Emergency Fund Essentials: Building Your 6-Month Safety Net by December 2026

Anúncios

Emergency Fund Essentials: Building Your 6-Month Safety Net by December 2026

In an unpredictable world, financial stability isn’t just a luxury; it’s a necessity. One of the cornerstones of a resilient financial life is a robust emergency fund. This isn’t merely about having some extra cash; it’s about creating a dedicated safety net designed to protect you from life’s inevitable curveballs. Whether it’s an unexpected job loss, a medical emergency, or a sudden home repair, an adequate emergency fund can mean the difference between a minor setback and a full-blown financial crisis.

Anúncios

Our ambitious, yet entirely achievable, goal for you is to build a comprehensive 6-month emergency fund by December 2026. This isn’t just a distant dream; it’s a concrete, actionable plan that we’ll break down step by step. By the end of this guide, you’ll have a clear roadmap, practical strategies, and the motivation to make your financial security a reality. Let’s delve into the emergency fund essentials you need to know and implement.

Anúncios

Understanding the ‘Why’: The Importance of an Emergency Fund

Before we dive into the ‘how,’ it’s crucial to solidify the ‘why.’ Why is an emergency fund so vital? Think of it as your personal financial insurance policy. While traditional insurance covers specific events like car accidents or house fires, an emergency fund covers the financial fallout from a broader range of unexpected situations that insurance might not touch. Here are some key reasons why prioritizing your emergency fund essentials is paramount:

- Job Loss or Income Reduction: This is arguably the most common and impactful reason for needing an emergency fund. Losing a job can quickly deplete your regular income, and finding a new one can take months. An emergency fund provides the breathing room to cover your expenses without resorting to high-interest debt.

- Medical Emergencies: Even with health insurance, out-of-pocket costs, deductibles, and co-pays can quickly add up. An emergency fund ensures you can focus on recovery, not financial strain.

- Unexpected Home or Car Repairs: Your roof springs a leak, your car breaks down, or your appliance gives out. These aren’t just inconvenient; they can be expensive. An emergency fund allows you to address these issues promptly, preventing them from escalating.

- Economic Downturns: Recessions and economic instability can impact job markets and investment values. A solid emergency fund offers stability during turbulent times, reducing anxiety and preventing forced asset sales.

- Avoiding Debt: Without an emergency fund, unexpected expenses often lead to relying on credit cards, personal loans, or even dipping into retirement savings. This can trap you in a cycle of debt that’s difficult to escape.

- Peace of Mind: Perhaps the most invaluable benefit is the psychological one. Knowing you have a financial cushion provides immense peace of mind, reducing stress and allowing you to make clear-headed decisions during crises.

By understanding these compelling reasons, you’re better equipped to commit to the journey of building your emergency fund. It’s not just about money; it’s about safeguarding your future and your well-being.

Defining Your Goal: How Much Do You Really Need?

Our target is a 6-month emergency fund, but what does that actually translate to in dollars? The first step in building your emergency fund essentials is to accurately calculate your monthly expenses. This isn’t about how much you spend, but how much you need to spend to maintain your basic living standards.

Step 1: Calculate Your Essential Monthly Expenses

Gather your bank statements, credit card bills, and any other financial records from the past three to six months. Categorize your spending into two groups: essential and non-essential.

- Essential Expenses: These are the non-negotiable costs that keep a roof over your head, food on your table, and you healthy. Examples include:

- Housing (rent/mortgage, property taxes, essential utilities like electricity, water, heat)

- Groceries (basic food needs, not dining out)

- Transportation (car payments, gas, public transport, essential maintenance)

- Insurance (health, car, home)

- Minimum debt payments (student loans, credit cards – focus on minimums to avoid default)

- Childcare (if applicable and essential for work)

- Essential medications

- Non-Essential Expenses: These are things you could temporarily cut back on or eliminate during a financial crisis. Examples include:

- Dining out/takeaway

- Entertainment (streaming services, movies, concerts)

- Hobbies and recreational activities

- Subscriptions (gym memberships, non-essential apps)

- Vacations and luxury purchases

- High-end clothing

Add up only your essential monthly expenses. Let’s say, for example, your essential monthly expenses come out to $3,000.

