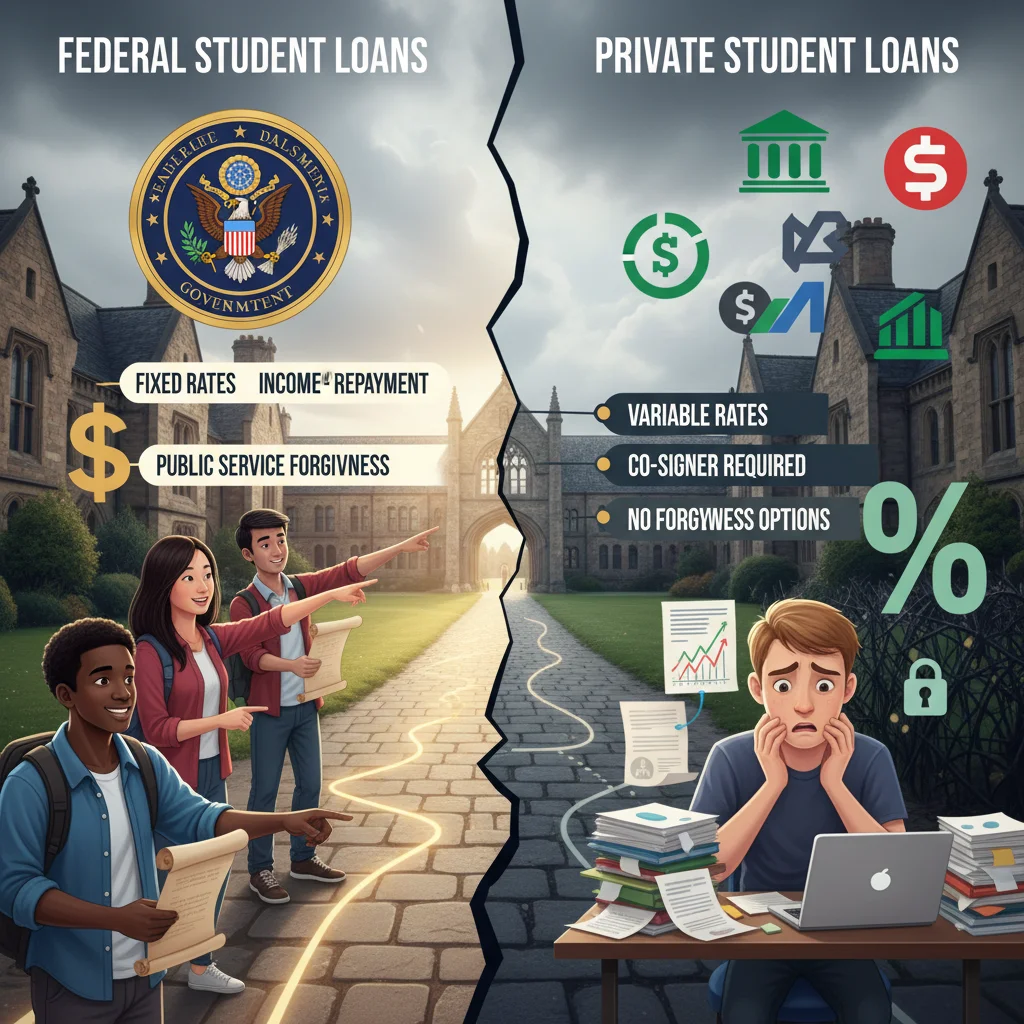

Private vs. Federal Student Loans 2026: A Comparative Analysis of Interest Rates and Repayment Terms

Navigating the landscape of student financing can be one of the most daunting aspects of pursuing higher education. As we look ahead to 2026, understanding the nuances between private and federal student loans becomes even more critical. The choices made today will have a profound impact on your financial future for decades to come. This comprehensive guide aims to demystify the complexities surrounding student loans 2026, offering a clear comparative analysis of interest rates, repayment terms, and crucial considerations to help you make the most informed decision.

