Maximize Your 2026 401(k) Contributions: A Comprehensive Retirement Planning Guide

Retirement planning is a journey, not a destination, and one of the most powerful vehicles for securing your financial future is your 401(k). As we look ahead to 2026, understanding the nuances of contribution limits, strategic planning, and optimization techniques becomes paramount. For many, the goal isn’t just to save, but to maximize 401k 2026 contributions to take full advantage of tax benefits and compound growth. This comprehensive guide will walk you through everything you need to know to ensure your retirement savings are on the right track, providing actionable insights and expert advice.

Anúncios

The landscape of retirement savings is constantly evolving, with contribution limits, regulations, and investment opportunities changing year to year. Staying informed is crucial for making the best decisions for your financial well-being. Whether you’re just starting your career or nearing retirement, optimizing your 401(k) can make a substantial difference in your golden years. We’ll delve into the specifics of what to expect in 2026, how to leverage employer matching, the power of catch-up contributions, and smart investment strategies to grow your nest egg.

Anúncios

Understanding 401(k) Basics for 2026

Before we dive into advanced strategies, let’s establish a solid understanding of what a 401(k) is and why it’s such a critical component of retirement planning. A 401(k) is an employer-sponsored defined-contribution retirement plan. It allows employees to contribute a portion of their pre-tax (or post-tax, in the case of Roth 401(k)s) salary to an investment account, with investments growing tax-deferred until retirement. The primary advantage lies in its tax benefits and, often, employer matching contributions, which essentially provide free money for your retirement.

For 2026, while the official IRS contribution limits are typically announced in the fall of the preceding year, we can anticipate them based on inflation adjustments and historical trends. Generally, these limits see a slight increase annually, reflecting the rising cost of living. It’s vital to stay updated with the latest figures from the IRS or your plan administrator to accurately maximize 401k 2026 contributions. These limits apply to the total amount you can contribute from your salary, excluding any employer contributions.

Beyond the standard employee contribution limit, there’s also a separate limit for total contributions (employee + employer). This often overlooked detail is important for high-income earners or those with very generous employer plans. Understanding both your individual contribution limit and the overall plan limit is key to ensuring you’re not leaving any potential savings on the table.

