Small Business Loans 2026: Funding for Women-Owned Businesses

Anúncios

The entrepreneurial spirit is alive and thriving, particularly among women. As we look towards 2026, the landscape for small business loans is evolving, presenting unprecedented opportunities for women-owned businesses. Projections indicate a remarkable 15% higher approval rate for these enterprises, a testament to their growing economic impact and the targeted efforts by financial institutions and government programs to foster their success. This comprehensive guide will navigate the intricacies of securing funding in this dynamic environment, offering insights, strategies, and a roadmap to empower your business growth.

For too long, women entrepreneurs have faced unique challenges in accessing capital, often encountering biases and systemic barriers that hindered their ability to scale. However, a significant shift is underway. Recognition of the immense potential within the women-owned business sector is driving innovation in lending practices, creating a more inclusive and supportive ecosystem. This article delves into what this shift means for you, how to prepare, and where to find the best small business loans to fuel your ambitions.

Anúncios

Understanding the Evolving Landscape of Small Business Loans in 2026

The year 2026 promises a more favorable climate for small businesses seeking financing, with a particular emphasis on supporting diversity and inclusion. This isn’t merely a trend; it’s a strategic economic imperative. Governments, traditional banks, and alternative lenders are increasingly recognizing that investing in women-owned businesses translates into robust economic growth, job creation, and innovation. This understanding is translating into more accessible and tailored small business loans products.

Anúncios

Key Drivers of Change

- Increased Awareness and Advocacy: Greater public and private sector awareness of the historical funding gap for women entrepreneurs has led to more advocacy and policy changes designed to level the playing field.

- Data-Driven Lending: Advancements in data analytics and artificial intelligence are allowing lenders to assess creditworthiness more holistically, moving beyond traditional metrics that may have disproportionately impacted women. This leads to more equitable evaluations for small business loans.

- Targeted Programs and Initiatives: A proliferation of programs specifically designed to support women-owned businesses, including grants, mentorship, and specialized loan products, is making a significant difference.

- Growth in Fintech and Alternative Lending: The rise of financial technology (Fintech) platforms has diversified the lending market, offering more flexible and accessible options for entrepreneurs who might not fit traditional banking criteria. These platforms are often more agile in adapting to the specific needs of niche markets, including women-owned businesses seeking small business loans.

- Economic Impact Recognition: Studies consistently show that women-owned businesses contribute significantly to GDP and job creation. This tangible impact reinforces the business case for increased investment and support through accessible small business loans.

This confluence of factors is creating a fertile ground for women entrepreneurs. The projected 15% higher approval rate for small business loans is not an arbitrary number; it reflects a systemic shift towards recognizing and empowering this vital segment of the economy.

Why the 15% Higher Approval Rate for Women-Owned Businesses?

The statistic of a 15% higher approval rate for women-owned businesses seeking small business loans in 2026 is a powerful indicator of progress. But what specifically underpins this positive trend? Several factors contribute to this encouraging development:

Stronger Business Acumen and Preparedness

Research suggests that women entrepreneurs often exhibit meticulous planning and a robust understanding of their business models. They tend to be more thorough in their loan applications, presenting comprehensive business plans, detailed financial projections, and clear strategies for repayment. This level of preparedness instills confidence in lenders, making their applications for small business loans more compelling.

Higher Repayment Rates

Historically, women have demonstrated excellent repayment behavior on loans. This track record of reliability makes them less risky borrowers in the eyes of financial institutions. As lenders increasingly leverage data to inform their decisions, this positive repayment history translates into more favorable lending terms and higher approval rates for small business loans.

Focus on Sustainable Growth

Many women-owned businesses prioritize sustainable growth and ethical practices, which can lead to more stable and resilient enterprises. Lenders are increasingly looking beyond rapid expansion and valuing businesses with strong foundations and long-term viability, making these businesses ideal candidates for small business loans.

