Maximizing 529 Plan Tax Benefits: A 2026 State-by-State Comparison for Educational Savings

Anúncios

Planning for college expenses is a significant undertaking for families across the United States. With the ever-increasing cost of higher education, finding effective ways to save and grow funds is paramount. Enter the 529 plan, a tax-advantaged savings plan designed to encourage saving for future education costs. While these plans offer federal tax benefits, including tax-free growth and withdrawals for qualified education expenses, the true financial leverage often comes from understanding and utilizing the 529 plan tax benefits offered at the state level. As we look towards 2026, a comprehensive state-by-state comparison becomes indispensable for maximizing these advantages.

Anúncios

The landscape of 529 plans is dynamic, with states frequently adjusting their programs to attract residents and enhance educational opportunities. This article delves deep into the nuances of 529 plan tax benefits for 2026, providing a detailed analysis to help you make informed decisions. We’ll explore various types of state-specific incentives, examine which states offer the most generous benefits, and discuss strategies to optimize your educational savings journey. Our goal is to equip you with the knowledge needed to navigate the complexities of 529 plans and harness their full potential.

Anúncios

Understanding the Core of 529 Plans and Federal Tax Benefits

Before diving into the state-specific intricacies, it’s crucial to grasp the fundamental federal tax advantages of 529 plans. These plans are officially known as “qualified tuition programs” and are authorized by Section 529 of the Internal Revenue Code. The primary federal benefits include:

- Tax-Free Growth: Any earnings within a 529 plan grow free from federal income tax. This means more of your money is working for you, compounding over time without being eroded by annual taxes on investment gains.

- Tax-Free Withdrawals: When withdrawals are made for qualified education expenses, they are also free from federal income tax. Qualified expenses are broad and include tuition, fees, books, supplies, equipment, and even room and board for students enrolled at least half-time.

- Beneficiary Changes: You can change the beneficiary of a 529 plan to another eligible family member without tax consequences. This flexibility is invaluable if your initial beneficiary decides not to pursue higher education or receives a scholarship.

- No Income Limitations: Unlike some other education savings vehicles, there are no income limitations to contribute to a 529 plan. This makes them accessible to a wide range of families.

- Estate Tax Benefits: Contributions to a 529 plan are considered completed gifts for federal gift tax purposes, allowing you to remove assets from your taxable estate while retaining control over the account.

While these federal benefits are substantial, they are just the starting point. The real game-changer for many families lies in the additional 529 plan tax benefits offered by their home state or other states. These state-level incentives can significantly boost your savings and reduce your overall tax burden.

Decoding State-Specific 529 Plan Tax Benefits for 2026

The variety of 529 plan tax benefits at the state level can be both a blessing and a challenge. Each state has its own rules, and what works best for one family might not be ideal for another. Understanding these differences is key to maximizing your savings. Here’s a breakdown of the common types of state-specific benefits you might encounter:

1. State Income Tax Deductions or Credits for Contributions

This is perhaps the most common and impactful state-level benefit. Many states offer a deduction or a credit on your state income tax for contributions made to a 529 plan. The specifics vary widely:

- Deduction for Contributions to Any State’s Plan: A handful of states are particularly generous, allowing residents to deduct contributions made to *any* state’s 529 plan, not just their own. This offers maximum flexibility. States like Arizona, Kansas, Minnesota, Missouri, Montana, and Pennsylvania often fall into this category, though specific rules and limits apply and can change.