The Power of Tax-Advantaged Growth

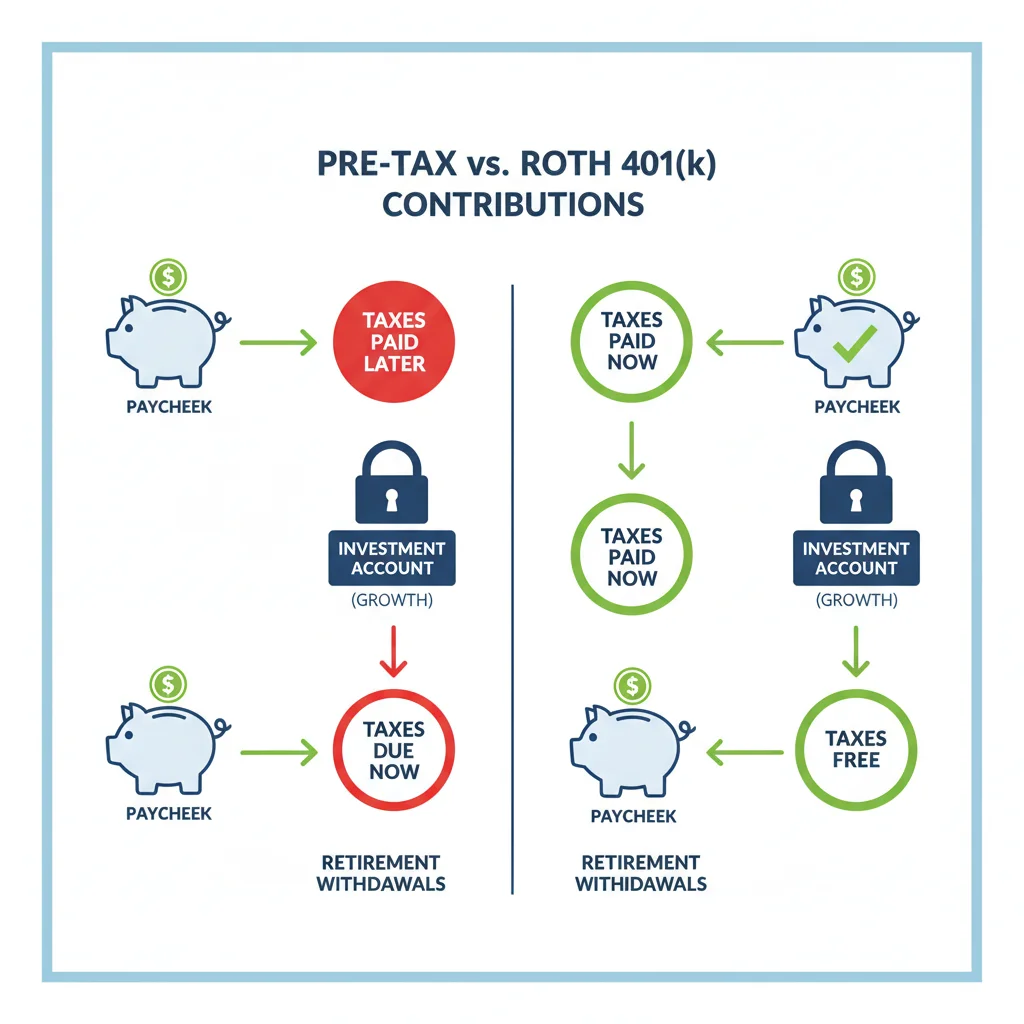

One of the most compelling reasons to contribute to a 401(k) is the tax-advantaged growth. For traditional 401(k)s, your contributions are made on a pre-tax basis, meaning they reduce your taxable income in the year you contribute. This can lead to immediate tax savings. The investments within your 401(k) then grow tax-deferred, meaning you don’t pay taxes on capital gains or dividends until you withdraw the money in retirement. This allows your investments to compound more aggressively over time, as you’re not losing a portion to taxes each year.

Roth 401(k)s offer a different tax advantage: contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This can be particularly beneficial if you anticipate being in a higher tax bracket in retirement than you are today. The choice between a traditional and Roth 401(k) depends on your current income, future income projections, and overall tax strategy. Many plans offer both options, allowing you to diversify your tax exposure in retirement. Consulting with a financial advisor can help you determine which option, or combination of options, is best for your situation to effectively maximize 401k 2026 benefits.

Key Strategies to Maximize 401(k) 2026 Contributions

Now that we’ve covered the basics, let’s explore actionable strategies to ensure you’re getting the most out of your 401(k) in 2026. These strategies go beyond simply contributing and focus on optimizing every aspect of your plan.

1. Hit the Employee Contribution Limit

The most straightforward way to maximize 401k 2026 contributions is to contribute the maximum allowed by the IRS. As mentioned, the exact limits for 2026 will be released later, but aiming for the projected maximum is a smart move. For 2024, the limit for employee contributions was $23,000. Assuming a modest increase for inflation, the 2026 limit could be around $24,500 – $25,500. Regularly check the IRS website or your plan administrator for the definitive numbers.

Breaking this down into monthly or bi-weekly contributions can make it seem less daunting. For example, if the limit is $25,000 for 2026, that’s roughly $2,083 per month. Adjusting your payroll deductions at the beginning of the year ensures you stay on track to hit the maximum without overshooting or undershooting. Automating these contributions is crucial for consistency and avoiding the temptation to spend money that could be saving for your future.

2. Don’t Miss Out on Employer Matching

Employer matching is often considered "free money" and is one of the most significant benefits of a 401(k). Many employers will match a percentage of your contributions up to a certain limit. For instance, an employer might match 50% of your contributions up to 6% of your salary. This means if you contribute 6% of your salary, your employer adds another 3%, effectively giving you a 50% immediate return on that portion of your investment.