Step 2: Determine Your Target Amount

Once you have your essential monthly expenses, multiply that by your desired coverage period. For our goal of a 6-month emergency fund:

Target Emergency Fund = Essential Monthly Expenses × 6

Using our example: $3,000/month × 6 months = $18,000.

This $18,000 is your concrete target. Having a specific number makes the goal tangible and easier to track. Remember, some financial experts recommend 3-6 months, while others suggest 9-12 months, especially for those with unstable incomes or dependents. Six months is a solid, widely recommended baseline for building your emergency fund essentials.

Crafting Your Savings Strategy: The Path to December 2026

Now that you know your target, how do you get there? This is where strategic planning and consistent action come into play. We have approximately 30 months until December 2026. This gives us a good runway to build a substantial fund.

Strategy 1: Create a Detailed Budget and Track Your Spending

You can’t save what you don’t track. A budget is your financial roadmap. It helps you understand where your money is going and identify areas where you can cut back to free up funds for your emergency savings.

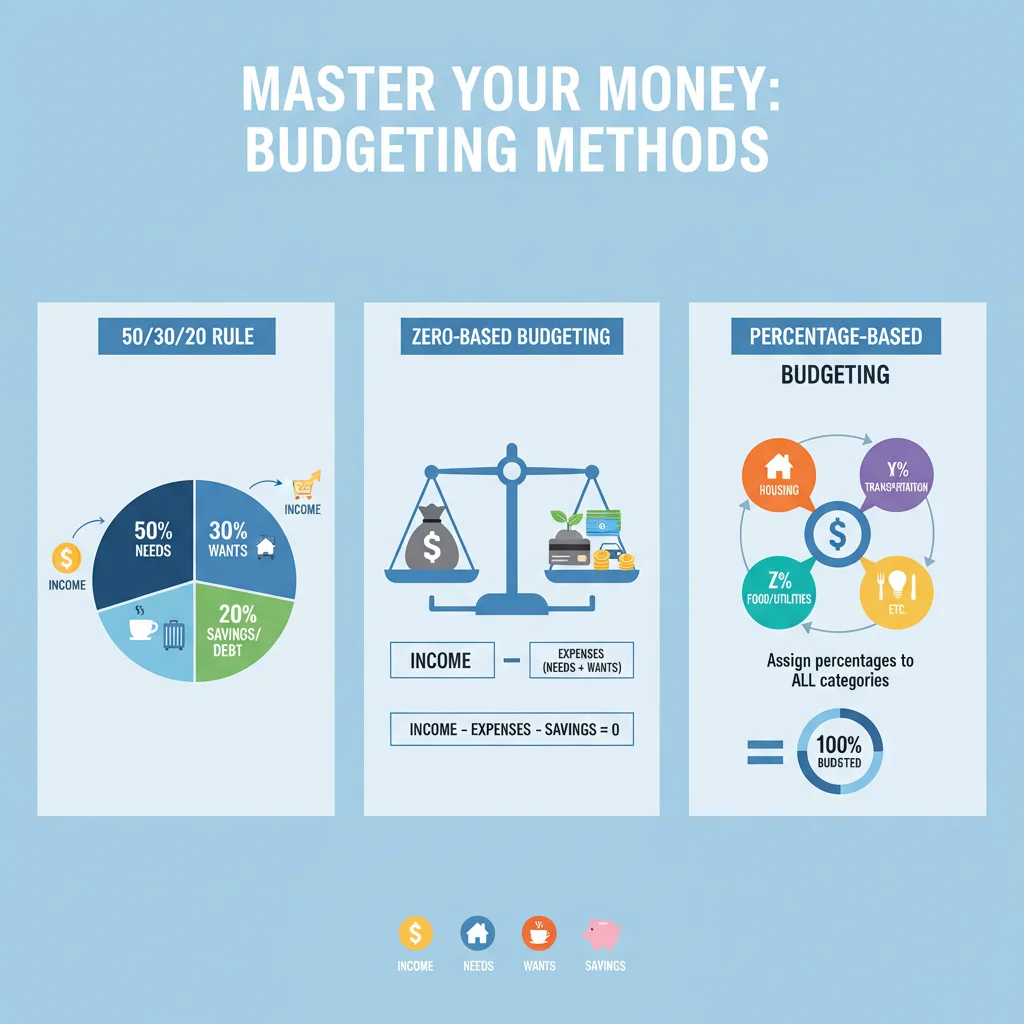

- The 50/30/20 Rule: A popular budgeting guideline where 50% of your income goes to needs, 30% to wants, and 20% to savings and debt repayment. If you’re aggressive about your emergency fund, you might aim to allocate more than 20% to savings temporarily.

