Parent PLUS Loans 2026: Rates, Repayment, & Financial Impact Guide

Anúncios

Navigating the complex landscape of college financing can be daunting for many families. Among the myriad options available, Parent PLUS Loans stand out as a significant federal loan program designed to help parents cover their children’s educational expenses. As we look towards 2026, understanding the nuances of these loans, particularly their interest rates and repayment options, becomes crucial for effective financial planning. This comprehensive guide aims to demystify Parent PLUS Loans, offering insights into their current interest rate of 8.05%, exploring various repayment strategies, and providing practical solutions to manage their financial impact.

Anúncios

What Are Parent PLUS Loans?

Parent PLUS Loans, officially known as Direct PLUS Loans for Parents, are federal loans that graduate or professional students and parents of dependent undergraduate students can use to help pay for education expenses not covered by other financial aid. Unlike other federal student loans, Parent PLUS Loans require a credit check. However, they are not based on financial need, meaning eligibility is primarily determined by the borrower’s creditworthiness and the cost of attendance less any other financial aid received.

Anúncios

These loans are disbursed directly to the school to cover tuition, fees, room and board, books, and other educational costs. While they offer a valuable means to bridge funding gaps, it’s essential for parents to understand the full scope of their obligations, especially concerning interest rates and repayment terms.

Parent PLUS Loans in 2026: The Current Interest Rate Landscape

For the academic year 2025-2026, the interest rate for Parent PLUS Loans is set at 8.05%. This rate is fixed for the life of the loan, meaning it will not change once the loan is disbursed. Understanding this fixed rate is paramount for long-term financial planning, as it directly impacts the total cost of borrowing.

Federal student loan interest rates, including those for Parent PLUS Loans, are determined annually by Congress. They are typically based on the 10-year Treasury note yield plus a fixed add-on, capped by a maximum rate. While the 8.05% rate for 2025-2026 might seem high compared to some other loan types, it’s crucial to compare it with private loan options, which can sometimes carry even higher variable rates or stricter repayment terms.

How the Interest Rate Impacts Your Loan

A fixed interest rate of 8.05% means that for every $10,000 borrowed, you will accrue approximately $805 in interest each year. Over the typical 10-year repayment period, this can add a significant amount to the principal balance. For example, a $30,000 Parent PLUS Loan at 8.05% over 10 years would result in total payments far exceeding the initial borrowed amount.

- Higher Monthly Payments: A higher interest rate translates to larger monthly payments, making it potentially more challenging to manage your budget.

- Increased Total Cost: The overall cost of the loan, including principal and interest, will be substantially higher with an 8.05% rate compared to lower rates.

- Long-Term Financial Commitment: Parents often carry these loans well into their retirement years, making the fixed interest rate a long-term financial commitment that requires careful consideration.

Understanding Parent PLUS Loan Eligibility and Application

Before diving into repayment, it’s essential to understand who can apply for Parent PLUS Loans and the application process itself. Eligibility is straightforward but crucial:

- Be a Biological or Adoptive Parent (or, in some cases, a stepparent): The parent must be the biological or adoptive parent of a dependent undergraduate student enrolled at least half-time at an eligible school.

- Good Credit History: Unlike other federal student loans, Parent PLUS Loans require a credit check. While a pristine credit score isn’t always necessary, borrowers cannot have an adverse credit history. An adverse credit history generally includes conditions like bankruptcy, foreclosure, tax lien, or wage garnishment within certain timeframes.

- Meet General Federal Student Aid Requirements: Both the parent and student must meet general eligibility requirements for federal student aid, such as U.S. citizenship or eligible non-citizen status.

The Application Process

Applying for a Parent PLUS Loan involves a few key steps:

- Complete the FAFSA: The student must first complete the Free Application for Federal Student Aid (FAFSA). This determines the student’s eligibility for other federal aid, which can reduce the amount of Parent PLUS Loan needed.

- Complete the PLUS Loan Application: Parents apply for the loan directly through StudentAid.gov. This application includes a credit check.

- Sign a Master Promissory Note (MPN): If approved, the parent must sign an MPN, which is a legal document promising to repay the loan.