Failing to contribute at least enough to get the full employer match is a common and costly mistake. Always prioritize contributing at least the minimum required to receive the full match before considering other savings vehicles. If you can only afford to contribute a small percentage of your salary, make sure that percentage is enough to unlock your employer’s full contribution. This is a fundamental step to truly maximize 401k 2026 growth.

3. Leverage Catch-Up Contributions (Age 50 and Over)

If you are age 50 or older by the end of 2026, the IRS allows you to make additional "catch-up" contributions to your 401(k) above the standard employee limit. This provision is designed to help older workers boost their retirement savings as they get closer to retirement. For 2024, the catch-up contribution limit was $7,500. It’s reasonable to expect a similar or slightly higher amount for 2026.

These catch-up contributions are a powerful tool for those who may have started saving later in life or who want to accelerate their savings in their peak earning years. If you qualify, making these additional contributions can significantly increase your retirement nest egg. Combine this with the standard employee contribution, and you could be putting away a substantial sum each year, further helping you to maximize 401k 2026 potential.

4. Understand and Utilize Roth 401(k) Options

As briefly touched upon, a Roth 401(k) offers tax-free withdrawals in retirement, provided certain conditions are met. This can be an incredibly valuable option, especially for younger workers who anticipate being in a higher tax bracket later in life, or for those who want to diversify their tax exposure in retirement. By paying taxes on your contributions now, you lock in your tax rate and enjoy tax-free growth and withdrawals later.

Even if you’re a high-income earner, a Roth 401(k) can be accessible when a Roth IRA might not be due to income limitations. If your employer offers a Roth 401(k), consider allocating at least a portion of your contributions to it. This strategy can provide flexibility and potentially significant tax savings in your retirement years. Discussing this with a tax professional can help you determine the optimal allocation to maximize 401k 2026 tax benefits for your specific situation.

5. Consider After-Tax 401(k) Contributions (Mega Backdoor Roth)

For high-income earners who have already maxed out their pre-tax or Roth 401(k) contributions and employer matching, some plans allow for after-tax 401(k) contributions. This is different from a Roth 401(k). These after-tax contributions, combined with your employer’s contributions and your pre-tax/Roth contributions, cannot exceed the overall IRS limit for total contributions to a defined contribution plan (which was $69,000 for 2024, and will likely be higher for 2026).

The magic happens when these after-tax contributions are then converted to a Roth IRA. This strategy, often referred to as the "Mega Backdoor Roth," allows you to funnel a significant amount of money into a Roth account, where it can grow and be withdrawn tax-free in retirement, circumventing the standard Roth IRA income limitations. Not all 401(k) plans allow for after-tax contributions or in-service distributions (which are necessary for the conversion), so check with your plan administrator. This advanced strategy is a powerful way to truly maximize 401k 2026 savings for those with the financial capacity.

Optimizing Your 401(k) Investments for 2026

Contributing the maximum is only half the battle; how you invest those contributions within your 401(k) is equally important. Smart investment choices can significantly impact the growth of your retirement nest egg.