- Zero-Based Budgeting: Every dollar has a job. You allocate every cent of your income to a specific category (expenses, savings, debt) until your income minus your allocations equals zero. This gives you maximum control.

- Envelope System: For cash spenders, this involves allocating physical cash into envelopes for different spending categories.

Tools like budgeting apps (Mint, YNAB, Personal Capital) or even a simple spreadsheet can be invaluable here. Regularly review your budget to ensure it aligns with your saving goals. Identifying and eliminating unnecessary expenses is a powerful way to accelerate your emergency fund growth.

Strategy 2: Automate Your Savings

The easiest way to save consistently is to make it automatic. Set up an automatic transfer from your checking account to a separate savings account specifically designated for your emergency fund. Schedule this transfer to occur on payday, before you have a chance to spend the money. Even small, consistent contributions add up significantly over time.

For example, if your target is $18,000 and you have 30 months:

$18,000 / 30 months = $600 per month.

Can you realistically save $600 a month? If not, adjust your budget, or look for ways to increase your income. The key is consistency.

Strategy 3: Boost Your Income

Sometimes, cutting expenses isn’t enough, or you’ve cut all you can. In such cases, increasing your income can significantly speed up your emergency fund progress. Consider:

- Side Hustles: Freelancing, ride-sharing, food delivery, tutoring, pet-sitting, selling crafts online – there are countless ways to earn extra money in your spare time.

- Selling Unused Items: Declutter your home and sell items you no longer need on platforms like eBay, Craigslist, Facebook Marketplace, or local consignment shops.

- Negotiating a Raise: If you’re due for one, prepare your case and ask your employer for a salary increase.

- Taking on Overtime: If available at your current job, this can be a quick way to boost earnings.

Every extra dollar earned and directed towards your emergency fund gets you closer to your December 2026 goal.

Strategy 4: Aggressively Attack Debt (Strategically)

While the primary focus is saving, high-interest debt (like credit card debt) can be a significant drain on your finances and make saving difficult. Consider a hybrid approach: save a smaller initial emergency fund (e.g., $1,000-$2,000) to cover minor immediate emergencies, then aggressively pay down high-interest debt. Once that debt is gone, redirect those freed-up funds to your main emergency fund. This strategy prevents interest payments from eating into your savings potential.

Strategy 5: Windfalls and Bonuses

Did you receive a tax refund, a work bonus, an inheritance, or a monetary gift? Resist the urge to splurge. Instead, direct a significant portion, or even all, of these windfalls directly into your emergency fund. These unexpected boosts can dramatically accelerate your progress towards your emergency fund essentials goal.

Where to Keep Your Emergency Fund: Accessibility and Growth

Once you start accumulating funds, where should you keep them? The location of your emergency fund is almost as important as the act of saving itself. The key criteria are safety, accessibility, and a modest return.

- High-Yield Savings Account (HYSA): This is generally the recommended option. HYSAs offer better interest rates than traditional savings accounts, meaning your money grows (albeit slowly) while remaining highly liquid. Look for FDIC-insured accounts to protect your deposits.

- Money Market Account: Similar to HYSAs, money market accounts often offer slightly higher interest rates and sometimes come with check-writing capabilities or a debit card, offering easy access if needed. They are also FDIC-insured.

- Certificates of Deposit (CDs) – with caution: While CDs offer higher interest rates, they lock up your money for a specified term. If you need to access your funds before the term ends, you’ll likely incur a penalty. Some people use a ‘CD ladder’ for a portion of their emergency fund, but for the core, easily accessible funds, HYSAs are preferred.

- Avoid the Stock Market: Your emergency fund should NOT be invested in stocks, mutual funds, or other volatile assets. The primary purpose of this fund is safety and accessibility, not growth. You cannot risk your emergency money being down 20-30% when you suddenly need it.