Anúncios

The Foundation: Understanding Federal Student Loans in 2026

Federal student loans are often considered the first and best option for most students due to their borrower-friendly terms and various protections. These loans are funded by the U.S. government and come with a host of benefits not typically found in private loan options. As we approach 2026, while specific policy changes might occur, the core structure and benefits of federal loans are expected to remain largely consistent.

Anúncios

Key Types of Federal Student Loans

- Direct Subsidized Loans: These are available to undergraduate students with demonstrated financial need. The U.S. Department of Education pays the interest while you’re in school at least half-time, during your grace period, and during deferment. This is a significant advantage, as it means the loan balance won’t grow while you’re focused on your studies.

- Direct Unsubsidized Loans: Available to undergraduate and graduate students, regardless of financial need. Interest accrues from the moment the loan is disbursed, even while you are in school. You can choose to pay the interest as it accrues or allow it to be capitalized (added to your principal balance) at repayment.

- Direct PLUS Loans: These are available to graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). Eligibility is not based on financial need, but a credit check is required. Borrowers with adverse credit histories may need an endorser.

- Direct Consolidation Loans: These allow you to combine multiple federal student loans into a single loan with one servicer and one monthly payment. This can simplify repayment but may extend the repayment period, potentially leading to more interest paid over the life of the loan.

Interest Rates for Federal Student Loans in 2026

Federal student loan interest rates are set by Congress and are fixed for the life of the loan. This means your interest rate won’t change, providing predictability in your repayment plan. While the exact rates for the 2025-2026 academic year won’t be finalized until mid-2025, they are typically determined based on the 10-year Treasury note auction results. Historically, these rates have been lower than those offered by private lenders, especially for borrowers with less-than-perfect credit. For context, recent federal loan rates have ranged from approximately 4% to 7.5%, depending on the loan type and borrower status (undergraduate, graduate, or PLUS). It’s crucial to monitor official Department of Education announcements for the precise figures as 2026 approaches to fully understand the cost of your student loans 2026.

Repayment Terms and Flexibility of Federal Student Loans

One of the most compelling advantages of federal student loans is the extensive array of repayment options and borrower protections. These are designed to help borrowers manage their debt, especially during times of financial hardship.

- Standard Repayment Plan: Payments are fixed and spread out over 10 years.

- Graduated Repayment Plan: Payments start low and gradually increase, typically every two years, over a 10-year period.

- Extended Repayment Plan: For borrowers with more than $30,000 in federal student loan debt, this plan allows for fixed or graduated payments over up to 25 years.

- Income-Driven Repayment (IDR) Plans: These plans (Income-Based Repayment, Pay As You Earn, Revised Pay As You Earn, and Income-Contingent Repayment) cap your monthly payments at an affordable percentage of your discretionary income. Any remaining balance after 20 or 25 years of payments (depending on the plan and loan type) may be forgiven, though the forgiven amount may be taxable. These plans are invaluable for borrowers with lower incomes relative to their debt.

- Forbearance and Deferment: These options allow you to temporarily postpone or reduce your loan payments if you’re experiencing financial difficulty, unemployment, or returning to school. Interest may or may not accrue during these periods, depending on the loan type and the specific program.

- Loan Forgiveness Programs: Federal loans offer various forgiveness programs, such as Public Service Loan Forgiveness (PSLF) for those working in qualifying public service jobs, and teacher loan forgiveness. These programs can significantly reduce or eliminate debt for eligible borrowers.

The Alternative: Exploring Private Student Loans in 2026

Private student loans are offered by banks, credit unions, and other financial institutions. Unlike federal loans, they are not guaranteed by the government and typically have fewer borrower protections. They are often used to bridge the gap between the cost of attendance and what federal aid and personal savings can cover. When considering private student loans 2026, a thorough understanding of their terms is paramount.

Key Characteristics of Private Student Loans

- Credit-Based Eligibility: Private lenders heavily rely on a borrower’s creditworthiness. Students with limited credit history often need a co-signer (usually a parent or another adult with good credit) to qualify and secure favorable interest rates.