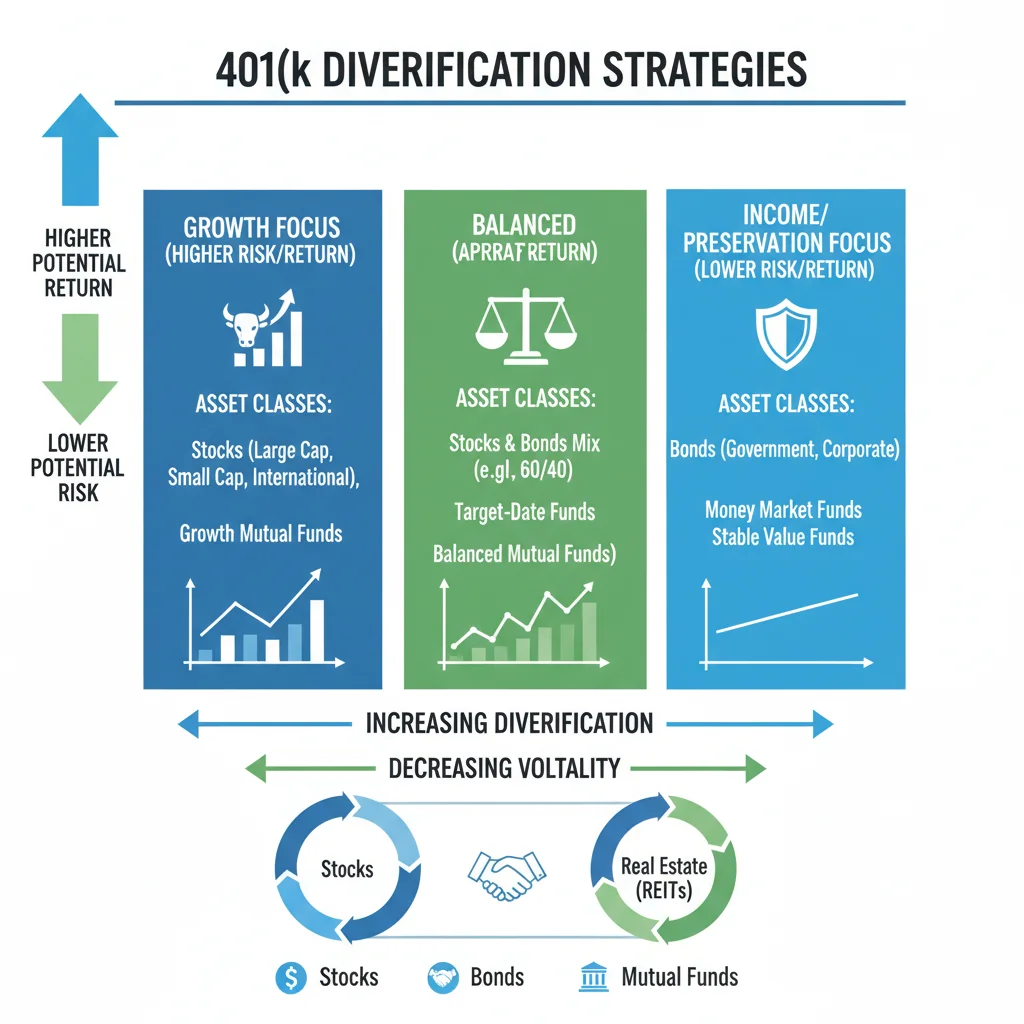

1. Diversification is Key

A well-diversified portfolio is crucial for managing risk and maximizing returns over the long term. Your 401(k) typically offers a selection of mutual funds, exchange-traded funds (ETFs), and sometimes individual stocks. Ensure your investments are spread across different asset classes (e.g., stocks, bonds, real estate), industries, and geographies. This helps protect your portfolio from significant downturns in any single market segment.

Avoid putting all your eggs in one basket, even if a particular asset class has performed exceptionally well recently. Market conditions can change rapidly. Regularly review your asset allocation to ensure it aligns with your risk tolerance and time horizon. A diversified portfolio is more resilient and better positioned to capture growth opportunities across various market cycles, helping you to effectively maximize 401k 2026 returns.

2. Understand Your Risk Tolerance and Time Horizon

Your investment strategy should be tailored to your individual circumstances. If you’re young and have decades until retirement, you can generally afford to take on more risk, focusing on growth-oriented investments like stocks. As you approach retirement, you’ll likely want to shift towards a more conservative allocation, emphasizing capital preservation and income generation with more bonds and stable assets.

Your risk tolerance also plays a significant role. If market volatility causes you undue stress, a more conservative portfolio might be appropriate, even if it means potentially lower returns. The goal is to find a balance that allows you to sleep at night while still making progress towards your retirement goals. Many 401(k) plans offer target-date funds, which automatically adjust their asset allocation over time based on your projected retirement year, providing a convenient "set it and forget it" option for many investors.