Dedicated Support Ecosystems

The growth of organizations, accelerators, and mentorship programs specifically catering to women entrepreneurs has equipped them with the skills, networks, and resources needed to succeed. This enhanced support system not only helps women start and grow businesses but also prepares them to navigate the complexities of securing small business loans effectively.

Policy and Legislative Support

Government initiatives and policies aimed at promoting women’s entrepreneurship are also playing a crucial role. These include set-asides for government contracts, tax incentives, and direct funding programs that indirectly improve the overall funding landscape for women-owned businesses seeking small business loans.

This confluence of factors creates a virtuous cycle: as women-owned businesses prove their creditworthiness and economic impact, more resources and opportunities become available, further bolstering their success in securing small business loans.

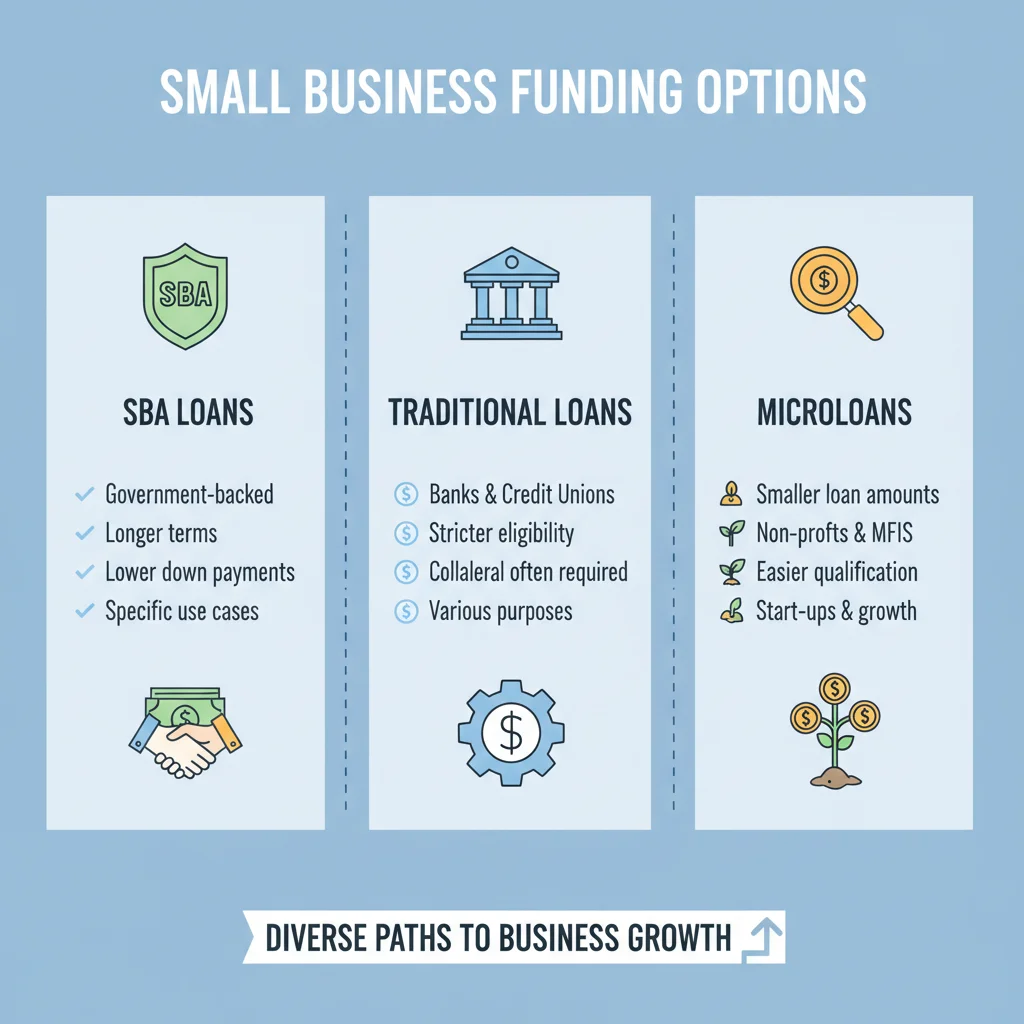

Types of Small Business Loans Available in 2026

The array of small business loans available in 2026 is diverse, catering to various stages of business development and specific financial needs. Understanding these options is the first step towards securing the right funding for your venture.