- Variable vs. Fixed Interest Rates: Private loans commonly offer both variable and fixed interest rates. Variable rates can fluctuate with market conditions (e.g., Prime Rate or LIBOR/SOFR), potentially leading to lower initial payments but also the risk of higher payments later. Fixed rates remain constant but might start higher than initial variable rates.

- Fewer Borrower Protections: Private loans generally do not offer income-driven repayment plans, extensive deferment/forbearance options, or loan forgiveness programs like federal loans do.

- Loan Limits: Loan limits are determined by the lender and are typically based on the cost of attendance, minus any other financial aid received.

Interest Rates for Private Student Loans in 2026

Private student loan interest rates for 2026 will be largely dependent on market conditions, the lender, and the borrower’s (or co-signer’s) credit score and history. Good credit can secure competitive rates, sometimes even lower than federal unsubsidized rates, particularly for variable-rate loans. However, borrowers with poor credit or no credit history will likely face much higher rates. It’s not uncommon for private loan rates to range from 3% to 15% or more, showcasing a much wider spectrum than federal rates. The best rates are usually reserved for those with excellent credit scores (typically 700+) and a strong financial history. It’s vital to shop around and compare offers from multiple lenders to find the most favorable terms for your private student loans 2026.

Repayment Terms and Flexibility of Private Student Loans

Private loan repayment terms are set by the individual lenders and can vary significantly. Common repayment periods range from 5 to 15 years, though some lenders offer longer terms. Unlike federal loans, there’s less standardization in repayment plans.

- Immediate Repayment: Some private loans require payments of both principal and interest while you’re still in school.

- Interest-Only Repayment: You pay only the interest while in school, deferring principal payments until after graduation.

- Deferred Repayment: Similar to federal loans, you can defer all payments until after graduation or leaving school, though interest will likely accrue during this period.

- Limited Forbearance/Deferment: While some private lenders offer limited forbearance options, they are generally less generous and less structured than federal programs. These are often granted on a case-by-case basis and may not be available for as long or for as many reasons as federal options.

Comparative Analysis: Federal vs. Private Student Loans 2026

To make the best decision for your higher education financing, a direct comparison of federal and private student loans 2026 is essential.

Interest Rates: Stability vs. Variability

Federal Loans: Offer fixed interest rates, providing predictable monthly payments and protection against market fluctuations. These rates are generally lower and more accessible to all students, regardless of credit history.

Private Loans: Can have fixed or variable rates. While variable rates might start lower, they carry the risk of increasing over time. Fixed rates offer stability but may be higher than federal options, especially for borrowers without excellent credit. The rates are highly dependent on the borrower’s credit profile.

Repayment Flexibility and Borrower Protections

Federal Loans: Excel in this area with a wide range of income-driven repayment plans, generous deferment and forbearance options, and potential for loan forgiveness. These features act as a safety net, protecting borrowers during periods of financial hardship.

Private Loans: Offer very limited flexibility. Income-driven repayment is typically unavailable, and deferment or forbearance options are at the discretion of the lender and often for shorter periods. Loan forgiveness is almost non-existent outside of specific refinancing programs.

Eligibility Requirements

Federal Loans: Primarily based on financial need (for subsidized loans) and enrollment status. Most students qualify for some form of federal aid, regardless of credit history (except for PLUS loans, which require a credit check but are more lenient than private lenders).

Private Loans: Heavily reliant on creditworthiness. A good credit score or a creditworthy co-signer is almost always required to secure a private loan, especially one with favorable terms.

Application Process

Federal Loans: Requires completing the Free Application for Federal Student Aid (FAFSA). This single application determines eligibility for various federal grants, scholarships, and loans.

Private Loans: Involves applying directly to individual lenders. Each application may require a credit check and may impact your credit score. It can be a more time-consuming process if applying to multiple lenders.

Making the Right Choice for Your Student Loans 2026

The decision between federal and private student loans, or a combination of both, should be a strategic one. Here’s a recommended approach:

1. Maximize Federal Loan Options First

Always start by completing the FAFSA as early as possible. Exhaust all federal loan options, particularly Direct Subsidized Loans, before considering private alternatives. The benefits, such as fixed rates, income-driven repayment, and potential for forgiveness, are simply unmatched.