Crucially, keep your emergency fund in a separate account from your everyday checking account. This makes it less tempting to dip into for non-emergencies and helps you clearly see your progress towards your emergency fund essentials goal.

Maintaining Momentum: Overcoming Challenges and Staying Motivated

Building a significant emergency fund takes time and discipline. There will be moments when you feel discouraged or tempted to use the money for something else. Here’s how to stay on track:

- Set Mini-Goals: Instead of just focusing on the final $18,000, celebrate reaching $1,000, then $3,000, then one month’s expenses. Small victories keep you motivated.

- Track Your Progress Visually: Use a spreadsheet, an app, or even a physical chart to see how far you’ve come. Visual progress can be incredibly encouraging.

- Remind Yourself of the ‘Why’: Regularly revisit the reasons you started this journey. Picture the peace of mind you’ll have knowing you’re financially secure.

- Be Flexible, Not Defeated: If an actual emergency arises and you need to use a portion of your fund, don’t view it as a failure. That’s exactly what it’s there for! Immediately create a plan to replenish it.

- Educate Yourself: Continuously learn about personal finance. The more you understand, the more empowered you’ll feel about your financial decisions.

- Find an Accountability Partner: Share your goal with a trusted friend or family member. They can offer encouragement and help keep you accountable.

Common Pitfalls to Avoid When Building Your Emergency Fund

While the path to building your emergency fund essentials is clear, there are common mistakes that can derail your efforts. Being aware of these can help you navigate around them:

- Not Having a Separate Account: Keeping your emergency money in your checking account makes it too easy to accidentally spend. A separate, dedicated account is crucial.

- Underestimating Expenses: Be realistic when calculating your essential monthly expenses. Skimping on this calculation will lead to an insufficient fund.

- Starting Too Small (or Not Starting at All): Don’t let the large goal intimidate you. Even saving $25 a week is a start. The most important step is the first one.

- Using the Fund for Non-Emergencies: That new gadget or vacation might feel urgent, but it’s not an emergency. Stick to your definition of an emergency.

- Ignoring Inflation: While not a primary concern for short-term savings, over very long periods, the purchasing power of your emergency fund can erode. Review your fund periodically to ensure it still covers your current essential expenses.

- Not Replenishing the Fund: If you use your emergency fund, make replenishing it your top financial priority immediately afterward.

- Being Impatient: Building a 6-month emergency fund takes time and consistent effort. Celebrate small wins and stay focused on the long-term goal of December 2026.

Advanced Strategies: Beyond the 6-Month Mark

Once you’ve successfully reached your 6-month emergency fund goal by December 2026, congratulations! That’s a massive achievement. But the journey doesn’t necessarily end there. Depending on your personal circumstances, you might consider:

- Expanding Your Fund: For those with highly unstable incomes (e.g., commission-based jobs, freelancers, small business owners) or multiple dependents, extending your fund to 9 or even 12 months of expenses can provide an even greater buffer.

- Optimizing for Interest: While safety and accessibility are paramount, once you have a substantial fund, you might explore slightly more sophisticated ways to earn a bit more interest, always ensuring liquidity. However, this should only be considered after your core fund is robust and secure.

- Addressing Other Financial Goals: With your emergency fund firmly in place, you can confidently redirect your aggressive saving habits towards other crucial financial goals, such as retirement planning, a down payment on a home, or funding a child’s education. The discipline you’ve built creating your emergency fund will serve you well in these endeavors.

Conclusion: Your Path to Financial Resilience by December 2026

Building a 6-month emergency fund by December 2026 is a significant, yet entirely achievable, financial milestone. It requires discipline, strategic planning, and consistent effort, but the peace of mind and security it provides are invaluable. By understanding the emergency fund essentials – calculating your needs, creating a robust savings strategy, choosing the right place for your money, and staying motivated – you are well on your way to achieving financial resilience.

Start today. Take that first step, whether it’s calculating your essential expenses, setting up an automatic transfer, or finding a side hustle. Every action, no matter how small, moves you closer to your goal. Imagine approaching December 2026 with the confidence that comes from a fully funded emergency safety net. That future is within your reach. Commit to it, and watch your financial security grow.