1. SBA Loans (Small Business Administration)

SBA loans remain a cornerstone of small business financing. While the SBA doesn’t lend money directly (except in specific disaster situations), it guarantees a portion of loans made by approved lenders. This guarantee reduces the risk for lenders, making them more willing to provide capital to small businesses, especially those that might not qualify for conventional loans. For women-owned businesses, SBA loans are particularly attractive due to their favorable terms, lower interest rates, and longer repayment periods.

Popular SBA Loan Programs:

- SBA 7(a) Loan Program: The most common and flexible SBA loan, suitable for a wide range of business purposes including working capital, equipment purchases, real estate, and refinancing debt.

- SBA 504 Loan Program: Designed for major fixed-asset purchases, such as real estate or machinery. It typically involves a partnership between a small business, a bank, and a Certified Development Company (CDC).

- SBA Microloan Program: Provides smaller loans (up to $50,000) for working capital or to purchase inventory, supplies, furniture, fixtures, or equipment. This program often works with intermediary lenders who also provide business training and technical assistance, which can be invaluable for women entrepreneurs.

2. Traditional Bank Loans

Conventional term loans and lines of credit from traditional banks are still a viable option for established businesses with strong credit histories and collateral. While they can be more challenging to secure for startups or businesses with limited operating history, their competitive interest rates and structured repayment plans make them desirable. Banks are increasingly offering specialized products and dedicated support for women entrepreneurs, recognizing the growth potential in this market.

3. Alternative Lenders and Fintech Platforms

The rise of online lenders and Fintech platforms has revolutionized the small business lending landscape. These platforms often offer quicker application processes, faster funding times, and more flexible eligibility criteria compared to traditional banks. They can be an excellent option for businesses needing rapid access to capital or those who may not meet strict bank requirements. Examples include online term loans, merchant cash advances, invoice factoring, and equipment financing. Many of these platforms are also actively seeking to support diverse entrepreneurs, including women-owned businesses.

4. Microloans and Community Development Financial Institutions (CDFIs)

CDFIs are mission-driven financial institutions that provide financial services to underserved communities and populations, including women entrepreneurs. They often offer microloans, technical assistance, and business counseling, making them a crucial resource for startups and very small businesses. Their focus on community development aligns well with the social impact often driven by women-owned enterprises.

5. Grants for Women-Owned Businesses

While not technically small business loans, grants are non-repayable funds that can provide significant capital. Numerous organizations, foundations, and government agencies offer grants specifically for women-owned businesses across various industries. While competitive, grants can be a fantastic way to secure funding without incurring debt. It’s crucial to research and apply for grants that align with your business’s mission and industry.

Choosing the right type of small business loans depends on your business’s stage, financial health, and specific needs. A thorough understanding of each option will empower you to make an informed decision.

Preparing Your Business for a Small Business Loan Application

Securing a small business loan, particularly with the enhanced opportunities in 2026, requires meticulous preparation. Lenders look for stability, growth potential, and a clear understanding of financial health. Here’s how to position your women-owned business for success:

1. Develop a Comprehensive Business Plan

A well-articulated business plan is your roadmap and a critical document for any lender. It should clearly outline your business’s mission, vision, products or services, market analysis, marketing and sales strategy, operational plan, and management team. For women-owned businesses, highlighting unique market insights or community impact can be an added advantage. A robust plan demonstrates your foresight and commitment to your venture, making your request for small business loans more compelling.