2. Understand Your Financial Need

Determine the actual cost of attendance for your chosen institution, including tuition, fees, room, board, books, and living expenses. Subtract any grants, scholarships, and federal loans you’ve been awarded. The remaining gap is what you might need to cover with private loans or other resources.

3. Evaluate Your Creditworthiness

If you anticipate needing private loans, check your credit score (and your co-signer’s, if applicable). A higher score will lead to better interest rates. Work to improve your credit before applying if possible.

4. Shop Around for Private Loans

If private loans are necessary, compare offers from multiple lenders. Look beyond just the interest rate; consider fees, repayment terms, and any borrower benefits they might offer. Read the fine print carefully.

5. Consider Future Income and Career Path

Your expected income after graduation should influence your borrowing decisions. If you anticipate a lower-paying career, the flexible repayment options of federal loans become even more critical. If you’re entering a high-paying field, you might be more comfortable with the potentially less flexible terms of private loans.

6. Be Wary of Co-signer Release Options

If you need a co-signer for a private loan, inquire about co-signer release options. Some lenders allow you to release your co-signer after a certain number of on-time payments, provided you meet specific credit criteria. This can be an important consideration for both you and your co-signer.

Potential Changes and Trends for Student Loans 2026

While the core distinctions between federal and private loans are likely to persist, the financial landscape is always evolving. Here are some trends and potential changes that could impact student loans 2026:

Government Policy Shifts

The U.S. government continuously evaluates and sometimes reforms federal student aid programs. Future legislative changes could affect interest rate formulas, eligibility for specific loan types, or the terms of income-driven repayment and loan forgiveness programs. Keeping an eye on federal policy discussions will be important.

Interest Rate Environment

Overall economic conditions, particularly inflation and the Federal Reserve’s monetary policy, will influence both federal and private student loan interest rates. A rising interest rate environment could mean higher costs for new loans in 2026.

Technological Advancements in Lending

Fintech companies are continually innovating in the lending space. We might see more streamlined application processes, personalized repayment tools, or alternative credit assessment methods from private lenders, potentially expanding access or offering different terms.

Focus on Student Outcomes

There’s an increasing emphasis on accountability in higher education. This could lead to more scrutiny on institutions whose graduates struggle with heavy debt burdens, potentially influencing future lending policies or even institutional aid practices.

The Importance of Financial Literacy

Regardless of whether you choose federal or private student loans 2026, developing strong financial literacy skills is paramount. Understanding concepts like compound interest, credit scores, budgeting, and debt management will empower you to make responsible borrowing decisions and successfully navigate repayment.

- Budgeting: Create a realistic budget to understand how much you truly need to borrow and how much you can afford to pay back each month.

- Emergency Fund: While federal loans offer flexibility, having an emergency fund can provide an extra layer of protection against unexpected financial challenges that might impact your ability to repay.

- Credit Monitoring: Regularly check your credit report to ensure accuracy and monitor for any fraudulent activity, especially if you have private loans.

- Proactive Communication: If you anticipate difficulty making payments, contact your loan servicer immediately. Federal servicers can guide you through available options, and some private lenders may offer limited assistance.

Conclusion: Your Strategic Approach to Student Loans 2026

Financing your education in 2026 requires a strategic and informed approach. Federal student loans, with their inherent protections, fixed rates, and flexible repayment plans, should always be your primary consideration. They offer a safety net that private loans simply cannot match. Private student loans can serve as a necessary supplement once federal options are exhausted, but they come with greater risk, higher dependence on creditworthiness, and fewer borrower safeguards.

By thoroughly researching current interest rates, understanding the nuances of repayment terms, and evaluating your personal financial situation, you can confidently make decisions regarding your student loans 2026. Remember, the goal is not just to secure funding for your education, but to do so in a way that positions you for long-term financial success, minimizing the burden of debt and maximizing your post-graduation opportunities. Stay informed, ask questions, and choose wisely to invest in your future.