3. Minimize Fees

Fees, even seemingly small ones, can eat into your investment returns over time. Pay close attention to the expense ratios of the funds available in your 401(k) plan. A difference of even 0.5% in annual fees can translate to tens of thousands of dollars lost over a 30-year investment horizon. Opt for low-cost index funds or ETFs when available, as they typically have lower expense ratios than actively managed funds.

Beyond fund fees, be aware of any administrative fees associated with your 401(k) plan. While some administrative fees are unavoidable, understanding them allows you to compare your plan’s costs against industry averages. If your plan’s fees seem excessively high, it might be worth discussing with your HR department or plan administrator. Minimizing fees is a crucial, yet often overlooked, component of how to maximize 401k 2026 growth.

4. Rebalance Your Portfolio Regularly

Over time, the performance of different asset classes can cause your portfolio’s original allocation to drift. For example, if stocks have performed exceptionally well, they might now represent a larger percentage of your portfolio than you initially intended. Rebalancing involves selling some of your overperforming assets and buying more of your underperforming ones to bring your portfolio back to your target allocation.

Regular rebalancing (e.g., once a year or when an asset class deviates significantly from its target) helps maintain your desired risk level and can be a disciplined way to "buy low and sell high." Some 401(k) plans offer automatic rebalancing, which can be a convenient feature. If not, schedule a time annually to review and adjust your portfolio manually. This proactive approach helps ensure your investments remain aligned with your long-term goals to maximize 401k 2026 potential.

Beyond the 401(k): Complementary Retirement Savings

While the 401(k) is a cornerstone of retirement planning, it’s often beneficial to utilize other retirement savings vehicles in conjunction with it. Diversifying your savings across different account types can offer additional tax advantages and flexibility.

Individual Retirement Accounts (IRAs)

Traditional and Roth IRAs are excellent complements to a 401(k). If you’ve maxed out your 401(k) contributions (especially if you’re not eligible for the Mega Backdoor Roth), an IRA is the next logical step. The contribution limits for IRAs are separate from 401(k)s, allowing you to save even more each year.

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. Roth IRAs have income limitations for direct contributions, but the "Backdoor Roth" strategy can be an option for high earners.

The choice between a Traditional and Roth IRA, much like their 401(k) counterparts, depends on your current and projected future tax situation. Using both a 401(k) and an IRA allows you to further maximize 401k 2026 and overall retirement savings.

Health Savings Accounts (HSAs)

For those with a high-deductible health plan (HDHP), an HSA can be an incredibly powerful, triple-tax-advantaged savings vehicle. Contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals for medical expenses are also tax-free. If you don’t use the funds for medical expenses, after age 65, they can be withdrawn for any purpose and are taxed like a traditional IRA.

Many financial experts consider HSAs to be "super IRAs" due to their unparalleled tax benefits. If you’re eligible, contributing to an HSA after maxing out your 401(k) and IRA can be an excellent strategy to boost your retirement savings and cover future healthcare costs, which are often a significant expense in retirement. This indirect method helps you to indirectly maximize 401k 2026 by freeing up other funds for direct 401(k) contributions.

Taxable Brokerage Accounts

Once you’ve exhausted all tax-advantaged retirement accounts, a taxable brokerage account is the next step. While these accounts don’t offer the immediate tax deductions or tax-free growth of retirement accounts, they provide liquidity and no contribution limits. Investments held for more than a year typically qualify for lower long-term capital gains tax rates. A diversified portfolio in a brokerage account can provide additional growth potential and flexibility for your overall financial plan, complementing your efforts to maximize 401k 2026 funds.

Regular Review and Adjustment

Retirement planning is not a one-time event; it requires ongoing attention and adjustment. Life circumstances change, market conditions fluctuate, and your financial goals may evolve. Regularly reviewing your 401(k) and overall retirement strategy is crucial.

- Annual Review: At least once a year, preferably at the beginning of the year or during open enrollment, review your 401(k) contributions, investment allocation, and beneficiary designations. Ensure you’re on track to maximize 401k 2026 contributions and that your risk tolerance still aligns with your investment choices.

