Student Loan Forgiveness 2026: PSLF Guide & Updates

Anúncios

Student Loan Forgiveness Programs in 2026: A Step-by-Step Guide to Public Service Loan Forgiveness (Practical Solutions, Recent Updates)

The landscape of student loan debt in the United States is vast and often complex, impacting millions of Americans. As we look ahead to 2026, the discussion around student loan forgiveness remains a critical topic for borrowers seeking relief. While broad, sweeping forgiveness initiatives have seen their share of political and legal challenges, targeted programs like the Public Service Loan Forgiveness (PSLF) continue to offer a beacon of hope for many. Understanding the intricacies of these programs, especially PSLF, is paramount for anyone aiming to reduce their student debt burden.

Anúncios

This comprehensive guide will delve into the current state of student loan forgiveness, with a particular focus on the Public Service Loan Forgiveness program as it stands in 2026. We will explore recent updates, eligibility criteria, the application process, and practical strategies to ensure you are on the right track towards achieving forgiveness. Whether you are just beginning your public service career or are nearing your 120 qualifying payments, this article aims to provide clarity and actionable advice.

Anúncios

Understanding the Current Landscape of Student Loan Forgiveness 2026

The concept of student loan forgiveness has evolved significantly over the past few years. While the Biden administration attempted a large-scale forgiveness plan, it faced legal hurdles and was ultimately blocked by the Supreme Court. This outcome underscored the importance of existing, established programs like PSLF, which operate under specific statutory guidelines. For borrowers looking for student loan forgiveness 2026, it’s crucial to differentiate between potential future legislative actions and the reliable pathways currently available.

In 2026, the primary avenue for significant federal student loan forgiveness for many will continue to be programs tied to specific employment or circumstances. Beyond PSLF, other programs exist for teachers, doctors in underserved areas, and individuals with total and permanent disability. However, for a broad segment of the population engaged in public service, PSLF remains the most impactful and widely accessible option. The focus on student loan forgiveness 2026, therefore, largely revolves around optimizing participation in these established frameworks.

Recent updates from the Department of Education have aimed at simplifying and expanding access to PSLF, particularly through temporary waivers and adjustments that have addressed past administrative complexities. While some of these temporary measures may have concluded by 2026, their impact on improving the program’s efficiency and transparency is likely to be long-lasting. Staying informed about these changes and understanding how they might still affect your eligibility or payment count is vital.

Public Service Loan Forgiveness (PSLF): The Cornerstone of Student Loan Forgiveness 2026