2. Maintain Impeccable Financial Records

Lenders need to see a clear picture of your financial health. This includes up-to-date:

- Financial Statements: Profit and loss statements, balance sheets, and cash flow statements for at least the past three years (if applicable).

- Tax Returns: Personal and business tax returns for the past two to three years.

- Bank Statements: Recent business bank statements to show cash flow and liquidity.

- Debt Schedule: A list of all outstanding business debts, including terms and payment history.

Accurate and organized financial records not only demonstrate fiscal responsibility but also allow lenders to assess your repayment capacity for small business loans.

3. Understand Your Credit Score (Personal and Business)

Both your personal and business credit scores will be scrutinized. A strong personal credit score (typically 680+) is often a prerequisite, especially for newer businesses. Establish business credit early by acquiring a DUNS number, separating business and personal finances, and ensuring timely payments to suppliers and vendors. A healthy credit profile significantly increases your chances of approval for small business loans.

4. Determine Your Funding Needs and Use of Funds

Clearly define how much money you need and exactly how you plan to use it. Vague requests are red flags for lenders. Whether it’s for purchasing equipment, expanding operations, hiring staff, or increasing inventory, provide a detailed breakdown. This demonstrates financial planning and shows that the small business loan will be used strategically to generate returns.

5. Prepare Collateral (If Applicable)

Some small business loans, particularly traditional bank loans and larger SBA loans, may require collateral. This could include real estate, equipment, accounts receivable, or inventory. Be prepared to discuss what assets you can offer to secure the loan. While not all loans require collateral, having it available can strengthen your application.

6. Craft a Compelling Loan Proposal

Beyond the standard documents, a well-written loan proposal can differentiate your application. This document should summarize your business, highlight its unique selling propositions, explain your funding request, and project future growth. Emphasize the experience and expertise of your management team, especially if it’s a woman-led team, and how you plan to leverage the small business loan for success.

Strategies for Women-Owned Businesses to Maximize Approval Rates

Leveraging the projected 15% higher approval rate for small business loans in 2026 requires more than just meeting basic requirements. Proactive strategies can significantly enhance your chances of securing the capital your business needs.

1. Seek Certifications and Designations

Obtaining certifications such as Women-Owned Small Business (WOSB) or Economically Disadvantaged Women-Owned Small Business (EDWOSB) can open doors to specific government contracts and preferential lending programs. These certifications validate your business’s status and often come with access to resources and networks that can aid in securing small business loans.

2. Network with Women-Focused Financial Institutions and Organizations

Many financial institutions and non-profit organizations specialize in supporting women entrepreneurs. These entities are often more attuned to the unique challenges and opportunities faced by women-owned businesses and may offer tailored small business loans products, mentorship, and financial literacy programs. Engaging with these networks can provide invaluable support and connections.

3. Leverage Mentorship and Business Advising

Connecting with experienced mentors or business advisors, especially those who have successfully navigated the funding landscape, can provide crucial insights. They can help you refine your business plan, strengthen your financial projections, and prepare for lender interviews, significantly increasing your confidence and readiness for applying for small business loans.

4. Focus on a Strong Online Presence

In today’s digital age, lenders often research businesses online. A professional website, active social media presence, and positive customer reviews can build credibility and demonstrate market traction. This digital footprint can indirectly support your loan application by showcasing your business’s legitimacy and appeal.

5. Clearly Articulate Your Business’s Social Impact

Many women-owned businesses are deeply committed to social responsibility and community impact. Highlighting these aspects in your loan application can resonate with lenders who prioritize ESG (Environmental, Social, Governance) factors. This can differentiate your business and potentially open doors to impact investments or socially responsible small business loans.

6. Practice Your Pitch

Be prepared to articulate your business idea, financial needs, and growth strategy concisely and confidently. Practice explaining your business plan and answering potential questions from lenders. A clear, compelling pitch can leave a lasting positive impression and reinforce your capability to manage the small business loan effectively.

