The 2026 Small Business Lending Landscape: Comparing SBA Loans vs. Private Funding Options

As we approach 2026, the financial landscape for small businesses continues to evolve at a rapid pace. Entrepreneurs and established small business owners alike are constantly seeking the most effective ways to secure capital for growth, expansion, or even just to maintain operations during lean times. The decision between pursuing an SBA Private Funding 2026 option is often one of the most critical financial choices a business can make. This comprehensive guide aims to dissect the nuances of both Small Business Administration (SBA) loans and private funding options, providing you with the insights needed to make an informed decision for your venture in the coming years.

Understanding the intricacies of each funding avenue is paramount. SBA loans, backed by the U.S. government, often come with more favorable terms but typically involve a more rigorous application process. Private funding, on the other hand, can offer quicker access to capital and greater flexibility but may come at a higher cost. The optimal choice depends heavily on your business’s specific needs, financial health, growth trajectory, and risk tolerance. Let’s embark on a detailed exploration to help you navigate this complex yet crucial aspect of small business management.

Anúncios

The Enduring Appeal of SBA Loans in 2026

SBA loans have long been a cornerstone of small business finance, designed to minimize risk for lenders and make capital more accessible to entrepreneurs. In 2026, their fundamental appeal remains strong, primarily due to government backing that encourages banks and other financial institutions to lend to small businesses that might otherwise be deemed too risky. This backing often translates into more attractive terms for borrowers.

Anúncios

Understanding the SBA Loan Ecosystem

The SBA itself does not directly lend money; instead, it sets guidelines for loans made by its partnering lenders (banks, credit unions, and other financial institutions). The SBA guarantees a portion of these loans, reducing the risk for lenders and encouraging them to provide financing to small businesses. In 2026, several popular SBA loan programs continue to dominate the landscape:

- SBA 7(a) Loan Program: This is the most common and flexible SBA loan program, offering financial assistance for a wide range of business purposes, including working capital, equipment purchases, real estate acquisition, and refinancing existing debt. Loan amounts can go up to $5 million, with terms extending up to 25 years for real estate. The government guarantee can be up to 85% for loans up to $150,000 and 75% for loans above $150,000.

- SBA 504 Loan Program: Specifically designed for major fixed assets that promote business growth and job creation, such as purchasing or renovating commercial real estate, or acquiring long-term machinery and equipment. These loans involve a partnership between a Certified Development Company (CDC), a bank, and the small business. The SBA guarantees a portion of the CDC’s debentures.

- SBA Microloan Program: These are smaller loans, typically up to $50,000, administered through non-profit community-based organizations. They are ideal for startups and small businesses needing modest capital for working capital, inventory, supplies, furniture, fixtures, or equipment.

- SBA Disaster Loans: Although not part of the regular business funding cycle, these are crucial for businesses in declared disaster areas, providing low-interest loans to help businesses recover.

Advantages of SBA Loans in 2026

The benefits of opting for an SBA loan in 2026 are compelling for many small businesses:

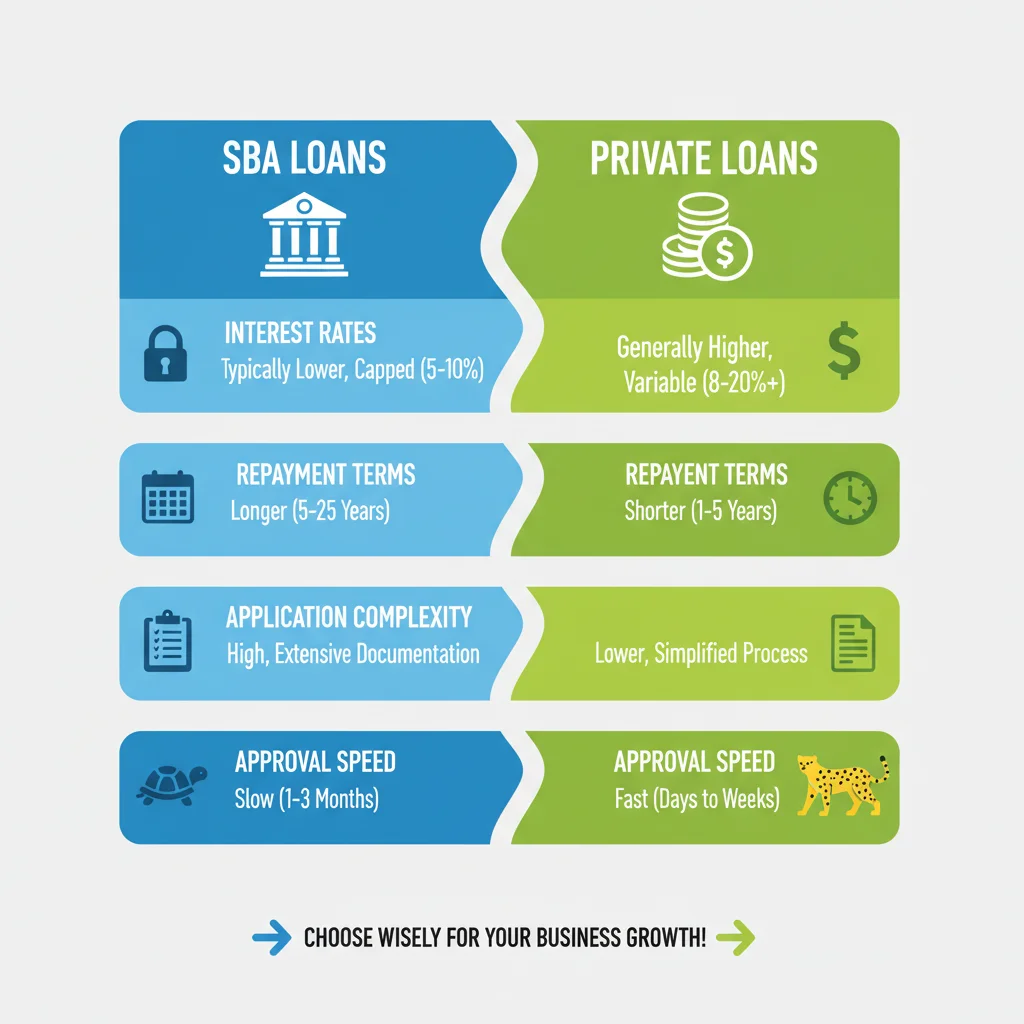

- Lower Interest Rates: Due to the government guarantee, lenders can offer lower interest rates compared to conventional loans, making repayment more manageable.

- Longer Repayment Terms: SBA loans typically feature longer repayment periods, which translates to lower monthly payments and improved cash flow for the business. This is a significant advantage, especially for businesses with fluctuating revenues or those just starting out.

- Lower Down Payments: Many SBA loans require a smaller down payment from the borrower than traditional bank loans, conserving valuable working capital.

- Flexibility in Use of Funds: Especially with the 7(a) program, funds can be used for a wide array of business purposes, offering significant operational flexibility.

- Accessible to a Broader Range of Businesses: The SBA’s mission is to support small businesses, meaning they are often more willing to consider businesses that might be rejected by traditional lenders due to limited operating history, industry type, or lower credit scores.

Disadvantages and Challenges of SBA Loans in 2026

While attractive, SBA loans also come with their own set of challenges that businesses must be prepared for:

- Rigorous Application Process: The application for an SBA loan is notoriously detailed and time-consuming. It requires extensive documentation, including business plans, financial statements, tax returns, and personal financial information. This can be a significant hurdle for businesses needing quick access to funds.

- Longer Approval Times: Due to the thorough vetting process by both the lender and the SBA, approval times for SBA loans can be considerably longer than for private funding options, sometimes extending to several weeks or even months.

- Strict Eligibility Requirements: Businesses must meet specific SBA size standards, operate for profit, and demonstrate a need for the loan, among other criteria. Certain industries may also be excluded.

- Collateral Requirements: While the SBA guarantees a portion of the loan, lenders will still typically require collateral, and personal guarantees are often necessary, which can put personal assets at risk.

- Credit Score Importance: Although SBA loans are more forgiving than traditional loans, a good personal and business credit score is still crucial for approval and securing the best terms.

The Dynamic World of Private Funding in 2026

Private funding encompasses a broad spectrum of financing options provided by non-governmental entities. This category has seen immense innovation and growth, particularly with the proliferation of online lenders and alternative finance solutions. In 2026, private funding continues to offer speed, flexibility, and accessibility that traditional and SBA loans sometimes lack.

Exploring Various Private Funding Avenues

The landscape of private funding is diverse, catering to different business needs and risk profiles:

- Term Loans: Offered by banks, credit unions, and online lenders, these are lump-sum loans repaid over a fixed period with regular interest payments. They can be secured or unsecured.