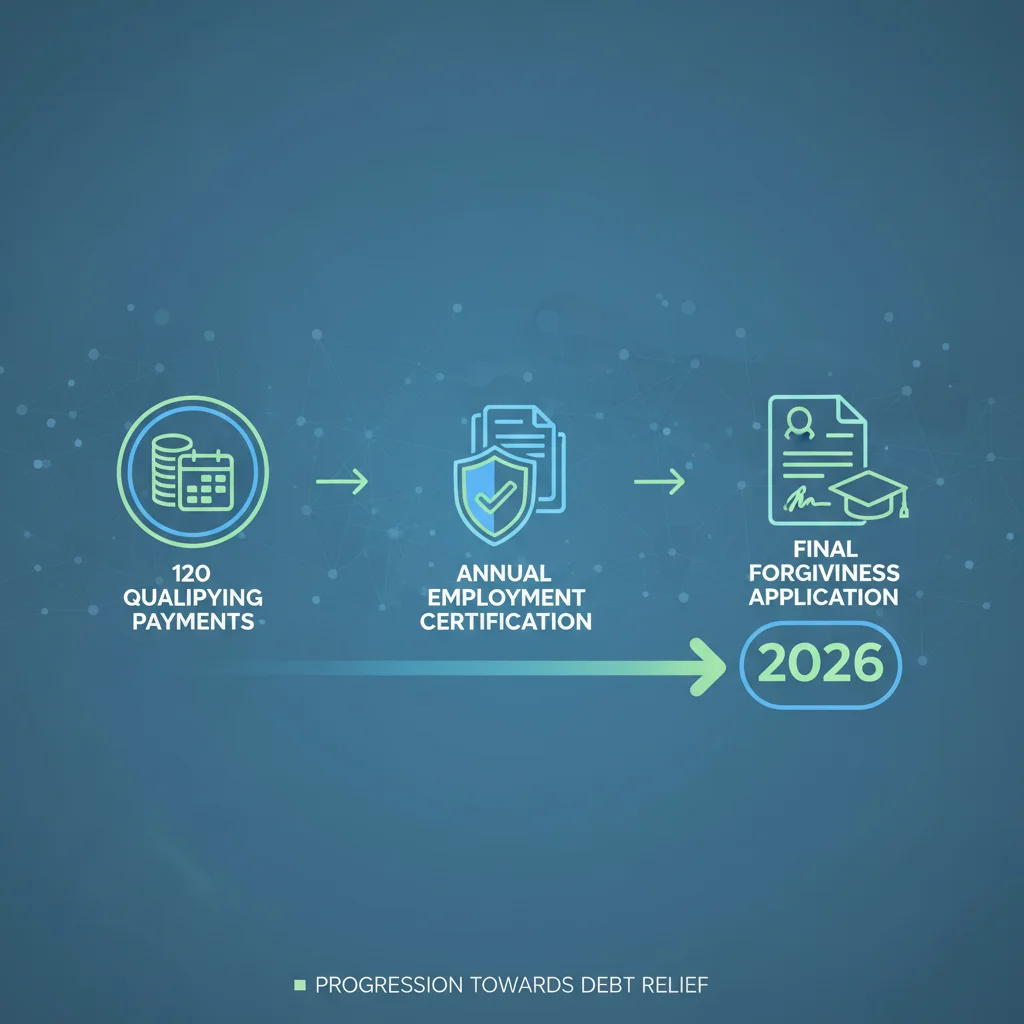

The Public Service Loan Forgiveness (PSLF) program is designed to encourage individuals to enter and remain in full-time public service employment. It offers forgiveness of the remaining balance on Direct Loans after 120 qualifying monthly payments have been made under a qualifying repayment plan while working full-time for a qualifying employer. This program is particularly relevant for those seeking student loan forgiveness 2026, as many borrowers will be reaching or surpassing their 10-year mark of public service by this time.

Who Qualifies for PSLF? Eligibility Criteria

To be eligible for PSLF, you must meet several key criteria:

- Eligible Loans: Only federal Direct Loans qualify for PSLF. If you have Federal Family Education Loan (FFEL) Program loans or Federal Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to be eligible. It’s important to do this sooner rather than later, as only payments made after consolidation will count towards the 120.

- Qualifying Employment: You must be employed full-time by a U.S. federal, state, local, or tribal government agency (including military service) or a not-for-profit organization that is tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Other non-profit organizations that provide certain public services may also qualify. Full-time generally means working at least 30 hours per week.

- Qualifying Payments: You must make 120 qualifying monthly payments. These payments must be made:

- After October 1, 2007.

- Under a qualifying repayment plan (typically an income-driven repayment plan).

- For the full amount due as shown on your bill.

- Within 15 days of your due date.

- While you are employed full-time by a qualifying employer.

- Repayment Plan: You must be enrolled in an income-driven repayment (IDR) plan (e.g., REPAYE, PAYE, IBR, ICR). Payments made under the Standard Repayment Plan also count, but only if you consolidate your loans and the standard plan is for a 10-year term, which would result in your loans being paid off before forgiveness could occur. Therefore, IDR plans are almost always necessary to have a remaining balance to forgive.

Understanding these criteria is the first step towards securing student loan forgiveness 2026 through PSLF. Any deviation from these requirements can jeopardize your eligibility.

The PSLF Application Process: A Step-by-Step Guide for 2026

The application process for PSLF has historically been a point of confusion for many borrowers. However, the Department of Education has made efforts to streamline it. Here’s a general guide for applying for student loan forgiveness 2026 through PSLF:

Step 1: Consolidate Your Loans (If Necessary)

As mentioned, only Direct Loans qualify. If you have FFEL or Perkins Loans, you must consolidate them into a Direct Consolidation Loan. This process can take several weeks, so do not delay. Remember, payments made on non-Direct Loans before consolidation will not count towards PSLF.

Step 2: Enroll in an Income-Driven Repayment (IDR) Plan

If you are not already, enroll in an IDR plan. These plans adjust your monthly payment based on your income and family size, ensuring that your payments are affordable and that you will likely have a remaining balance to forgive after 120 payments. The Department of Education offers a tool to help you choose the best IDR plan for your situation.