- Entrance Counseling: While not always mandatory for Parent PLUS Loan borrowers, some schools may require entrance counseling to ensure borrowers understand their rights and responsibilities.

It’s important to apply for the loan well in advance of when the funds are needed, as processing times can vary.

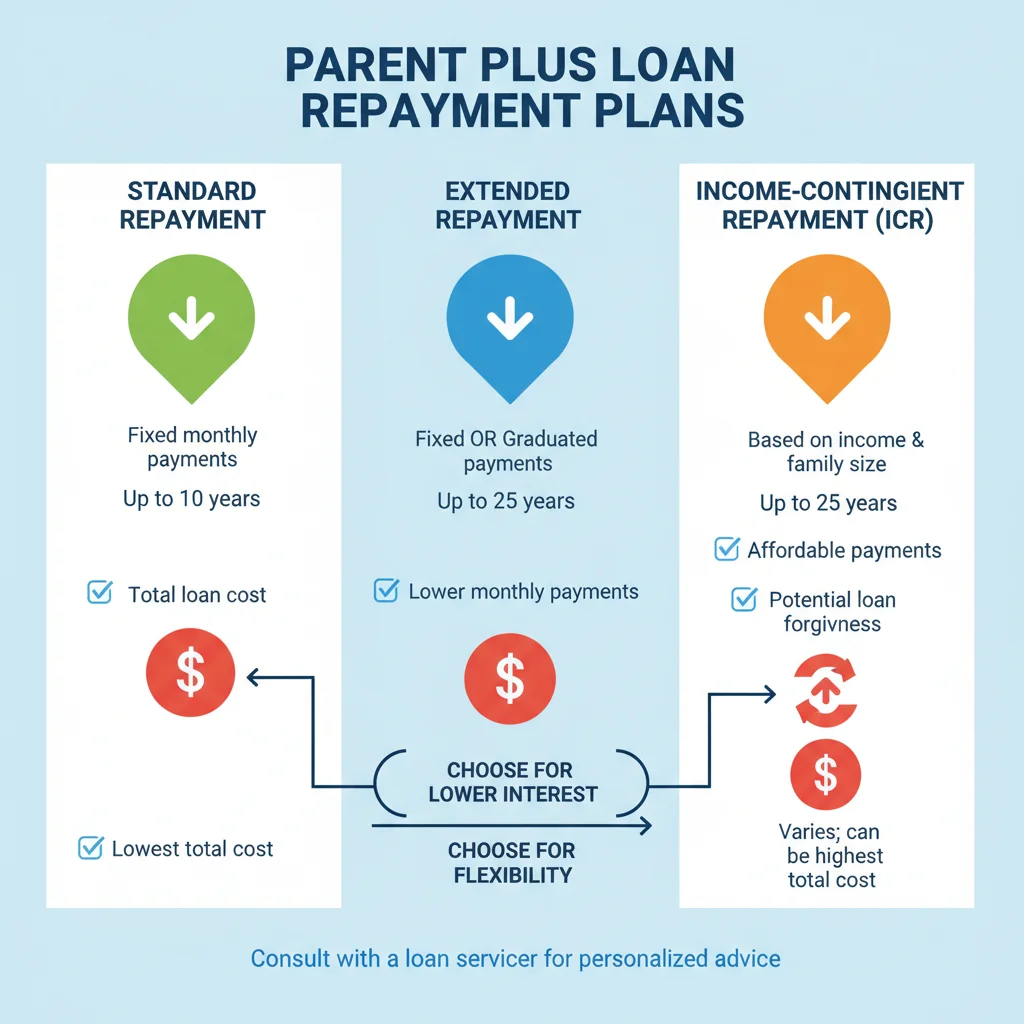

Exploring Repayment Options for Parent PLUS Loans

One of the most critical aspects of managing Parent PLUS Loans is understanding the various repayment options available. While the standard repayment plan is typically 10 years, there are alternatives that can significantly impact your monthly payments and overall financial burden, especially with an 8.05% interest rate.