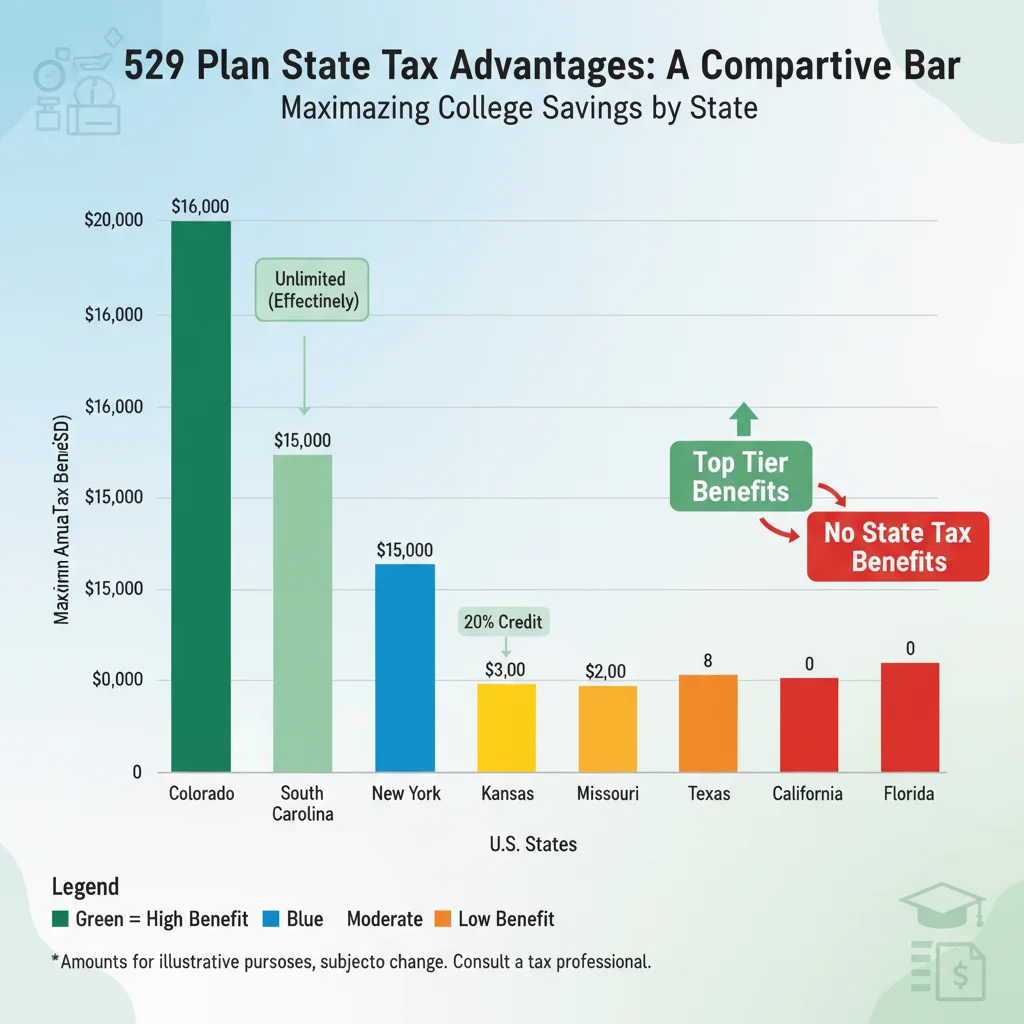

- Deduction for Contributions to Your Home State’s Plan: Most states that offer a tax incentive limit it to contributions made to their own state’s 529 plan. This encourages residents to invest locally. The deduction amounts can vary from a few thousand dollars per taxpayer to the entire contribution amount, often with annual limits. For example, New York offers a deduction of up to $5,000 for single filers and $10,000 for married couples filing jointly.

- Tax Credits: Instead of a deduction, some states offer a tax credit, which directly reduces your tax liability dollar-for-dollar. While less common than deductions, credits can be incredibly valuable. Indiana, for instance, has historically offered a generous credit.

- Recapture Provisions: Be aware that some states have “recapture” provisions. If you take a non-qualified withdrawal from your 529 plan, the state may recapture the tax deductions or credits you previously claimed. This is a crucial detail to consider.

2. Tax-Free Withdrawals for Non-Qualified Expenses (State-Specific)

While federal law dictates tax-free withdrawals for qualified education expenses, some states offer additional flexibility. For example, a few states might not impose state income tax on withdrawals used for certain non-qualified expenses that are still education-related, although this is less common and should be verified with the respective state’s specific guidelines for 2026.

3. Protection from Creditors

In some states, 529 plan assets are protected from creditors, offering an additional layer of security for your educational savings. This can be a significant advantage, particularly for self-employed individuals or those with potential liability concerns.