Common Pitfalls to Avoid When Applying for Small Business Loans

While the outlook for women-owned businesses seeking small business loans is bright, it’s essential to be aware of common mistakes that can derail your application. Avoiding these pitfalls will streamline the process and increase your chances of success.

1. Inadequate Preparation

As mentioned, preparation is key. Rushing the application process, submitting incomplete documentation, or providing inaccurate financial figures are surefire ways to get rejected. Take the time to gather all necessary documents, verify information, and ensure your business plan is robust and well-supported. Lenders prioritize thoroughness and attention to detail when evaluating applications for small business loans.

2. Unrealistic Financial Projections

While optimism is good, lenders prefer realistic and conservative financial projections. Overly ambitious revenue forecasts or underestimating expenses can signal a lack of financial acumen. Base your projections on market research, historical data (if available), and industry benchmarks. Be prepared to justify every figure in your financial statements for small business loans.

3. Poor Personal Credit History

Even if your business is thriving, a poor personal credit score can significantly impact your eligibility for small business loans, especially for newer ventures. Lenders often view personal credit as an indicator of an entrepreneur’s financial responsibility. If your personal credit is weak, take steps to improve it before applying, or explore options that rely less on personal credit, such as some alternative lenders.

4. Mixing Personal and Business Finances

Failing to separate personal and business finances is a common mistake for small business owners. This practice makes it difficult to track business expenses, revenues, and profitability accurately, which is crucial for a loan application. Open a dedicated business bank account and credit cards, and maintain separate records. This demonstrates professionalism and makes your financial statements clearer for lenders evaluating small business loans.

5. Not Understanding Loan Terms and Conditions

Before signing any agreement, thoroughly understand the interest rates, repayment schedule, fees, collateral requirements, and any covenants associated with the small business loan. Don’t be afraid to ask questions. Being fully informed ensures you choose a loan that aligns with your business’s financial capacity and avoids unexpected surprises down the line.

6. Applying for the Wrong Type of Loan

As discussed, there are various types of small business loans. Applying for a loan that doesn’t fit your business’s needs or stage can lead to rejection and wasted time. For example, a startup needing working capital might struggle to get a traditional term loan designed for established businesses buying real estate. Research and match the loan product to your specific use case.

7. Lack of a Clear Use for Funds

Lenders want to know precisely how their money will be used and how it will contribute to your business’s growth and ability to repay the loan. A vague statement like ‘for general business operations’ is insufficient. Provide a detailed breakdown of how the small business loan funds will be allocated and the expected return on investment.

By proactively addressing these potential issues, women entrepreneurs can significantly strengthen their applications and take full advantage of the favorable lending environment for small business loans in 2026.

The Future is Bright: Empowering Women in Business

The projected 15% higher approval rate for women-owned businesses seeking small business loans in 2026 is not just a statistic; it represents a significant step forward in economic equality and empowerment. It signifies a growing recognition of the talent, resilience, and innovative spirit that women entrepreneurs bring to the global economy.

This positive trend is a call to action for all aspiring and existing women business owners. The resources, support, and capital are becoming more accessible than ever before. By understanding the landscape, preparing diligently, and leveraging available opportunities, you can secure the funding necessary to grow your business, create jobs, and contribute to a more vibrant and diverse economic future.

As you plan for 2026 and beyond, remember that securing small business loans is a journey. It requires research, persistence, and a clear vision. Embrace the support systems available, learn from every experience, and continue to build a strong foundation for your business. The future for women-owned businesses is not just promising; it’s being actively shaped by the collective efforts of entrepreneurs, financial institutions, and supportive communities worldwide. Your success is integral to this progress.

Take advantage of this evolving landscape. Research specific programs for women entrepreneurs, connect with financial advisors, and meticulously prepare your application. The path to securing the right small business loans for your venture is clearer than ever, paving the way for unprecedented growth and impact.