Standard Repayment Plan

This is the default plan for most federal loans. Payments are fixed and typically made over 10 years. While this plan ensures the loan is paid off relatively quickly and often results in the least amount of interest paid over the life of the loan, the monthly payments can be substantial, especially for larger loan amounts at 8.05%.

Extended Repayment Plan

If you need lower monthly payments than the Standard Plan offers, the Extended Repayment Plan might be an option. This plan allows you to repay your loans over a period of up to 25 years. You can choose to have fixed or graduated payments (payments that start low and increase over time). While this lowers your monthly burden, it generally results in paying more interest over the long term.

Graduated Repayment Plan

Similar to the Extended Plan, the Graduated Repayment Plan allows for a longer repayment period (up to 10 years, or up to 25 years under the Extended Graduated option). Payments start low and increase every two years. This can be beneficial if your income is expected to rise over time, but like the Extended Plan, you’ll likely pay more in total interest.

Income-Contingent Repayment (ICR) Plan

This is the only income-driven repayment (IDR) plan directly available for Parent PLUS Loans. However, to qualify for ICR, Parent PLUS Loans must first be consolidated into a Direct Consolidation Loan. Once consolidated, your monthly payment will be the lesser of:

- 20% of your discretionary income, or

- What you would pay on a fixed 12-year repayment plan, adjusted according to your income.

Payments are recalculated annually based on your income and family size. After 25 years of qualifying payments, any remaining balance may be forgiven, though the forgiven amount might be subject to income tax.

Deferment and Forbearance

In certain circumstances, such as economic hardship, unemployment, or during the student’s enrollment, you might be eligible for deferment or forbearance. These options allow you to temporarily postpone or reduce your loan payments. However, interest continues to accrue on Parent PLUS Loans during most deferment and all forbearance periods, which can increase your total loan cost significantly.

Strategies to Mitigate the Financial Impact of Parent PLUS Loans

Given the 8.05% interest rate, proactive strategies are essential to manage the financial impact of Parent PLUS Loans effectively. Here are several practical solutions:

1. Borrow Only What You Need

This might seem obvious, but it’s often overlooked. Carefully assess your child’s true educational expenses and subtract all other forms of financial aid (scholarships, grants, student’s federal loans) before determining the amount of Parent PLUS Loan needed. Every dollar borrowed at 8.05% will cost significantly more in the long run.

2. Make Interest Payments During In-School Deferment

Parent PLUS Loans typically have a deferment period while the student is enrolled at least half-time. While payments are not required during this time, interest still accrues. If you can afford it, making interest-only payments during this period can prevent the interest from capitalizing (being added to the principal balance), thereby reducing the total amount you repay.

3. Consider Refinancing Parent PLUS Loans

Once the student has graduated and you are in repayment, you might consider refinancing your Parent PLUS Loans with a private lender. Refinancing can potentially lower your interest rate, especially if you have excellent credit, or allow you to choose a different repayment term. However, refinancing federal loans into private loans means losing federal loan benefits, such as access to income-driven repayment plans (like ICR) and certain deferment/forbearance options. This decision requires careful consideration of your financial situation and risk tolerance.

4. Explore Loan Consolidation

Consolidating your Parent PLUS Loans into a Direct Consolidation Loan can simplify repayment by combining multiple federal loans into one, resulting in a single monthly payment. The interest rate on a Direct Consolidation Loan is the weighted average of the interest rates of the loans being consolidated, rounded up to the nearest one-eighth of a percentage point. Crucially, consolidation is a prerequisite for Parent PLUS Loans to become eligible for the Income-Contingent Repayment (ICR) plan.

5. Aggressive Repayment

If your budget allows, making extra payments or paying more than the minimum monthly amount can significantly reduce the total interest paid and shorten the repayment period. Directing extra payments towards the principal balance can save you thousands over the life of the loan, especially with an 8.05% interest rate.

6. Communication and Collaboration with Your Student

Open dialogue with your student about the financial responsibilities associated with their education is vital. While Parent PLUS Loans are solely in the parent’s name, students can contribute to repayment once they graduate and are employed. This shared understanding can foster a sense of responsibility and potentially ease the financial burden on parents.