4. No State Income Tax on Earnings or Withdrawals

Beyond the initial deduction or credit, many states also exempt 529 plan earnings from state income tax, even if they tax other investment income. This mirrors the federal benefit and further enhances the tax efficiency of these plans. For states that don’t have a state income tax (e.g., Florida, Texas, Nevada), this particular benefit is less relevant, but they still offer the federal advantages.

Which States Offer the Best 529 Plan Tax Benefits in 2026? A Comparative Analysis

Identifying the “best” state for 529 plan tax benefits depends on your individual circumstances, particularly your state of residence. However, certain states consistently stand out for their generous incentives. For 2026, while exact figures can shift, the general trends are expected to continue. Here’s a look at some of the leading contenders:

States Offering Deductions for Contributions to Any State’s 529 Plan:

These states provide the most flexibility, allowing residents to choose a 529 plan from any state that best suits their investment preferences, while still receiving a state income tax deduction. This is a huge advantage as it separates the investment decision from the tax benefit decision.

- Arizona: Often allows a deduction for contributions to any 529 plan, with a maximum deduction that can be quite substantial.

- Kansas: Typically offers a deduction up to a certain limit for contributions to any 529 plan.

- Minnesota: Provides a credit or deduction for contributions to any 529 plan, depending on income level.

- Missouri: Known for allowing a deduction for contributions to any 529 plan, with a generous annual limit.

- Montana: Offers a deduction for contributions to any 529 plan.

- Pennsylvania: A popular choice for its deduction on contributions to any 529 plan, often with no income limitations on the deduction itself, though annual limits apply.

If you reside in one of these states, you have the luxury of shopping around for the 529 plan with the lowest fees, best investment options, and strongest track record, without sacrificing your state tax break. This is a critical point for maximizing your 529 plan tax benefits.

States Offering Generous Deductions or Credits for Their Own State’s 529 Plan:

For residents of these states, choosing their home state’s 529 plan can lead to significant tax savings.

- New York: Offers a deduction of up to $5,000 for single filers and $10,000 for married couples filing jointly for contributions to New York’s 529 plan. This is a direct deduction from your taxable income.

- Illinois: Provides a deduction of up to $10,000 for single filers and $20,000 for married couples filing jointly for contributions to the Bright Start or Bright Directions 529 plans.

- Virginia: Offers an unlimited deduction for contributions to Virginia529 plans, though there are stipulations for those over 70. This makes it incredibly attractive for high-income earners.

- South Carolina: Provides an unlimited deduction for contributions to its Future Scholar 529 plan.

- Georgia: Offers a deduction of up to $8,000 per beneficiary per year for contributions to the Georgia Path2College 529 Plan.

- Indiana: Known for its 20% state income tax credit on contributions up to $5,000 (a maximum credit of $1,000), which is a dollar-for-dollar reduction in tax liability. This is one of the most powerful 529 plan tax benefits available.

- Utah: Offers a tax credit for a percentage of contributions to the Utah Educational Savings Plan (UESP), with limits based on filing status.

It’s important to note that these are just examples, and the specific limits and rules can change. Always verify the most current regulations for 2026 directly with your state’s tax authority or the official 529 plan website.

States with No State Income Tax or No State-Specific 529 Benefits:

Several states do not have a state income tax (e.g., Florida, Nevada, Texas, Washington, Wyoming, Alaska, South Dakota), making state-specific income tax deductions or credits irrelevant. In these states, the federal tax benefits of 529 plans are still highly valuable. Other states may have a state income tax but do not offer any specific 529 plan tax benefits beyond the federal ones. For residents of these states, the strategy shifts to focusing purely on the investment performance and fees of different state plans, as there’s no state tax incentive to tie them to a particular plan.

Strategies for Maximizing Your 529 Plan Tax Benefits in 2026

Once you understand the various state-specific 529 plan tax benefits, the next step is to formulate a strategy to maximize them. Here are several key considerations:

1. Choose Your State Wisely (If Applicable)

If your state offers a deduction or credit only for contributions to its own 529 plan, it often makes financial sense to invest in your home state’s plan to capture that immediate tax benefit. The value of this upfront saving can outweigh minor differences in investment performance or fees compared to out-of-state plans.