- Lines of Credit: Similar to a credit card, a business line of credit allows businesses to draw funds as needed, up to a certain limit, and only pay interest on the amount borrowed. This is excellent for managing cash flow fluctuations.

- Invoice Factoring/Financing: Businesses can sell their outstanding invoices to a third party (a factor) at a discount to get immediate cash. This is a good option for businesses with many outstanding accounts receivable.

- Merchant Cash Advances (MCAs): A lump sum is provided in exchange for a percentage of future credit card sales. While quick to obtain, MCAs often come with very high effective interest rates.

- Equipment Financing: Specific loans used to purchase business equipment, with the equipment itself often serving as collateral.

- Venture Capital (VC) and Angel Investors: For high-growth startups with significant potential, VCs and angel investors provide capital in exchange for equity. This is not debt but an investment.

- Crowdfunding: Raising small amounts of capital from a large number of individuals, often through online platforms. This can be equity-based, debt-based, or rewards-based.

Advantages of Private Funding Options in 2026

The allure of private funding, especially from online lenders, lies in its distinct benefits:

- Speed and Efficiency: Many private lenders, particularly online platforms, boast streamlined application processes and rapid approval times, often providing funds within days or even hours. This is crucial for businesses facing urgent capital needs.

- Flexibility and Customization: Private lenders often have more flexible eligibility criteria than SBA or traditional bank loans. They may be more willing to work with businesses with lower credit scores, shorter operating histories, or those in niche industries. Loan terms can also be more readily customized to a business’s unique cash flow patterns.

- Less Bureaucracy: The application process is typically less document-intensive and involves fewer layers of approval compared to SBA loans.

- Broader Range of Options: The sheer variety of private funding products means businesses can often find a solution tailored to very specific needs, whether it’s short-term working capital, equipment acquisition, or bridging cash flow gaps.

- Innovation in Lending: The private lending sector is constantly innovating, offering new types of financial products and leveraging data analytics to assess creditworthiness beyond traditional metrics.

Disadvantages and Considerations for Private Funding in 2026

While agile, private funding also comes with potential drawbacks that warrant careful consideration:

- Higher Interest Rates and Fees: Generally, private loans, especially from alternative lenders, come with higher interest rates and fees than SBA-backed loans. This is to compensate for the increased risk and faster approval times.

- Shorter Repayment Terms: Private loans often have shorter repayment schedules, which can lead to higher monthly payments and put more strain on a business’s cash flow.

- Predatory Lending Concerns: The less regulated nature of some parts of the private lending market means businesses must be vigilant against predatory lenders offering unfavorable terms. Thorough due diligence is essential.

- Collateral and Personal Guarantees: While some private loans are unsecured, many still require collateral or personal guarantees, especially for larger amounts or businesses with higher perceived risk.

- Complex Fee Structures: Beyond interest rates, private loans can have various fees, including origination fees, administrative fees, and late payment penalties, which can significantly increase the overall cost of borrowing. It’s crucial to understand the Annual Percentage Rate (APR) to compare costs accurately.

Key Factors for Choosing Between SBA and Private Funding in 2026

The decision between an SBA Private Funding 2026 option is not one-size-fits-all. It requires a careful evaluation of several key factors specific to your business.

1. Your Business’s Financial Health and Creditworthiness

Your credit score (both personal and business), revenue stability, and profitability play a pivotal role. Businesses with strong credit, consistent revenue, and a solid financial history are better positioned for SBA loans with their favorable terms. Businesses with less-than-perfect credit or a shorter operational history might find private lenders more accommodating, though often at a higher cost.

2. Urgency of Funds

How quickly do you need the capital? If you require funds within days or a couple of weeks to seize an opportunity or address an immediate need, private funding, especially from online lenders, will likely be your best bet. If you have the luxury of time (several weeks to months), and your business qualifies, an SBA loan can provide more cost-effective financing.

3. Loan Amount and Purpose

Small amounts for working capital might be better suited for an SBA Microloan or a private line of credit. Large sums for real estate or major equipment purchases often align well with SBA 7(a) or 504 programs due to their longer terms and lower rates. For very high-growth, innovative startups, venture capital or angel investment might be more appropriate than debt financing.

4. Repayment Capacity and Cash Flow

Evaluate your business’s ability to handle monthly payments. SBA loans, with their longer terms and lower payments, can be less burdensome on cash flow. Private loans, particularly short-term ones, can have high monthly payments that require robust and consistent cash flow to manage.