The Long-Term Outlook: Financial Planning Beyond Graduation

The decision to take out Parent PLUS Loans extends far beyond the student’s graduation day. For many parents, these loans become a significant part of their retirement planning, impacting savings, investments, and overall financial security. With the 8.05% interest rate for 2025-2026, the long-term implications are even more pronounced.

Impact on Retirement Savings

Servicing Parent PLUS Loan debt can divert funds that would otherwise be allocated to retirement accounts, such as 401(k)s or IRAs. This can lead to a delayed retirement or a less comfortable financial situation in later years. It’s crucial to balance current loan payments with future financial goals.

Credit Score Considerations

While Parent PLUS Loans can help establish or maintain a good credit history if managed responsibly, missed payments or defaults can severely damage a parent’s credit score. A strong credit score is vital for other financial endeavors, such as securing a mortgage, buying a car, or even obtaining competitive insurance rates.

Estate Planning

Unlike some private loans, federal Parent PLUS Loans are discharged upon the death of the parent borrower or the student for whom the loan was taken. While this offers a safety net, it’s a grim consideration that highlights the serious nature of the financial commitment.

Alternatives to Parent PLUS Loans

Before committing to Parent PLUS Loans, it’s wise to explore all other available funding sources. These alternatives can often come with lower interest rates or more favorable repayment terms.

- Federal Student Loans (in the student’s name): Direct Subsidized and Unsubsidized Loans offered directly to students typically have lower fixed interest rates and more flexible repayment options, including several income-driven plans. Students should maximize these options first.

- Scholarships and Grants: These are forms of financial aid that do not need to be repaid. Encourage your student to apply for as many as possible, based on merit, need, demographics, or specific talents.

- Student Employment: A part-time job or work-study program can help students cover some of their expenses, reducing the need for loans.

- Personal Savings: If possible, utilizing personal savings can be a good way to cover educational costs without incurring debt.

- Private Student Loans: While often a last resort, private loans can sometimes offer competitive interest rates for borrowers with excellent credit. However, they lack the federal protections and flexible repayment options of federal loans, so compare them carefully with Parent PLUS Loans.

- Home Equity Loans or Lines of Credit (HELOCs): If you own a home, you might consider using its equity. These loans often have lower interest rates than Parent PLUS Loans, but they come with the significant risk of putting your home up as collateral.

Key Takeaways for Parent PLUS Loan Borrowers

The 8.05% interest rate for Parent PLUS Loans in 2026 underscores the necessity for careful planning and informed decision-making. Here are the essential takeaways:

- Understand the Costs: Be fully aware of the fixed 8.05% interest rate and how it will impact your monthly payments and total repayment amount over the life of the loan.

- Explore All Repayment Options: Don’t default to the standard plan. Investigate Extended, Graduated, and especially the Income-Contingent Repayment (ICR) plan (after consolidation) to find the best fit for your financial situation.

- Consider Refinancing Carefully: Refinancing can offer lower rates but means losing federal protections. Weigh the pros and cons meticulously.

- Prioritize Other Aid First: Maximize scholarships, grants, and federal loans in the student’s name before turning to Parent PLUS Loans.

- Communicate Openly: Discuss financial responsibilities with your student to ensure a shared understanding and potential collaboration in repayment.

- Plan for the Long Term: Recognize that these loans are a long-term financial commitment that can affect your retirement and other financial goals.

Conclusion: Making Informed Decisions for Your Family’s Future

Parent PLUS Loans serve as a critical tool for many families seeking to provide their children with higher education opportunities. However, with the current 8.05% interest rate, it’s more important than ever to approach these loans with a clear understanding of their implications. By carefully assessing your needs, exploring all available repayment options, and considering alternative funding sources, you can make informed decisions that safeguard your family’s financial well-being while investing in your child’s future.

Remember, financial literacy is your most powerful asset when navigating student debt. Take the time to research, consult with financial advisors if necessary, and choose the path that best aligns with your long-term financial goals.

")