2. Consider “Out-of-State Shopping”

If your state allows deductions for contributions to *any* 529 plan, or if your state offers no specific tax benefits, you have the freedom to choose the best plan based on its investment options, fees, and historical performance. Websites like Savingforcollege.com provide excellent tools for comparing plans across states.

3. Contribute Regularly and Consistently

Even small, consistent contributions can add up over time, especially when coupled with tax-free growth and state tax benefits. Automating contributions can help ensure you don’t miss out on potential tax deductions.

4. Understand Contribution Limits and Recapture Rules

Be aware of any annual contribution limits for state tax deductions or credits. Contributing more than the deductible amount won’t yield additional state tax savings for that year. Also, always review the recapture rules. If you anticipate needing to withdraw funds for non-qualified expenses, the potential recapture of state tax benefits could diminish your overall savings.

5. Leverage Grandparent Contributions

Grandparents can also contribute to a 529 plan for their grandchildren. In many states, if the grandparent resides in a state that offers a tax deduction, they can claim that deduction on their own state income tax return, providing another avenue for 529 plan tax benefits.

6. Be Mindful of Gift Tax Exclusion

Contributions to a 529 plan are considered gifts. You can contribute up to the annual gift tax exclusion amount (which is $18,000 per individual in 2024, and likely to be similar in 2026) without incurring gift tax. You can also front-load five years of contributions at once, allowing a lump sum of $90,000 (or more for married couples) per beneficiary without gift tax implications, provided no other gifts are made to that beneficiary during the five-year period.

7. Review and Adjust Annually

The rules and offerings of 529 plans can change. It’s wise to review your chosen plan’s performance, fees, and your state’s tax laws annually to ensure you are still maximizing your 529 plan tax benefits. Your financial situation may also change, warranting adjustments to your contribution strategy.

Potential Changes and Considerations for 2026

While this article provides a comprehensive overview based on current trends and historical data, it’s essential to remember that tax laws and 529 plan specifics can evolve. For 2026, potential changes to consider include:

- State Legislative Changes: State legislatures regularly review and modify their tax codes. New deductions, credits, or changes to existing ones could be introduced.

- Federal Policy Updates: Although less frequent, federal legislation could impact 529 plans, such as expanding qualified expenses or altering contribution rules. The Secure Act 2.0, for example, introduced the ability to roll over unused 529 funds to a Roth IRA, albeit with specific limitations. This is a significant new benefit to consider.

- Economic Factors: Market performance and economic conditions can influence investment options and fees within 529 plans.

Staying informed by checking official state 529 plan websites and consulting with a qualified financial advisor will be crucial as 2026 approaches.

Beyond Tax Benefits: Other Factors When Choosing a 529 Plan

While 529 plan tax benefits are a major draw, they shouldn’t be the *only* factor in your decision. Other important considerations include:

- Investment Options: Look for a plan with a diverse range of investment portfolios, including age-based options (which automatically adjust asset allocation as the beneficiary gets older), static portfolios, and individual fund options.

- Fees and Expenses: High fees can erode your returns. Compare administrative fees, underlying fund expenses, and program management fees across different plans.

- Performance History: While past performance doesn’t guarantee future results, it can provide insight into the management and effectiveness of a plan’s investment options.

- Ease of Use: Consider the plan’s online interface, customer service, and overall ease of managing your account.

- Flexibility: The ability to change beneficiaries, investment options, and withdrawal methods can be important.

For residents of states with no state income tax benefits for 529 contributions, these factors become even more important, as the decision is purely investment-driven.

Conclusion: Strategic Savings with 529 Plans in 2026

Saving for education is a long-term commitment, and leveraging the full spectrum of 529 plan tax benefits can make a substantial difference in your financial journey. By understanding the federal advantages and meticulously comparing state-specific deductions, credits, and other incentives for 2026, you can strategically choose and manage a 529 plan that maximizes your savings growth and minimizes your tax burden.

Whether you reside in a state that offers generous deductions for its own plan, allows contributions to any state’s plan, or has no state income tax, there’s a strategic approach to optimize your educational savings. Remember to stay informed about legislative changes, consult with financial professionals, and regularly review your plan to ensure it continues to align with your financial goals and the evolving educational landscape. Your proactive planning today will pave the way for a brighter educational future for your loved ones tomorrow.

")