- Life Events: Major life events such as marriage, divorce, birth of a child, a new job, or a significant salary increase should trigger a review of your retirement plan. These events often present opportunities to increase contributions or adjust your strategy.

- Market Conditions: While you shouldn’t react to every market fluctuation, significant shifts in economic conditions or market trends might warrant a review of your investment strategy. This doesn’t necessarily mean making drastic changes but rather ensuring your portfolio remains resilient.

- Seek Professional Advice: Consider consulting with a certified financial planner (CFP). A CFP can provide personalized advice, help you navigate complex decisions, and ensure your retirement plan is optimized for your specific goals and circumstances. They can offer insights on how to best maximize 401k 2026 and integrate it into your broader financial picture.

Common Mistakes to Avoid

Even with the best intentions, some common pitfalls can hinder your ability to maximize 401k 2026 contributions and growth. Being aware of these can help you steer clear of them:

- Not Contributing Enough: The most significant mistake is not contributing at all or only contributing a minimal amount. Start early, even if it’s a small percentage, and gradually increase it.

- Missing the Employer Match: As discussed, this is free money. Always contribute at least enough to get the full match.

- Being Too Conservative (Especially When Young): While risk management is important, being overly conservative when you have a long time horizon means missing out on significant growth potential from equities.

- Being Too Aggressive (Nearing Retirement): Conversely, maintaining an overly aggressive portfolio close to retirement exposes you to significant market downturns right before you need to start drawing on your funds.

- Ignoring Fees: High fees erode your returns over time. Be diligent about choosing low-cost funds.

- Not Diversifying: Concentrating your investments in a single stock or industry can lead to significant losses if that sector underperforms.

- Cashing Out When Changing Jobs: Resist the temptation to cash out your 401(k) when you leave a job. This incurs taxes and penalties and severely damages your long-term savings. Instead, roll it over into your new employer’s plan or an IRA.

- Forgetting Beneficiaries: Ensure your beneficiary designations are up-to-date. This ensures your assets go to your intended heirs without going through probate.

The Economic Outlook and Your 401(k) for 2026

While no one has a crystal ball, understanding the general economic outlook can help inform your retirement planning decisions. For 2026, experts often project continued, albeit potentially slower, economic growth, along with ongoing inflation management by central banks. Interest rates might stabilize or even see slight adjustments, impacting bond markets and the cost of borrowing.

These macroeconomic factors can influence investment returns and the purchasing power of your retirement savings. However, the core principles of long-term investing remain constant: consistent contributions, diversification, and a disciplined approach. Don’t let short-term economic forecasts derail your long-term strategy to maximize 401k 2026 and beyond. Instead, use them as a backdrop for reviewing your plan, not for making impulsive changes.

For instance, if inflation remains elevated, the importance of growth-oriented investments (like equities) that can outpace inflation becomes even more critical. Conversely, if economic slowdowns are anticipated, a well-diversified portfolio with some allocation to more stable assets can provide a buffer. The key is to remain adaptable and informed, rather than reactive.

Conclusion: Your Path to a Secure Retirement in 2026 and Beyond

The journey to a secure and comfortable retirement is a marathon, not a sprint. By proactively planning and consistently executing strategies to maximize 401k 2026 contributions, you are laying a strong foundation for your financial future. This involves not only hitting the maximum contribution limits, especially if you’re eligible for catch-up contributions, but also leveraging employer matches and making smart investment choices within your plan.

Remember to consider the benefits of Roth options, explore advanced strategies like the Mega Backdoor Roth if applicable, and complement your 401(k) with other powerful savings vehicles like IRAs and HSAs. Regular review of your plan and a willingness to adapt to changing circumstances are paramount. By avoiding common mistakes and staying informed, you can ensure your 401(k) is working as hard as possible for you, paving the way for the retirement you’ve always envisioned. Start today, stay disciplined, and watch your retirement nest egg grow.