Step 3: Submit the PSLF & Temporary Expanded PSLF (TEPSLF) Certification & Application (ECF) Form Annually

This is perhaps the most critical step for tracking your progress towards student loan forgiveness 2026. You should submit the PSLF Employment Certification Form (ECF) annually, or whenever you change employers. This form serves two main purposes:

- It verifies that your employer qualifies for PSLF.

- It allows the Department of Education to track your qualifying payments.

Submitting this form regularly helps identify and correct any issues early on, preventing potential headaches down the line. The form is available on the Federal Student Aid website. Your employer will need to complete and sign a section of the form to certify your employment.

Step 4: Monitor Your Payment Count

After submitting your ECF, your loan servicer (which will likely be MOHELA for PSLF-eligible loans) will review your employment and payment history and update your qualifying payment count. It is your responsibility to regularly check your count and ensure it is accurate. If you believe there are discrepancies, contact your loan servicer immediately to investigate. This proactive approach is essential for successful student loan forgiveness 2026.

Step 5: Apply for Forgiveness After 120 Qualifying Payments

Once you have made 120 qualifying payments (which equates to 10 years of payments), you will submit the final PSLF & TEPSLF Certification & Application form. This time, you will check the box indicating you are applying for forgiveness. The Department of Education will then review your entire history of employment and payments. If everything aligns, your remaining federal Direct Loan balance will be forgiven, tax-free.

Recent Updates and What They Mean for Student Loan Forgiveness 2026

The student loan landscape is dynamic, with policies and programs subject to change. While specific temporary waivers like the PSLF Waiver (which ended in October 2022) and the IDR Account Adjustment (expected to be completed in 2024) may not be active in 2026, their effects will still be felt. These initiatives retroactively credited borrowers for payments that previously didn’t count, bringing many closer to forgiveness. If you benefited from these, ensure your payment counts accurately reflect these adjustments as you plan for student loan forgiveness 2026.

The SAVE Plan and its Impact

The new Saving on a Valuable Education (SAVE) Plan, which fully rolled out in 2024, is an income-driven repayment plan that offers significant benefits, particularly for PSLF-eligible borrowers. Key features of the SAVE plan include:

- Lower Monthly Payments: For undergraduate loans, payments are reduced from 10% to 5% of discretionary income.

- Interest Subsidy: If your monthly payment doesn’t cover the accrued interest, the government covers the remaining interest, preventing your loan balance from growing. This is a game-changer for many borrowers.

- Shorter Forgiveness Timelines: While PSLF still requires 120 payments, the SAVE plan offers forgiveness for balances as low as $12,000 after 10 years of payments, even for non-PSLF borrowers. For PSLF, the interest subsidy makes it an even more attractive IDR option.

The SAVE plan is now considered the most beneficial IDR plan for most borrowers, especially those pursuing PSLF. Enrolling in SAVE could make your monthly payments more manageable and ensure you continue to make qualifying payments towards student loan forgiveness 2026 without your balance ballooning due to unpaid interest.

Potential for Future Legislative Changes

While this guide focuses on existing pathways, it’s important to acknowledge that legislative efforts for broader student loan relief may continue. However, relying on hypothetical future legislation for student loan forgiveness 2026 is a risky strategy. It is always best to actively pursue the programs currently available and ensure you meet their requirements. Stay informed through official government sources like the Department of Education and Federal Student Aid websites.

Practical Solutions and Tips for Maximizing Your PSLF Benefits Towards Student Loan Forgiveness 2026

Navigating the PSLF program requires diligence and attention to detail. Here are practical tips to help you maximize your chances of achieving student loan forgiveness 2026:

1. Keep Meticulous Records

Maintain a detailed personal file of all your student loan documents, including:

- Copies of all PSLF Employment Certification Forms (ECFs) submitted.

- Confirmation emails or letters from your loan servicer.

- Records of your employment dates and employers.

- Proof of payments made.

This documentation will be invaluable if there are any discrepancies in your payment count or employment history. Digital copies, backed up in multiple locations, are highly recommended.

2. Certify Employment Annually (or More Often)

Don’t wait until you think you’re close to 120 payments. Submitting your ECF annually, or even whenever you switch jobs, ensures your progress is regularly tracked and verified. This proactive approach helps catch and resolve any issues with your qualifying employment or payments early on, making the path to student loan forgiveness 2026 smoother.