5. Collateral Availability and Personal Guarantees

Are you willing and able to pledge collateral? Are you comfortable providing a personal guarantee? Both SBA and many private lenders will require these, especially for larger loans. Understanding the implications of personal guarantees on your personal assets is crucial.

6. Industry and Business Type

Certain industries might have better access to specific types of funding. For instance, tech startups often attract venture capital, while established retail businesses might find traditional bank or SBA loans more suitable. Some industries are explicitly excluded from SBA programs.

Navigating the Application Process in 2026

Regardless of whether you choose SBA Private Funding 2026, preparing for the application process is key to success. This involves thorough documentation and a clear understanding of your business’s financial narrative.

For SBA Loans:

- Comprehensive Business Plan: A well-articulated plan outlining your business model, market analysis, management team, and financial projections.

- Detailed Financial Statements: Profit and loss statements, balance sheets, and cash flow projections for at least the past three years (if applicable) and projections for the future.

- Tax Returns: Personal and business tax returns for recent years.

- Legal Documents: Business licenses, articles of incorporation, leases, and contracts.

- Personal Financial Statement: Details of your personal assets and liabilities.

For Private Funding:

While generally less onerous, you will still need:

- Basic Business Information: Legal structure, industry, time in business.

- Bank Statements: Often for the last 3-12 months, to assess cash flow.

- Credit Score: Lenders will pull both personal and business credit reports.

- Revenue Information: Proof of consistent income.

- Collateral Documentation: If applying for a secured loan.

Emerging Trends and What to Expect in 2026

The lending landscape is dynamic, and 2026 will likely bring continued shifts:

- Increased Digitalization: Expect further automation and digitalization of loan applications and underwriting processes for both SBA and private lenders, potentially speeding up approval times across the board.

- Focus on Data Analytics: Lenders will increasingly rely on advanced data analytics and AI to assess creditworthiness, moving beyond traditional FICO scores to evaluate real-time business performance and potential.

- Sustainability and ESG Factors: There may be a growing emphasis on Environmental, Social, and Governance (ESG) factors, with some lenders offering preferential terms to businesses demonstrating strong sustainability practices.

- Hybrid Lending Models: We might see more hybrid models emerge, combining aspects of SBA guarantees with the speed and flexibility of private lenders, creating new funding solutions for small businesses.

- Economic Volatility Preparedness: Lenders and borrowers will both be more attuned to economic fluctuations, with a greater emphasis on stress testing and contingency planning in loan agreements.

Making Your Informed Decision for SBA Private Funding 2026

Ultimately, the choice between SBA loans and private funding for your small business in 2026 boils down to a strategic alignment with your business goals, financial standing, and timeline. If your business has a solid financial history, good credit, and you can afford the time for a thorough application process, an SBA loan often provides the most advantageous terms and lowest overall cost of capital. This is particularly true for significant, long-term investments like real estate or major equipment.

Conversely, if you require immediate capital, have a less conventional financial profile, or prioritize speed and flexibility over the lowest possible interest rate, private funding offers a wealth of options. Online lenders, in particular, have democratized access to capital for many businesses that might not qualify for traditional bank or SBA loans.

It’s also important to remember that these are not mutually exclusive paths. Some businesses might utilize private funding for short-term needs and then pursue an SBA loan for long-term growth. Consulting with a financial advisor or a loan specialist who understands the SBA Private Funding 2026 landscape can provide invaluable guidance tailored to your specific situation. They can help you sift through the myriad of options, understand the fine print, and position your business for successful funding.

Conclusion: Strategic Capital for a Thriving 2026

The 2026 small business lending landscape offers diverse opportunities for securing capital. By meticulously comparing SBA loans and various private funding options, understanding their respective advantages and disadvantages, and critically assessing your business’s unique circumstances, you can make a strategic decision that propels your growth and ensures long-term stability. Whether it’s the government-backed security of an SBA loan or the agile solutions of private lenders, the right funding can be the catalyst for your business’s success in the years to come. Plan diligently, research thoroughly, and choose wisely to unlock your business’s full potential.

The journey to securing capital is a critical one, and being well-informed is your greatest asset. As 2026 unfolds, stay abreast of market changes, lender offerings, and economic indicators to ensure your funding strategy remains robust and responsive. Good luck!