3. Understand Your Loan Servicer’s Role

MOHELA is currently the exclusive servicer for borrowers pursuing PSLF. Familiarize yourself with their online portal, understand how they track your payments, and know how to contact them for assistance. While the Department of Education sets the rules, your servicer is the primary point of contact for day-to-day management of your loans and PSLF tracking.

4. Re-certify Your Income-Driven Repayment Plan Annually

Your IDR plan requires annual re-certification of your income and family size. Failing to do so can result in your payments reverting to the higher Standard Repayment Plan, which might not count towards PSLF or could significantly increase your monthly burden. Stay on top of these deadlines to ensure continuous qualifying payments for student loan forgiveness 2026.

5. Consult with a Student Loan Expert (If Needed)

If your situation is particularly complex, or if you encounter persistent issues with your PSLF application or payment count, consider consulting with a non-profit student loan counselor or an attorney specializing in student loan law. They can provide personalized advice and advocacy. Be wary of companies that charge exorbitant fees for services you can get for free from the Department of Education or your loan servicer.

6. Stay Informed About Policy Changes

The rules governing student loan forgiveness can change. Regularly check official sources like StudentAid.gov for the latest updates. Subscribing to email newsletters from the Department of Education can also keep you informed about any new announcements or policy shifts that could impact your journey towards student loan forgiveness 2026.

Beyond PSLF: Other Forgiveness Options in 2026

While PSLF is a major focus for student loan forgiveness 2026, it’s worth briefly mentioning other federal forgiveness programs that might apply to specific situations:

Teacher Loan Forgiveness (TLF)

This program offers up to $17,500 in forgiveness for eligible federal student loans for teachers who work full-time for five consecutive academic years in low-income schools or educational service agencies. The type of teaching (e.g., highly qualified in a high-need subject) affects the forgiveness amount.

Total and Permanent Disability (TPD) Discharge

Borrowers who are totally and permanently disabled may be eligible to have their federal student loans discharged. This can be based on a U.S. Department of Veterans Affairs (VA) disability determination, a Social Security Administration (SSA) disability determination, or a physician’s certification.

Borrower Defense to Repayment

This provides a path to forgiveness for borrowers who were defrauded by their college. If your school engaged in misconduct or violated certain state laws, you may be eligible to have your federal loans discharged.

Closed School Discharge

If your school closes while you are enrolled or soon after you withdraw, you might be eligible for a discharge of your federal student loans. This is typically for students who could not complete their program due to the closure.

Death Discharge

Federal student loans are discharged upon the death of the borrower. A family member or representative must provide proof of death to the loan servicer.

It’s important to research each of these programs thoroughly to determine if you meet the specific eligibility requirements. While they provide crucial relief, their scope is generally narrower than PSLF.

The Future of Student Loan Forgiveness Beyond 2026

Predicting the exact future of student loan forgiveness is challenging due to political and economic factors. However, the ongoing discussion highlights the persistent need for solutions to student debt. As 2026 approaches and passes, it’s reasonable to expect continued debate and potential adjustments to existing programs, or even the introduction of new initiatives. The rising cost of higher education and its impact on individuals and the economy ensures that student loan policy will remain a prominent issue.

For current and future borrowers, the best strategy remains to be proactive. Understand your loans, explore all available repayment and forgiveness options, and diligently follow the requirements of any program you pursue. This approach provides the most stable path toward managing and ultimately reducing your student debt, regardless of broader policy shifts.

Conclusion: Your Path to Student Loan Forgiveness 2026

For millions of public servants, the Public Service Loan Forgiveness program offers a tangible and significant pathway to debt relief. As we move towards student loan forgiveness 2026, understanding the nuances of PSLF, staying informed about recent policy updates like the SAVE plan, and meticulously tracking your progress are essential steps.

The journey to loan forgiveness can be long and requires sustained effort, but the reward of having your student debt erased is invaluable. By following the step-by-step guide outlined above, certifying your employment regularly, and remaining proactive in managing your loans, you can confidently navigate the path to student loan forgiveness 2026 and beyond. Your dedication to public service is commendable, and the PSLF program is designed to acknowledge and reward that commitment by helping you achieve financial freedom.